Top 3 Predictions for Telecom in 2022

Telecom industry faces new challenges in the post-pandemic era

2022 will be a transition year for the telecom industry

After emerging from the COVID-19 pandemic relatively unscathed, the telecom industry is entering a new phase and faces a new set of challenges. These challenges include navigating a supply chain left in shambles due to the impact of the pandemic and, representing a separate concern, the inexorable rise and encroachment of hyperscalers in the telecom domain, which threatens to completely disrupt the status quo in the industry.

Incumbent communication service providers (CSPs) and their vendors are navigating these issues, but there is an increased urgency to digitally transform and align with structural changes occurring in the industry, such as the pressure to work with hyperscalers on network transformation and business model co-creation in the cloud.

2022 is poised to be a unique transition year for the telecom industry. While unprecedented government stimulus that originated in the wake of the COVID-19 outbreak continues to be pumped into the global economy, lifting all players in some way across the market landscape, CSPs and their vendors must transition to the fundamentally new network architecture, which is software-based, fully virtualized and cloud-centric. CSPs must also determine where they will play in the new value chains that are being created in the digital economy, most notably in hyperscalers’ marketplaces, and in conjunction with new players that are entering the scene in domains such as private networks and satellites.

Meanwhile, supply chain challenges are expected to persist through 2022, with continuing semiconductor and component shortages as well as ongoing skilled labor deficiencies and shipping delays, all of which threaten to delay market development and hinder vendors’ ability to recognize revenue and pursue new growth opportunities. Inflation (potentially stagflation) and rising interest rates also pose risks, portending margin pressure and debt refinancing challenges.

Taken together, these circumstances indicate 2022 will be an unusual year for the telecom industry. While government-induced stimulus will provide various benefits to players across the industry, giving off a sense that the industry is functioning normally and is healthy, an acceleration in competitive and technological changes poses a risk to the long-term performance of incumbents. Amid the uncertainty 2022 will bring, one thing is certain: Major changes are coming to the telecom industry in the post-pandemic world, and fast.

2022 telecom predictions

- Supply-demand imbalance delays pace of 5G market development

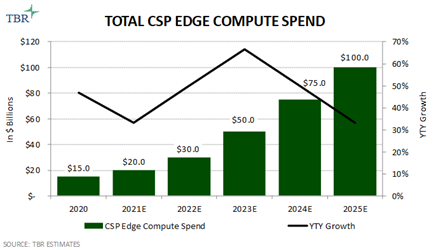

- Hyperscalers scale out edge cloud

- Government becomes leader in 5G spend among nontelecom verticals

Download a free copy of TBR’s Top 3 Predictions for Telecom in 2022

Telecom Business Research’s 2022 Predictions is a special series examining market trends and business changes in key markets. Covered segments include cloud, telecom, devices, data center, and services & digital.