Getty Images, via Canva Pro

Getty Images, via Canva ProWill C&SI Revenue Growth Accelerate Significantly Due to AI Adoption at Scale?

In 2025 the total consulting and systems integration (C&SI) market reached $556 billion, growing 4.9% year-to-year, with the top five vendors contributing roughly a quarter of total market revenue. The C&SI market among the 18 vendors tracked in TBR’s Consulting & Systems Integration Market Forecast reached $247 billion, up 2.9% over the same period. The main growth drivers were technology adoption and optimization-related business transformation.

Although clients tightened budgets in 2025 and thus far in 2026, they engaged in smaller projects around technology adoption and implementation. In 2030 the total C&SI market is estimated to reach $739 billion, reflecting growth of 4.4% year-to-year ($302 billion for the tracked 18 vendors, up 4.3%), slower than 2025, as the nature of consulting projects will change. Underpinning consulting with technology solutions and tools will create new projects but reduce the value of contracts, resulting in slower market growth. At the same time, investment in talent will be needed to ensure vendors can execute on consulting-led projects related to advanced technology solutions.

Watch TBR Insights Live webinar on demand: “IT Services Market Outlook: Forecasting Growth, AI Impact and Competitive Shifts Through 2030”

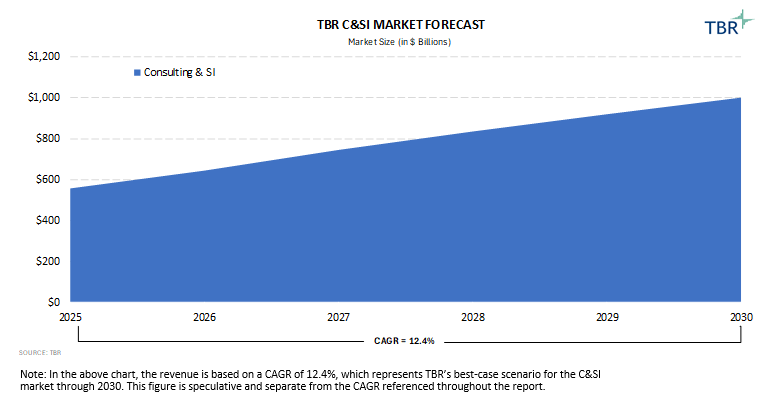

Consulting and systems integration market best-case scenario

Accelerated adoption of AI at scale by the companies included in this market forecast, combined with increasing demand from clients to map out, implement and support AI-enabled solutions, could cause C&SI revenue to grow much faster than the single-digit rate projected in TBR’s baseline forecast.

Nearly all IT services companies and consultancies have adopted a customer-zero approach to emerging technologies. With enough experience and scale, they should move into the latter half of the 2020s with compelling use cases for clients and opportunities to benefit from their internal AI adoption.

Maturing AI use cases and next-generation AI-enabled solutions, such as agentic AI, will likely be less horizontal in nature and much more industry-specific. With very few exceptions, IT services companies and consultancies orient themselves and their offerings around industries, making the AI play to their strengths. Not every IT services vendor or consultancy can lead in every industry, so separation may come as certain vendors capture increasingly larger shares of an industry’s AI-specific C&SI needs. Every vendor can serve the largest IT-buying industries like financial services and healthcare, making true differentiation more about subindustries and, perhaps, slower AI adopters.

C&SI Market Forecast for 2025 through 2030 (Source: TBR)

Growth leaders will guide technology adoption and management with a focus on delivering outcomes and creating value

2030 market leader expectations

Laggards in 2030 will move into positive revenue growth positioning, but their growth potential will be mixed. Two main market changes will influence the slower growth rates in 2030. First, the shift to outcomes-based and fixed-price contracts will reduce total contract value despite the expansion of technology projects, resulting in lower revenue growth tied to consulting and higher revenue growth from managed services. Second, more niche consulting firms continue to emerge in the market. Although these firms target smaller enterprises than the larger vendors, these niche consulting firms will challenge traditional vendors. Growth opportunities will be focused on technology-led transformation as well as business consulting to improve operations following larger-scale transformation projects. SI services will likely remain in-house for traditional IT services vendors, such as the India-centric firms, helping solidify the image of transformation partners.

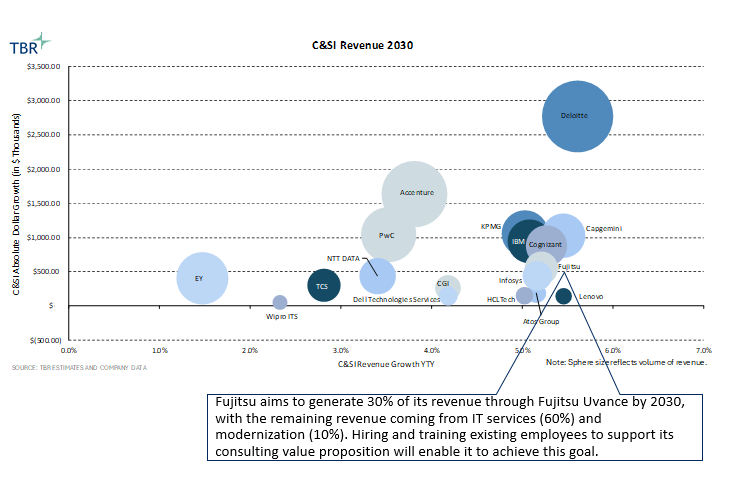

C&SI Revenue Projection for 2030 (Source: TBR Estimates and Company Data)

AI adoption and outcomes-based commercial models will reshape the traditional C&SI space and push IT services companies and consultancies to identify new areas of value and differentiation

TBR’s Consulting & Systems Integration Market Forecast is a comprehensive view of vendor activity and investment across the market. The research includes estimates for total market size, growth and trajectory, and highlights best- and worst-case scenarios for the market.

The first publication of this new research explored key market insights such as:

- Clients will increasingly require fixed-price and outcomes-based billing models. By 2030, 85% of engagements will feature new commercial models, and the remainder will be split between time & materials and software sales.

- The cannibalization of the traditional consulting model due to AI will lower contract values, requiring vendors to find new methods of growth such as in managed services, security and operations.

- Specialization strategies related to talent, business models and portfolios will define laggards and leaders. The need for blended technology and traditional consulting skills will accelerate.

- Although it is not an immediate threat, the emergence of niche consultants could pressure vendors and their ability to charge high prices.

The first publication of this annual report is now available. Click here to Learn how you can access the full research and all supporting data.

Technology Business Research, Inc.

Technology Business Research, Inc.

Elnur, via Canva Pro

Elnur, via Canva Pro Maxim Basinski, Vasabii via Canva Pro

Maxim Basinski, Vasabii via Canva Pro Alemedia.ID via Canva Pro

Alemedia.ID via Canva Pro Getty Images, via Canva Pro

Getty Images, via Canva Pro Alemedia.ID, via Canva Pro

Alemedia.ID, via Canva Pro