With TBR’s Telecom market and competitive intelligence research, examine telecom operator and telecom vendor markets as well as key industrywide trends and developments, such as 5G, edge computing, private networks, and the encroachment of hyperscalers into the telecom industry.

Understand operator business models, capital expenditure, subscriber metrics and next-generation technology adoption, with coverage spanning wireless, wireline, cable and enterprise markets. Access vendor customer demand analysis, portfolio analysis and competitive benchmarking.

Additionally, we are the leading resource for telecom infrastructure services (TIS) market research.

A free trial of TBR’s Insights Center platform gives you access to our entire Telecom research portfolio and the ability to customize and curate reports detailing our analysis based on your company’s specific needs. Start your free trial today!

Trends we’re watching in 2026:

- Impact of K-shaped economy on telecom market

- Why a price war is coming to the broadband market

- How telcos will adjust to meet AI’s timetable

- Ways in which the network needs to adjust for the AI economy

Explore TBR Telecom Coverage

Market & Competitor Benchmarks

Market and competitor benchmarks provide a comparison of vendor performance in a market, including analysis on vendor strategies, financial performance, go-to-market and resource management. The research graphically portrays comparisons of vendors by myriad metrics, calling out leaders, laggards and business models. Defensible, data-informed views of market opportunity and operational best practices are highlighted in each publication. TBR also provides benchmark data in Excel pivot tables.

Current Market & Competitor Benchmarks:

- Private Cellular Networks Vendor Benchmark

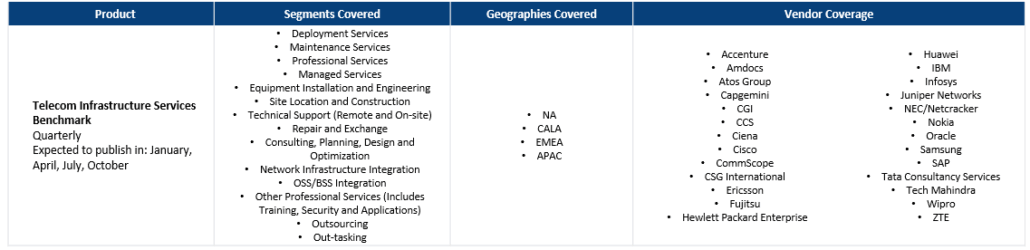

- Telecom Infrastructure Services Benchmark

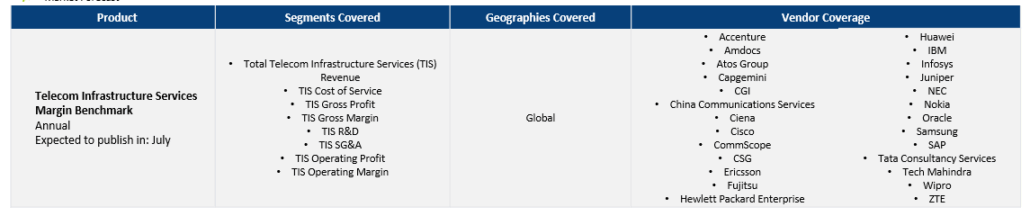

- Telecom Infrastructure Services Margin Benchmark

- U.S. Mobile and Broadband Operator Benchmark

- U.S. B2B and Public Sector Telecom Operator Benchmark

Market Forecasts

Market Landscapes

TBR’s vendor reports, snapshots and profiles provide deep-dive analysis of a single vendor across corporate strategies, tactics, SWOT analysis, financials, go-to-market strategies and resource strategies. Vendor performance is put in the context of market opportunity and competitive environment and our assessment shows where a vendor will success and its future market position.

Telecom

- AT&T

- Cisco Systems

- T-Mobile USA

- Verizon

- Ericsson

- Nokia

")

Ready to Level Up Your Insights?

TBR’s digital-first competitive intelligence platform, TBR Insight Center™, allows for configured & customized views into IT markets, vendors, alliances and ecosystems.

Benefits delivered through TBR Insight Center™ include:

- Dynamic, configurable platform for TBR’s objective, independent and validated data and analysis

- Customizable views of millions of data points to match your specific needs

- Simple download functionality for customized views of analysis and feeds of data, saving staff dozens of hours per month

- Updates for market disruptions and emerging trends

- All data found in Insight Center can be leveraged to power your company’s AI tool via an API feed

Already a TBR Classic client but don’t have access to TBR Insight Center yet? Request access today.

AMD Enters the Execution Phase of its Full-stack AI Strategy

/by Ben Carbonneau, Senior AnalystAdvancing AI 2026 showed that AMD has assembled the architecture and road map required to compete at rack scale. Helios connects the company’s GPUs, CPUs, networking and software into a system-level platform, while expanding partnerships with Microsoft, OpenAI, Anthropic and Meta provide credible paths to large deployments. ROCm.ai gives AMD a new way to reduce the engineering effort required to bring up and optimize applications on Instinct GPUs. Agentic workloads also expand the AI-driven opportunity for EPYC beyond its role as a host CPU for accelerators, allowing AMD to address the agent sandboxes, applications, databases and data services surrounding GPU inference.

Hidden Costs of AI Market Intelligence

/by Dan DemersThe enterprises that succeed will not be those that provide unrestricted AI access to every employee. The winners will build trusted intelligence architectures enabled with proprietary, non-public data and analysis that prevent organizations from paying thousands of times for the same expensive thought. The future of enterprise AI is not simply broader access. It is governed intelligence aligned to enterprise strategy, with CFO approved efficiency. And increasingly, that efficiency may prove more valuable than the AI models themselves.

Global Analyst Summit 2026: Value Creation Through Operating Model Transformation

/by Kelly Lesiczka, Senior AnalystAs consulting continues to evolve due to AI’s influence on business models and day-to-day operations across enterprises, EY’s leaders discussed how the firm is adapting its approach to guide clients through uncertainty and increased speed of change, and introduced featured clients, giving them an opportunity to share their experiences. The client stories emphasized the speed at which they need to navigate market changes and their desire to work with a long-term partner such as EY to guide the transformation as well as to create an ecosystem of vendors that support their end goals. The notion of value was consistent throughout the event, as the firm seeks to reconfirm its positioning in the consulting space despite ongoing market uncertainty about consulting’s future relevance.