More than hardware and networking: Huawei does digital transformations

In the massive and confusing landscape of the digital transformation market, Huawei’s brand centers around hardware and telecommunications — essential, though unexciting, components. Beyond the brand, Huawei has been delivering digital services and engaging with enterprises on their digital transformations in the company’s home market of China and globally, steadily building experience and use cases to support a substantial services practice.

In a wide-ranging discussion with Hank Stokbroekx, Huawei’s VP for Enterprise Services, TBR learned the company has strategically partnered with vendors such as Accenture and EY on digital transformation engagements outside China while building its own reference use cases on the mainland. Stokbroekx highlighted two for TBR that indicate where Huawei is headed.

Shenzhen Bao’an International Airport

In Shenzhen, Huawei’s headquarters, the company has been piloting various digital transformation projects within Shenzhen Bao’an International Airport, including passenger recognition, analytics and IoT solutions. In Stokbroekx’s view, profitability is not the No. 1 priority, as the heightened profile for Huawei of being integral to the airport’s transformation provides brand and marketing value on its own.

During the Huawei 2021 Global Analyst Summit in April, Stokbroekx introduced analysts to Industry Operations Assistance. The solution, based on a platform and ecosystem piloted in China, enables intelligent operation command center monitoring inside a company. Intelligent Operation & Maintenance was used in the Shenzhen airport, which previously had a complex operational system with multiple requirements for operation and maintenance services. As a result of the implementation, the airport experienced reduced time to locate a fault in its network from one day to 20 minutes and improved systems availability by 20%, leading to reduced flight delays.

The solution also enabled the airport to improve operation and maintenance efficiency by 30%. In TBR’s assessment, Shenzhen Bao’an International Airport offers Huawei two massive opportunities. First, every client from every different industry coming to Huawei’s headquarters will pass through the airport, providing the company a chance to demonstrate its digital transformation capabilities in a direct and experiential way. Second, successfully deploying solutions at one airport provides reference use cases for embarking on other digital transformation pilot programs at other airports around the region.

https://tbri.com/wp-content/uploads/2021/05/bao-menglong-FhoJYnw-cg-unsplash.jpg427640Patrick Heffernan, Practice Manager and Principal Analysthttps://tbri.com/wp-content/uploads/2021/09/TBR-Insight-Center-Logo.pngPatrick Heffernan, Practice Manager and Principal Analyst2021-05-24 09:28:052021-05-24 09:28:05Think global, act local: Huawei’s digital transformation services

Based on a foundation in Linux, which enables containerized applications to move across physical and virtual environments, Red Hat maintains a unique market presence with its neutral PaaS solution, Red Hat OpenShift. Red Hat’s vision to extend the applicability of Red Hat OpenShift, which is leveraged by 90% of Fortune 500 companies, to new use cases, consumption models and environments was one of the key takeaways from Red Hat Summit 2021.

As discussed by Paul Cormier, one of the main benefits of an open hybrid cloud approach, which is based on open code, processes and cultures, is the flexibility to run applications across environments with consistency. This approach positions Red Hat and its customers to evolve alongside emerging market trends such as AI, 5G and even quantum computing. As seen in Red Hat’s expanding top line, the company has been successful leading with an architectural approach under core brands such as Red Hat Enterprise Linux (RHEL), OpenShift and Ansible. TBR believes Red Hat will be well positioned to expand its portfolio to new markets and customers and push its open-source expertise beyond the bounds of cloud computing due to continued support from IBM (NYSE: IBM) and an expanding ecosystem of systems integrators (SIs) and ISVs.

Red Hat expands Red Hat OpenShift usage with new managed cloud services

While Red Hat has offered Red Hat OpenShift as a managed service for some time, scaling up managed support is becoming a key initiative for the company, especially as more customers pursue managed offerings to offload operational tasks at both the applications and infrastructure layers. To broaden the applicability of Red Hat OpenShift, at the event, the company unveiled three new cloud managed services supporting customers’ need to build, deploy and integrate modern applications within their existing Red Hat OpenShift environment, either in the cloud or on premises.

At the Red Hat Summit 2021 conference, Red Hat continued to convey to a group of customers, partners and industry analysts the message of open hybrid cloud the company has been leading with for over a decade. Over the course of the three-day event, executives including Red Hat CEO Paul Cormier and Products and Technologies EVP Matt Hicks outlined Red Hat’s evolution from an operating system company to one offering a full suite of self-service software and services for hybrid cloud.

https://tbri.com/wp-content/uploads/2021/05/network-2002812_640.jpg426640Catie Merrill, Senior Analysthttps://tbri.com/wp-content/uploads/2021/09/TBR-Insight-Center-Logo.pngCatie Merrill, Senior Analyst2021-05-19 09:30:002021-05-19 09:30:00Scope of Red Hat OpenShift expands, bringing hybrid cloud to new environments and open-source projects

Accelerating success through successful acquisitions integration

TBR recently had the opportunity to catch up with TELUS International President and CEO Jeff Puritt, two years after the company’s inaugural analyst summit in Las Vegas and two $1 billion acquisitions later. Right from the start it was clear that the company has been able to preserve its most valuable asset, its culture, despite massive portfolio expansion and operating model transformation (TELUS International went public on Feb. 3).

The purchase of Competence Call Center (CCC) in February 2020 and subsequent acquisition of Lionbridge AI in December 2020 have not only provided the company with the breadth of offerings necessary to navigate an increasingly complex ecosystem bolstered by the advent of AI and consumer-generated content, but have also enhanced its value proposition; as Puritt positioned it, “Purpose built to be digital first responders.”

CCC added over 8,000 employees, mostly across European operations. Lionbridge AI provided access to both IP and a crowdsourcing community of over 1 million trained professionals with skills ranging from speaking multiple languages to holding, in some instances, advanced degrees. Integrating large-scale acquisitions such as these is not an easy task, but Puritt and his team are successfully executing on these transactions, guided by principles focused on employee engagement and customer satisfaction. In its first full quarter as a publicly traded company, TELUS International reported 57% year-to-year revenue growth to $505 million in 1Q21, with strong contribution from these recent purchases; absent that contribution, TELUS International’s growth was 20% on an annual basis during the same period. For comparison: In TBR’s IT Services Vendor Benchmark, we estimate on average total revenue for the 30 benchmarked vendors will expand by low single digits in 2021.

Mixing AI into employee culture at scale is not easy, but TELUS International seems to be mastering it

With AI permeating consumers’ everyday lives and enterprises’ IT and business operations, TELUS International has an opportunity to become a household name as an automation-enabled organization with human capabilities. The purchase of Lionbridge AI could serve as a catalyst of that transformation at scale, given the company’s AI platform and access to 1 million trained professionals that can support TELUS International in providing data annotation services for text, images, videos and audio.

While the future promise of AI depends on its ability to adapt and recommend with minimal human intervention, we do not anticipate the need for human support to evaporate any time soon. The increasing volume of user-generated content and the complexity and sophistication of systems will continue to necessitate the development, integration and management of algorithms and human involvement, which TELUS International can deliver. Managing quality and ensuring privacy and security requirements are met while tapping into the crowdsourcing pool is not an easy task, but TELUS International continues to build a human-centric culture that empowers both full-time team members and crowd community members to take charge of their careers while also acting as brand ambassadors in their local communities.

TBR witnessed this culture firsthand during visits to TELUS International facilities in Las Vegas and Sofia, Bulgaria, where the company has grown roots not only to expand its recruitment reach but also to build local trust, reflected in its extensive corporate social responsibility program.

Next phase of success will depend on managing the ecosystem

As TELUS International executes on its road map as a publicly traded company, managing stakeholders’ expectations through a well-grounded vision will be key to success. Alliance partners such as Google Cloud will play a critical role in TELUS International’s ability to scale performance, especially as the company strives to win AI services and solutions opportunities, an area Google enables through its Contact Center AI solutions.

TBR, along with Puritt, recognizes that TELUS International still faces opportunity areas where the company can continue to strengthen its value proposition, one of which is consulting and advisory services. While we do not anticipate the company will double down on becoming a management consultancy, we expect TELUS International will continue to pursue a more pragmatic approach toward building domain expertise through strategic partnerships. The company has an opportunity to deepen expertise around close-to-the-data annotation and moderation services similar to the way telcos offer consulting to their telco box. Maintaining trust within the ecosystem will also support TELUS International’s move to the next phase of opportunities, especially as the company increasingly relies on AI-enabled systems. As TELUS International elevates its brand and value proposition within the highly competitive digital customer experience market, trust will come from within, starting with successful employee management.

https://tbri.com/wp-content/uploads/2021/09/TBR-Insight-Center-Logo.png00Bozhidar Hristov, Principal Analysthttps://tbri.com/wp-content/uploads/2021/09/TBR-Insight-Center-Logo.pngBozhidar Hristov, Principal Analyst2021-05-18 16:48:262021-05-18 16:48:26TELUS International: Purpose built to be digital first responders

Rackspace Technology unveils new high-touch services framework, strengthening its play in managed public cloud

In April 2021, to assert itself in the managed public cloud space, Rackspace Technology unveiled its Rackspace Elastic Engineering framework, which promises a more scalable approach to the multicloud engagement life cycle compared to standard managed services contracts. The framework provides on-demand access to pools of cloud engineers, architects and engagement managers, dubbed “pods,” that will support customers from the advisory and consulting stage to system provisioning and management. Aligned to nine dedicated specialists, each pod acts as a landing spot for customers that they will constantly engage with to achieve goals post-migration.

Rackspace Technology supports its Rackspace Elastic Engineering offering with the message: “It’s no longer enough to just be in the cloud.” While many customers will initially leverage Rackspace Technology for its vendor-neutral approach to address cloud migration requests, the pod framework is designed to support customers’ cloud-native projects, which has the potential to improve Rackspace Technology’s value-add with support for emerging technologies such as serverless functions, automation and Infrastructure as Code.

The new Rackspace Technology offering supports AWS, Microsoft Azure and Google Cloud, which addresses the growing trend of customers adopting multiple cloud platforms to support specific workloads. TBR notes many cloud service providers (CSPs) are looking to address multicloud management pain points, either with professional services or self-service solutions. TBR expects that the Rackspace Technology platform-neutral approach, combined with a customer-centric approach to cloud transformation, will help the company assert itself in the managed cloud space to increasingly capture more market share away from its technology to services-centric competitors.

With both managed services and dedicated hosting capabilities, Rackspace Technology strives to become the ‘best place to run VMware’

While Rackspace Technology has been a longtime partner of VMware, offering hosting and managed services support for core virtualization offerings, VMware’s rapid shift to the cloud has presented new opportunities for IaaS players and global systems integrators (GSIs). To make it easier for customers to move VMware outside the data center, hyperscalers are allying with VMware to deliver the VMware Cloud Foundation (VCF) platform — which comprises vSphere, NSX and vSAN — on dedicated or multitenant cloud infrastructure. TBR notes VMware has traditionally been less reliant on SI partners, but we expect the company to outsource VMware Cloud management tasks more heavily through 2021 as the portfolio continues to grow, due in part to its recent multiyear, multimillion-dollar partnership agreement with Accenture.

As a result of these dynamics, Rackspace Technology’s private cloud strategy was one of the main highlights conveyed with its launch of Rackspace Services for VMware Cloud. In addition to supporting various hosting methods, including on premises via consumption-based pricing, in Rackspace Technology data centers or through a colocation provider, the addition of Rackspace Services for VMware Cloud supports VMware clients from the services angle. As complexity and lack of in-house resources are among the leading customer concerns surrounding VMware migrations, Rackspace Technology is applying its Rackspace Elastic Engineering framework to support a number of use cases, from lift and shift to application refactoring.

Prior to going public again in August 2020, Rackspace Technology (Nasdaq: RXT) underwent a major strategic pivot, placing less emphasis on the capital-intensive data-hosting model it has been historically known for and shifting its investments to build a resource base within cloud professional services. With the announcements of Rackspace Elastic Engineering and Rackspace Services for VMware Cloud in April and May 2021, the company is competing in the managed cloud space with a new high-touch services framework designed to support enterprise clients at all layers of the cloud stack, from infrastructure management to application modernization. Rackspace Technology’s long-standing technology alliances with Amazon Web Services (AWS) (Nasdaq: AMZN), Microsoft (Nasdaq: MSFT), Google Cloud (Nasdaq: GOOGL) and VMware (NYSE: VMW); ability to host clients’ enterprise workloads in a dedicated cloud; and well-established Fanatical Experience brand are among the ways the company will not only seek differentiation and position itself as an alternative to peers but also establish itself as an “un-GSI.”

https://tbri.com/wp-content/uploads/2021/05/dallas-reedy-F2HTC_CF4Jo-unsplash.jpg427640Catie Merrill, Senior Analysthttps://tbri.com/wp-content/uploads/2021/09/TBR-Insight-Center-Logo.pngCatie Merrill, Senior Analyst2021-05-13 09:11:172021-05-13 09:11:17Rackspace Technology: Becoming elastic as the ‘un-GSI’

It is always hit or miss whether a blog post will solicit dialogue from readers. TBR’s recent blog post Who is going to want Boomi? certainly struck a chord. The blog focused on the actions of the private equity firms intending to acquire Boomi, which ultimately led Boomi to provide TBR with deeper insight into its most recent achievements, activities and aspirations as the company moves to new corporate ownership. Boomi has a sound growth strategy with a high chance of success, assuming the company and its new owners are in strategic alignment.

Evaluating the business using an inside-out/outside-in construct provides a reasonable framework for the market implications Boomi ― and really any integration PaaS (iPaaS) vendor ― will face in the years ahead. The situation starts with a universal fact: Digital businesses gain a competitive advantage against peers if they automate the flow of data across their organization. Any step where a business has to add labor when a peer does not is a cost disadvantage. In this respect, Boomi’s value is twofold: 1) automations can be built into the process and tightly integrated so that they don’t break as applications evolve, and 2) organizations can create even greater advantage when they are discovering data from all of their sources and understand the data and applications involved in the automation process.

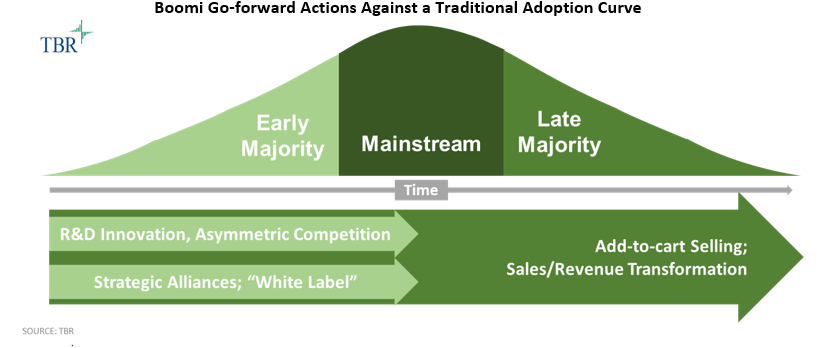

Figure 1

Outside in: The rise of data management and asymmetric competition

Our initial blog on the sale of Boomi referenced UiPath and startups Kong and Entefy as potential asymmetric challengers to Boomi’s core value proposition. Additionally, you have the basic PaaS offerings from the exascale cloud platforms providing prebuilt connectors and myriad additional services for security, data protection and data management. SaaS players, as mentioned in our prior blog, offer prebuilt integrations to popular, adjacent applications. Numerous vendors vie for what they generally call single-pane-of-glass management in multiple forms, with all vendors stressing analytics and automation in some manner.

Just as paramount is the economywide war for talent. Qualified talent versed in new technologies and tools are sought virtually everywhere, making it an employee’s market. As is the case with any acquisition, talent retention and recruitment will be key to the innovations Boomi has charted out in its development road map. In acquisition parlance, it is called putting “the golden handcuffs” on essential personnel to ensure they do not jump to a competing firm. Locking down key engineering talent will be critical.

Situationally, iPaaS tool sets can be acquired either in best-of-breed fashion or by standardization on one platform that is expansive enough to solve an immediate need and evolve with the organization. In large enterprises, there could be a mix of tools based on those brought into the organization via acquisition. In this way, iPaaS brands can be pigeonholed for what they have been offering and not necessarily given consideration for their go-forward innovations. In turn, tool purchases are often a derived decision as part of a broader initiative. The cost is justified in terms of the time savings for the business initiative rather than how the purchase will make the life of the IT department easier.

It is for this reason Figure 1 references “Strategic Alliances; ‘White Label.’” Externally, many global systems integrators (GSIs) are pivoting to managed services offerings, especially the advisory firms with deep tax and audit credentials, whose distinction comes from the tax and audit knowledge base they can automate to address data management, governance and compliance rules.

By underpinning GSI software development with its own tools, Boomi can gain a distinct selling advantage into large enterprises as it will have these influencers and quasi sellers at its disposal. Tighter relationships will also help Boomi keep an ear to the ground on the emerging technology vendors that GSIs and early adopter enterprises are considering and those that pose an asymmetric threat to the Boomi core.

Furthermore, Boomi made clear it does not aspire to substantially grow its consulting and services operations. GSIs will find this clear swim lane delineation refreshing considering the ways in which traditional services and software firms are beginning to encroach on one another’s core offerings.

Inside out: Transforming direct selling and creating new demand through ‘add to cart’

As a technology firm selling technology to IT departments, Boomi has sound, traditional selling motions. Increasingly, however, we hear the clarion call of selling business outcomes, and that move to consultative selling to lines of business will be necessary, given technology matters less and less while people and process matter more. In turn, studies show buyers want to self-research products and then self-provision those products from online portals.

Boomi has made steps in that regard with the availability of its AtomSphere Go edition, which aims to give customers a frictionless buying experience, at an early entry price point of $50 per month. AtomSphere Go also gives Boomi a way to disaggregate the various services in the existing offer to allow Boomi to move down market to reach late-majority enterprises. Additionally, Boomi recently announced AtomSphere Go is available on Amazon Marketplace, the mecca for seamless, add-to-cart ordering.

That type of selling, often called “land and expand,” has a very different set of operating best practices than traditional direct, or blue suit, selling. The aspiration of this kind of selling is lifetime customer value (LCV). It requires a different type of telephone support that is part technical advisory and part consultative selling for cross- and up-sell opportunities with smaller enterprises.

It is also a business model where revenue and expense do not align to the 90-day quarterly reporting cycle. This requires a leap of trust to embark on such selling approaches, as costs will far outweigh revenue until scale is achieved and the “flywheel effect” kicks in. For startup operations it is a very prominent challenge, and for Boomi the challenge will come more from setting up the operations with different motions and finding a way to balance investing in selling motions with awaiting payoff of the new add-to-cart operations.

Situation analysis: Never confuse a clear view for a short distance

TBR has laid out Boomi’s situation analysis levers as 1) talent retention and ongoing innovation to continue evolving a traditional space (iPaaS) that is being encroached upon by startups and established vendors on all sides, 2) heightened partner selling, and 3) a challenging shift to the add-to-cart selling model primarily to move down market, which requires fiscal patience. Provided there’s a vision match with the new owners, Boomi has solid platform depth and breadth with a reasonable innovation road map to survive and thrive in this ever-accelerating business pivot where automating data management, seamlessly moving data and empowering the right users to engage with data are paramount to maintain a persistent competitive advantage no matter the standard industrial classification (SIC) code.

So, what do you think? Will Boomi’s strategy succeed with new management?

In TBR’s newest blog series, What Do You Think?, we’re sharing questions our subject-matter experts have been asking each other lately, as well as posing the question to our readers. If you’d like to discuss this edition’s topic further, contact Geoff Woollacott at [email protected].

https://tbri.com/wp-content/uploads/2021/04/muhammad-haikal-sjukri-1NzJggtJ6j4-unsplash-scaled-1.jpg25602048adminhttps://tbri.com/wp-content/uploads/2021/09/TBR-Insight-Center-Logo.pngadmin2021-05-12 16:10:082021-05-12 16:10:08Will Boomi’s strategy succeed with new management?

Leidos expands in Australia with a defense IT modernization award and the launch of a new software development facility

Leidos will join APAC-based partner Fujitsu and U.S.-based partner KBRWyle on a three-year, AU$175 million program to upgrade and modernize IT and communications systems for the Australian Department of Defence (DOD). The enhancement will include service desk support for end users as well as workstations, VoIP and email upgrades, the implementation of new collaboration tools, and network infrastructure services and management.

Leidos has a 20-plus-year history serving clients in Australia, including the national government and provincial authorities, the nation’s healthcare sector, the intelligence community, and the country’s border defense agencies. In 2020 between 45% and 50% of Leidos’s $1 billion in overseas sales revenue derived from Australia. Leidos’ 2020 increase in international revenue, up 17.5% year-to-year, was driven largely by aggressive growth in Australia, and the company is primed for continued rapid expansion in the country and across APAC more broadly as Leidos leverages Australia as a staging point and case study for future regional expansion. The recent award with the Australian DOD comes on the heels of an AU$21 million contract with the agency for IT systems consolidation in 2020.

Leidos is also opening a new software development factory in Melbourne that will create 100 or more IT jobs and will be the company’s first such facility outside the U.S. — another sign the company expects steady growth in Australia for many years. In 2020 Australia Prime Minister Scott Morrison affirmed over AU$270 billion (about $190 billion) in new defense outlays over the next decade, including defense IT modernization and upgrades to weapons platforms. Australia’s relations with China have become increasingly strained in recent months, and government officials have also noted a sharp increase in regional economic and strategic instability. Leidos is ideally positioned to capture a large share of the expected budgetary investments to modernize defense platforms and civilian IT infrastructures.

Leidos’ Australian operations make the company relatively unique among top-tier federally centric IT integrators and professional services vendors, at least regarding the scale and tenure of its business in the ANZ region. Maximus provides business process management solutions, mostly employment services for the Australian government’s Disability Employment Services program, but the company has no presence in the Australian defense sector. Conversely, Raytheon Intelligence & Space (I&S) derives nearly 40% of its $19 billion backlog from international markets and 12% of its total revenue (about $800 million in 2020) from APAC (not exclusive to Australia), but does not provide traditional enterprise IT services to the Australian government or other foreign government clients in the region.

Leidos is among the 13 vendors covered in TBR’s quarterly Public Sector IT Services Benchmark and one of eight IT services companies primarily serving the U.S. federal government TBR analyzes in depth in semiannual reports featuring financial performance, go-to-market approaches, and alliance and resource management strategies. TBR’s Public Sector portfolio focuses primarily on IT services vendors’ work with U.S. federal government agencies. The international public sector market continues to attract investment from TBR’s covered vendors and remains an important, if small, revenue stream.

https://tbri.com/wp-content/uploads/2021/05/australia-62823_640.jpg526640John Caucis, Senior Analysthttps://tbri.com/wp-content/uploads/2021/09/TBR-Insight-Center-Logo.pngJohn Caucis, Senior Analyst2021-05-12 13:52:302021-05-12 13:52:30U.S. federal IT stalwart Leidos fortifies its foothold in Australia

5G represented a small portion of the overall PCN market in 2020, but is poised to rapidly scale in coming years

According to TBR’s estimates, 5G represented 8%, on average, of benchmarked companies’ private cellular network (PCN) revenue in 2020, with the rest being LTE. LTE remains the de facto technology for PCN, thanks to its maturity and vibrant ecosystem, which has been developed over the past decade. 5G for private networks, on the other hand, remains in its infancy, with key 3GPP Release 16 standards recently ratified, 5G spectrum gradually coming to market, compatible infrastructure commercialized and endpoint devices becoming available in the past year.

The endpoint device aspect of the nascent 5G ecosystem will begin to proliferate over the next couple of years, at which point 5G PCN implementations can be scaled commercially. In the meantime, most of the 5G engagements that occurred in 2020, with the notable exception of those in China, were focused on experiments and pilots, pending the commercial availability of compatible endpoint devices.

China has a significant head start with private 5G, with Huawei and ZTE equipping leading entities in the country, particularly the government, with the technology as part of national digitalization-related initiatives. Other developed APAC countries, namely South Korea, Japan, Taiwan and Singapore, are following closely behind China in 5G readiness.

Vendors’ PCN sales funnels are burgeoning

Vendors are experiencing significant and broad interest from enterprises and governments for how to leverage PCN for digital transformation-related initiatives. 5G is of particular interest, portending a strong growth profile through this decade.

Though 5G remains primarily in the exploratory phase, many of these engagements are likely to convert into commercial contracts over the next couple of years. In the interim, the bulk of PCN deal wins will be for private LTE networks.

TBR’sPrivate Cellular Networks Vendor Benchmarktracks the revenue key vendors obtain from the sale of LTE- and 5G-related infrastructure (includes RAN, core, transport and services provided for that infrastructure) to governments and enterprises, including large, medium and small non-CSP (telco, cableco, webscale) businesses. The benchmark ranks key private cellular networks vendors by overall revenue and by segment. Global market share and regional data and analysis are also provided.

https://tbri.com/wp-content/uploads/2021/05/Private-Cellular-Networks-Market-Share-2020.png484900Chris Antlitz, Principal Analysthttps://tbri.com/wp-content/uploads/2021/09/TBR-Insight-Center-Logo.pngChris Antlitz, Principal Analyst2021-05-11 10:23:122021-05-11 10:23:12PCN vendors poised for rapid growth as 5G ecosystem is built out

According to TBR’s December 2020Digital Transformation: Voice of the Customer Research, 61% of respondents indicate cloud computing is the leading technology they purchase as part of their central digital transformation (DT) initiatives. Over the course of the next five years, enterprises will continue to lead with cloud-first strategies — a trend that will be accelerated due to lessons learned from the COVID-19 pandemic. As customers move outside the data center, control over IT assets rapidly changes, as by no longer owning their hardware, customers can focus on data to drive innovation. Since cloud migration is the first step in unlocking data insights, Informatica is positioning its new solutions, most notably Intelligent Data Management Cloud (IDMC), as the foundation for true digital transformation. While maintaining strong ties to technical specialists, such as data scientists and engineers, Informatica’s ability to enable DT with a cloud-first approach positions the company to expand its applicability to nontechnical influencers and evolve its portfolio for a data-driven economy, which will be underpinned by cloud infrastructure.

By unifying data management with the cloud, IDMC will serve as the connection point for Informatica’s entire portfolio

Historically, Informatica’s Intelligent Data Platform (IDP) has underpinned much of the company’s core portfolio and provided customers a landing spot for their data management, integration, quality and security services. However, as cloud continues to dominate the technology landscape, Informatica’s strategy and market messaging are evolving to address customers’ challenges around storing data in the cloud. While leveraging the same underlying technology as IDP, IDMC takes data integration and management to the next level, offering customers over 260 services natively built into the platform, which can be deployed in the public or private cloud and consumed in a pay-as-you-go manner. Meanwhile, at the core of the platform remains Informatica’s embedded AI engine, CLAIRE, which acts as a system of record for metadata and helps customers derive insights across assets and product modules. The launch of IDMC reaffirms Informatica’s commitment to the cloud and modern applications, as IDMC serves as a complete replacement of IDP, which largely supported traditional software. Nonetheless, with a more scalable delivery model, the release mirrors the modular approach Informatica has always applied to data, offering customers choice and flexibility when it comes to the services that can be deployed on top of the platform, and their underlying data sources. For example, during the event’s opening remarks, Informatica Chief Product Officer Jitesh Ghai discussed how the company’s services are agnostic across infrastructures and data processing methods. An example of this impartiality is highlighted in services like Database Ingestion, which allows customers to take data residing in an Oracle database and move it into storage with an Azure data lake, for example. Informatica’s Data Integration service on IDMC is another example of how customers can leverage Informatica to integrate data across leading public clouds as an alternative to using three competing services from each cloud provider.

Supported by the cloud, Informatica’s platform services and capabilities meet customers’ specific business needs

Customer experience (CX) also remains the cornerstone of digital transformation efforts, and customers are adopting CX frameworks backed by emerging technologies, including AI and machine learning (ML) to complement their back-office operations. CX remains integral to Informatica’s strategy, evidenced by the January 2021 launch of Informatica Customer 360 as a SaaS solution. Customer & Business 360 is one of the core capabilities supported by IDMC in providing customers with a single-pane view of data across key business functions. Other capabilities of the platform that are in line with the main benefits of cloud computing include data discovery, ingestion, preparation, cleansing, records, delivery and governance. Throughout the event, one of the customer highlights was from Peloton (Nasdaq: PTON), a born-in-the-cloud company that has adopted IDMC to support its daily volume of roughly 10 million to 15 million records. Further, the New York State Department of Health adopted Informatica’s platform and leveraged the benefits of cloud-native analytics to support decisions and drive efficiencies during the height of the COVID-19 pandemic. Emphasizing data-driven business initiatives is a key gap IDMC aims to fill, as the platform not only supports customers’ IT initiatives, such as data engineering and warehousing, but also targets core business functions, such as e-commerce and finance. TBR suspects these core capabilities delivered through IDMC will provide Informatica with a strong competitive position, as the company unifies IT teams and line-of-business leaders through a cohesive data platform.

What would have been a large gathering in the heart of Las Vegas became Informatica’s biggest virtual event, which hosted over 10,000 registrants and featured talks from customers, partners and industry experts on their experiences with data and the critical role it is playing in the digital economy. Informatica World 2021’s theme of going from “Binary to Extraordinary” speaks to Informatica’s main announcement — the launch of its Intelligent Data Management Cloud — as the company looks to support a variety of data-centric use cases, which are positioned for success when built in the cloud. While Informatica’s neutral standing — as the “the Switzerland of data,” as CEO Amit Walia puts it — remains unchanged, a cloud-first approach positions the company to meet a unique set of challenges enterprises face in the cloud, regardless of underlying infrastructure or deployment method.

https://tbri.com/wp-content/uploads/2021/05/nasa-Q1p7bh3SHj8-unsplash-scaled-1.jpg17032560Catie Merrill, Senior Analysthttps://tbri.com/wp-content/uploads/2021/09/TBR-Insight-Center-Logo.pngCatie Merrill, Senior Analyst2021-05-07 10:48:552021-05-07 10:48:55At its customer conference, Informatica unifies cloud-agnostic data management

Testing smart city concepts, technologies and operations in a semi-confined setting

As detailed in TBR’s most recent Digital Transformation: Blockchain Market Landscape, maritime ports present an intriguing test bed for blockchain technology, given three intertwined elements essential to successful blockchain adoption. First, ports rest at the center of a diverse ecosystem, with players engaging directly on varying cadences, with different technologies and IT infrastructures and collaborative as well as competing needs — in short, a place messy and competitive enough to warrant a comprehensive solution to restrain complexity and digitize trust. (And if you do not believe ports can be messy, corrupt places, watch the second season of HBO’s “The Wire.”) Second, governments typically have a strong interest in port operations, either running them as quasi-governmental entities or regulating and overseeing them to advance national security and local and/or regional economic interests. For blockchain, as has been made clear in this report, government involvement can accelerate adoption. And third, with their diverse landscape of actors — shipping companies, trucking companies, freight forwarders, inspectors, stevedores, even local fire and rescue units — maritime ports are self-contained mini-universes, like small cities, a characteristic that pulls together the diverse ecosystem and government interest into a useful whole, for the purposes of blockchain.

As TBR noted previously, “The Port of Oulu has taken an approach shared by most municipalities looking to become a smart city — start small, but with a large, long, deep vision, and build incrementally … a port like Oulu’s, which is both small enough to be manageable through a disruptive digital transformation and large enough to be replicative of a larger port’s ecosystem and challenges, could be an ideal place for connectivity and emerging technology vendors to experiment and prove out the use case for bringing one of the most fundamental infrastructure environments fully into the digital age.”

Some blockchain consultancies have been experimenting with these ideas, as we noted here: “For EY, a firmwide approach to addressing every element of trade — including supply chain, tax and regulatory compliance, blockchain solutions, in-port IoT, connectivity to inland regions, and real-time shipping data — comes together under its NextWave Global Trade Initiative, a white space for EY to build cross-border, cross-service-line and cross-industry solutions.”

As is clear from both the Oulu and EY examples, blockchain can only be part of a port’s digital transformation, not the entirety of it. In line with the concept that a “rising tide lifts all ships,” connectivity, IoT and analytics round out the picture (cloud and cybersecurity should already be there), making blockchain an essential component, if not the most easily adopted or most transformational (arguably IoT sensors on every element of a port — with supporting analytics and insights — would more rapidly lead to streamlined operations, even if blockchain-enabled tracking and trade-based financing would lead to longer-term value).

Even recognizing the limitations, for blockchain services vendors, maritime ports may provide an essential opportunity to test solutions in diverse, yet manageable, ecosystems while partnering with governments or quasi-governmental institutions that will be critical to wider blockchain adoption. If the use case appears limited, consider the more than 50 ports that exist between Duluth, Minn., and the Atlantic Ocean. Blockchain-enabling that supply chain archipelago could be a massive use case and spark wider adoption across the enterprises interacting with every one of those ports.

For further details about blockchain in the context of digital transformation, IT services and consulting, see TBR’s most recent Digital Transformation: Blockchain Market Landscape, which includes use cases, vendor insights, and client pain points and needs.

https://tbri.com/wp-content/uploads/2021/05/shipping-4319421_640.jpg359640Patrick Heffernan, Practice Manager and Principal Analysthttps://tbri.com/wp-content/uploads/2021/09/TBR-Insight-Center-Logo.pngPatrick Heffernan, Practice Manager and Principal Analyst2021-05-07 09:00:002021-05-07 09:00:00Maritime ports serve as a natural test bed for blockchain ecosystems

Deal wins and investments in manufacturing suggest Infosys is anticipating a rebound in the vertical

With COVID-19 disrupting global supply chains and forcing participants to seek alternative channels to either reduce transaction costs by leveraging blockchain or transform IT infrastructure by migrating applications to cloud to offset technical debt and diminish financials pressure, some vendors have had the opportunity to gain a prime position. This includes Infosys, which has technology acumen and a low-cost presence and continues to go to market by industry vertical. During the first quarter of 2021, Infosys capitalized on these market dynamics, most prominently within the manufacturing vertical.

Infosys’ manufacturing sales declined significantly throughout 2020, with sales as a percentage of total revenue sliding 50 basis points to 9.5%, on average, in 2020 compared to 2019. However, in 1Q21 the company experienced strong momentum, illustrated by several deal wins, including with Siemens Gamesa Renewable Energy for SAP Business Suite 4 HANA (S/4HANA) implementation and with Johnson Controls to modernize the company’s smart global warranty solutions using the S/4HANA-ready SAP Fiori platform. Additionally, Infosys tested new ways to interact with clients to maintain trust and stickiness. The company also deployed Infosys Meridian, a collaboration platform that enables virtual events, including a four-day dealer engagement forum for Toyota Material Handling North America, which has been a client since 2018.

As COVID-19 continues to impede high-touch consulting opportunities and as auto shows — the main channel for the automotive community to interact — have essentially ground to a halt, testing innovative ways to interact with clients will benefit Infosys, provided the company captures feedback and applies lessons learned. Further, Infosys added $1 million to its 2016 investment of $1.6 million in the drone startup ideaForge as Infosys tries to diversify its manufacturing addressable market. Lastly, Infosys partnered with FourKites, gaining access to real-time tracking and visibility solutions and bolstering its supply chain capabilities, a necessary move as the company seeks to generate ongoing revenue growth in the manufacturing vertical.

Publishing in June, TBR’s latest IT Services Vendor Benchmark will include special detailed analysis of the changing ways IT services vendors are addressing new demands and digital transformations within the manufacturing sector.

https://tbri.com/wp-content/uploads/2021/05/car-doors-406883_1280-1.jpg8531280Bozhidar Hristov, Principal Analysthttps://tbri.com/wp-content/uploads/2021/09/TBR-Insight-Center-Logo.pngBozhidar Hristov, Principal Analyst2021-05-06 09:00:002021-05-06 09:00:00Infosys and manufacturing: Technology prowess, low-cost presence and innovative offerings

We may request cookies to be set on your device. We use cookies to let us know when you visit our websites, how you interact with us, to enrich your user experience, and to customize your relationship with our website.

Click on the different category headings to find out more. You can also change some of your preferences. Note that blocking some types of cookies may impact your experience on our websites and the services we are able to offer.

Essential Website Cookies

These cookies are strictly necessary to provide you with services available through our website and to use some of its features.

Because these cookies are strictly necessary to deliver the website, refusing them will have impact how our site functions. You always can block or delete cookies by changing your browser settings and force blocking all cookies on this website. But this will always prompt you to accept/refuse cookies when revisiting our site.

We fully respect if you want to refuse cookies but to avoid asking you again and again kindly allow us to store a cookie for that. You are free to opt out any time or opt in for other cookies to get a better experience. If you refuse cookies we will remove all set cookies in our domain.

We provide you with a list of stored cookies on your computer in our domain so you can check what we stored. Due to security reasons we are not able to show or modify cookies from other domains. You can check these in your browser security settings.

Other external services

We also use different external services like Google Webfonts, Google Maps, and external Video providers. Since these providers may collect personal data like your IP address we allow you to block them here. Please be aware that this might heavily reduce the functionality and appearance of our site. Changes will take effect once you reload the page.

Google Webfont Settings:

Google Map Settings:

Google reCaptcha Settings:

Vimeo and Youtube video embeds:

Privacy Policy

You can read about our cookies and privacy settings in detail on our Privacy Policy Page.