The Race for Digital Sovereignty: How 4 IT Services Leaders Are Positioned

TBR Fourcast is a quarterly blog series examining and comparing the performance, strategies and industry standing of four IT services companies. The series also highlights standouts and laggards according to TBR’s quarterly revenue projections as well as its geographic and segment estimates. With discussions about sovereignty in Europe only becoming louder, TBR thinks it is worthwhile to examine Atos Group, CGI, Fujitsu and Kyndryl. Our intent is to shine light on these similarly sized companies that have a strong presence in Europe and/or a strong presence in ITO and consulting and to discuss where each company’s opportunity lies.

Who will secure and defend market share in sovereignty in Europe?

In the sixth iteration of the Fourcast Blog, we examine the sovereignty market in EMEA across Atos Group, CGI, Fujitsu and Kyndryl.

Atos Group and Kyndryl share a similar motivation to pursue and expand sovereign capabilities. Atos Group is reducing its low-margin infrastructure services contracts and focusing on three target areas to improve revenue growth and regain market share: mission-critical agentic AI, digital sovereignty and cybersecurity. Similarly, Kyndryl aims to reduce the share of its low-margin infrastructure services contracts inherited from IBM and seeks deals in hybrid cloud, cybersecurity and agentic AI.

CGI and Fujitsu are both concentrating on scaling their global presence. Specifically, CGI is expanding its presence in Europe, and TBR predicts the company will enhance its sovereign capabilities in the second half of 2026 and in 2027. Similarly, Fujitsu has begun increasing its sovereign capabilities in Europe as it pushes to expand beyond Japan.

As sovereignty becomes an enabler for deals such as agentic AI and application modernization, developing the right solutions and go-to-market approach, while challenging established players such as Atos Group, will be a key battle in the coming years. The companies that most effectively combine sovereign solutions with IT consulting, hybrid cloud, secure infrastructure and AI governance and management expertise will be best positioned to defend existing accounts and capture new opportunities across Europe.

CGI is becoming a stronger rival to Atos Group. What now?

Five years ago, Atos Group’s trailing 12-month (TTM) EMEA revenue was approximately twice CGI’s revenue in the region, with Atos Group at $9.6 billion in 1Q21 compared to CGI’s $4.7 billion. Although Atos Group is historically a larger and more established company in EMEA, CGI has significantly expanded revenue in the region through selective acquisitions to build its geographic footprint. CGI focuses on underpenetrated regions and metro markets, including the Nordics and Baltics. CGI acquired Comarch Polska SA, expanding its presence in Poland and the Baltic states, with visible impacts in areas such as infrastructure services and consulting and systems integration (C&SI).

The company has announced a slew of engagements in the region during 2026, including a deal with the Finnish National Agency for Education, Stockman, Telia and Posti, all based in Finland. CGI is, in part, evading direct competition in the sovereign market to expand its revenue share; in contrast, Atos Group is focusing on its largest core geographies, such as France, U.K. & Ireland, and Germany, Austria & Eastern Europe, which collectively accounted for 53% of revenue in 1Q26. Atos Group’s renewed focus on its core territories will make it a greater threat to CGI in these regions.

CGI maintains a strong presence in Europe and France, Atos Group’s home territory. Although both companies now have similar revenue levels, CGI is not straying from expanding into France’s highly penetrated market. Last August, CGI completed the acquisition of Apside, a digital and engineering services firm headquartered outside of Paris with 2,200 employees in France and approximately $250 million in revenue.

However, the biggest challenge will be overcoming Atos Group’s established brand reputation in Europe. Atos Group’s long-standing work with commercial clients and public sector organizations such as the European Union (EU), national governments, NATO, EU cybersecurity bodies and municipalities has created a level of trust CGI will struggle to replicate. Atos Group’s work on sovereign AI platforms, critical infrastructure cybersecurity testing and emergency management systems reinforces its compliance expertise and operational credibility.

Recently, Atos Group launched its Digital Sovereignty offering, Threat Research Center, and Atos Sovereign Agentic Studios, signaling its push to embed AI-driven cybersecurity into enterprise operations, enhancing its revenue growth opportunities and resiliency. For these reasons, TBR believes Atos Group will be able to defend its turf in EMEA, despite its TTM EMEA revenue declining year-to-year since 1Q22. Long-term growth will depend on Atos Group’s ability to industrialize AI-led offerings, convert consulting capabilities into scalable revenue, and differentiate through sovereignty and systems integration rather than relying solely on innovation.

CGI is no stranger to mission-critical environments, but Atos Group is more explicitly tied to cybersecurity and sovereignty in mission-critical environments related to national security and defense. TBR believes CGI’s portfolio may be less developed in this regard. CGI emphasizes embedded capabilities, whether AI, security or other, as part of larger contracts that support clients’ needs holistically rather than with a one-size-fits-all solution.

CGI announced a sovereign AI and data services platform in Finland called KATAKRI that complies with local regulations. The platform runs on CGI’s hybrid service on a certified data center within the country, intended for classified and other sensitive workloads. TBR anticipates CGI will expand its sovereign capabilities, prioritizing underpenetrated regions. In this regard, it will be difficult for CGI or any competitor to completely shake Atos Group’s grip on France.

Where does Atos Group go from here?

TBR anticipates the company will double down on refining its portfolio to focus on what it does best — mission-critical cybersecurity and IT services — and will expand in its high-value and high-growth target areas, including mission-critical agentic AI, digital sovereignty and cybersecurity. Second, the company has a new corporate brand and national communications campaign in France.

As described in the 1Q26 Atos Group report, “The campaign supports Atos Group’s objective to rebuild client, investor and employee confidence while clarifying the relationship between the Atos (services) and Eviden (products) business lines. The new Accelerating Intelligence tagline supports the company’s positioning around AI-powered, sovereign- and cybersecurity-focused transformation services. The branding effort reflects Atos Group’s recognition that restoring commercial momentum requires more than operational restructuring and cost reduction.”

All roads lead to consulting

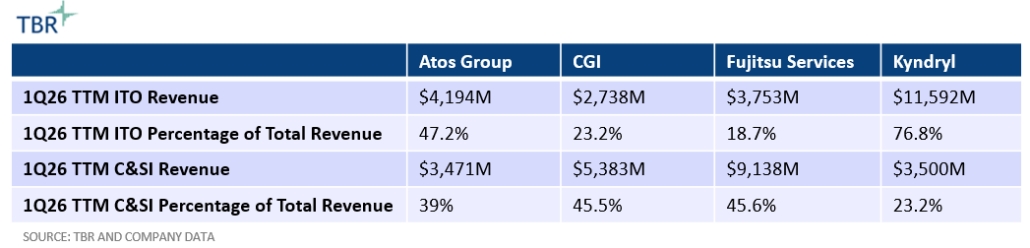

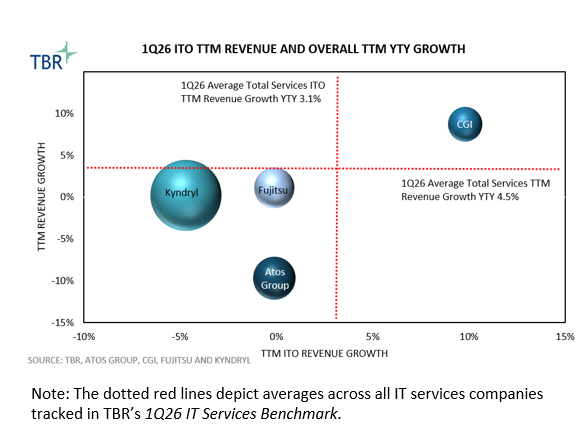

According to TBR’s proprietary data, Atos Group and Kyndryl have the largest ITO segments among the four companies. Further, ITO accounts for the largest revenue share for Atos Group and Kyndryl. ITO resources are foundational in sovereign delivery because they include cybersecurity teams, sovereign technology and dedicated managed infrastructure teams. In many ways, cybersecurity and sovereign demand have revived sluggish growth in the segment.

According to TBR’s IT Services Benchmark, TTM ITO revenue growth declined for seven consecutive quarters before rebounding in 4Q25 as these deals were realized. We expect the two companies’ presence in ITO, along with their portfolios of managing mission-critical environments, to provide a competitive advantage. As with Atos Group and CGI, Kyndryl has launched key solutions such as Kyndryl Sovereignty Solutioning, a suite of advisory, implementation and managed services. TBR believes this reflects the company’s focus on addressing data sovereignty, regulatory compliance and business continuity requirements.

Kyndryl also launched its first Cyber Defense Operations Center in India, a command hub that combines network operations and security operations, and the Kyndryl Intelligent Recovery Service, both of which indicate a shift toward making cyber resilience and recovery a central, differentiated capability as regulatory and operational pressures mount.

Despite improved performance in ITO currently, Atos Group and Kyndryl have been pivoting to consulting, in part to capture higher-value, higher-margin opportunities. Atos Group has formalized its consulting efforts by introducing Atos Amplify, a new unified and AI-powered consulting business unit. Similarly, Kyndryl is scaling Kyndryl Consult to shift toward higher-value transformation work rather than relying on legacy infrastructure outsourcing services. Kyndryl Consult’s revenue share has improved to approximately 23% of revenue in FY26, up from 19% of revenue in FY25, supported by AI modernization, cloud and cybersecurity.

By embedding AI into Kyndryl Consult, the company is moving to higher-value advisory and transformation services. Atos Amplify and Kyndryl Consult support a more comprehensive delivery strategy and will improve profitability for both companies.

Fujitsu is also expanding its consulting profile through Uvance, its consulting segment that addresses enterprise societal challenges, to drive revenue growth and broaden project scope. Although Uvance typically focuses on advisory services, Fujitsu is positioning itself around sovereignty to gain market share in Europe. Fujitsu recently introduced Digital Sovereignty Advisory Services, encompassing cybersecurity assessment and related security services concentrating on compliance with recent regulations for organizations in Europe.

Although a follower in sovereignty compared to peers such as Kyndryl and Atos Group, Fujitsu is well-equipped in certain pockets of Western Europe, leveraging its experience with Japan’s similar security initiatives and industry expertise. For example, Fujitsu is manufacturing sovereign AI servers as it adapts its focus in light of Japan’s Economic Security Promotion Act. Like CGI, TBR views Fujitsu’s messaging strategy and deal engagement as focused on holistic client outcomes, which makes its sovereign services slightly less visible.

Among the four companies, CGI and Fujitsu generate the most revenue from consulting and systems integration, segments that Atos Group and Kyndryl are trying to scale. While TBR expects CGI and Fujitsu to remain dedicated to consulting in EMEA, it raises the question: Why would CGI and Fujitsu also want to delve into the typically lower-margin ITO market?

The answer is twofold. First, increasingly complex infrastructure and digital landscapes, driven by new regulations, the advent of AI and rapidly changing macroeconomic environments, create more opportunities for consulting-enabled transformational engagements (along with enhancing their service quality). Second, for Atos Group and Kyndryl, consulting will help drive contracts in sovereignty and cybersecurity as environments become more complex.

What is the future direction of sovereignty?

The sovereignty boom will be important over the next two to three years, but can those with more revenue and dedication to ITO, like Atos Group and Kyndryl, survive in the long run on this new demand? After all, the wave of cybersecurity and sovereignty is acting like a life raft for ITO. One answer is to leverage growing geopolitical uncertainty to expand consulting, but what about when that uncertainty is no longer a concern too?

If Atos Group and Kyndryl successfully build out larger consulting arms, how will they use them in the future? TBR believes these types of sovereign environments and heightened scrutiny of cybersecurity practices will be around for the long haul; if anything, it was a long time coming. Where Atos Group and Kyndryl may have value is providing broader C&SI engagements, such as change management with AI and cybersecurity practices on the ground, as well as integrating next-generation technologies in mission-critical environments across heavily regulated industries, such as the public sector, financial services and healthcare.

What does this mean for Fujitsu and CGI? TBR believes their freshly built-out sovereign and cybersecurity capabilities will enhance service quality and secure their position in consulting in Europe. If CGI and Fujitsu did scale ITO more significantly, TBR could see some added resources and capabilities eventually phased out slightly once sovereign solutions reach maturity, as the two companies will opt to stay true to their consulting roots.

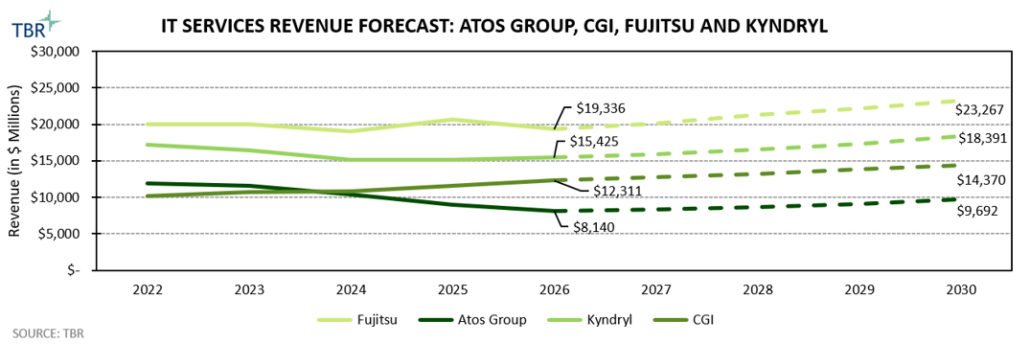

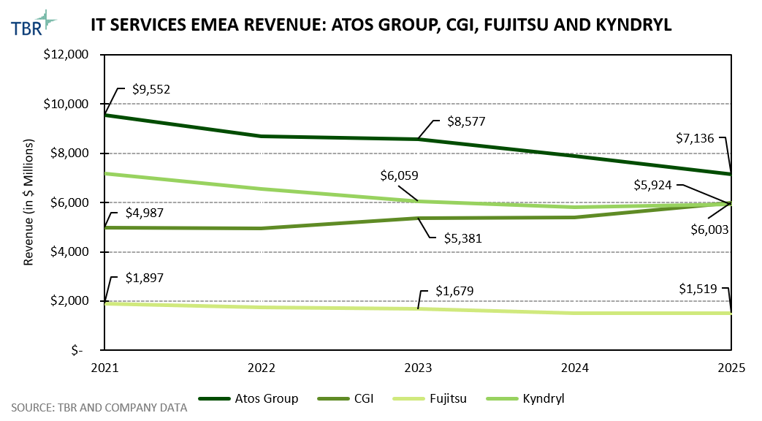

The IT Services Revenue Forecast graph below shows TBR’s total revenue projections for the four companies. Notably, CGI surpassed Atos Group in 2024, but we expect Atos Group’s revenue to rebound in 2028, with Fujitsu continuing to lead through 2030. In the second graph, we present historical data for each company, using TBR’s proprietary taxonomy, beginning in 2021 to provide a five-year view. CGI’s and Atos Group’s EMEA revenue converged from 2022 onward, and CGI’s revenue exceeded Kyndryl’s for the first time in 2025. Fujitsu’s EMEA revenue increased from $5.8 million in 2024 to $5.9 million in 2025.