TBR Fourcast is a quarterly blog series examining and comparing the performance, strategies and industry standing of four IT services companies. The series also highlights standouts and laggards, according to TBR’s quarterly revenue projections. This quarter we are looking at Accenture, Deloitte, IBM Consulting and Infosys, including Accenture’s extensive investment in GenAI and IBM Consulting’s and Infosys’ risk of falling into a downward trajectory.

Vendors Ramp Up Optimization and Operational Efficiency Projects Amid Revenue Deceleration from Tight Client Discretionary Spending

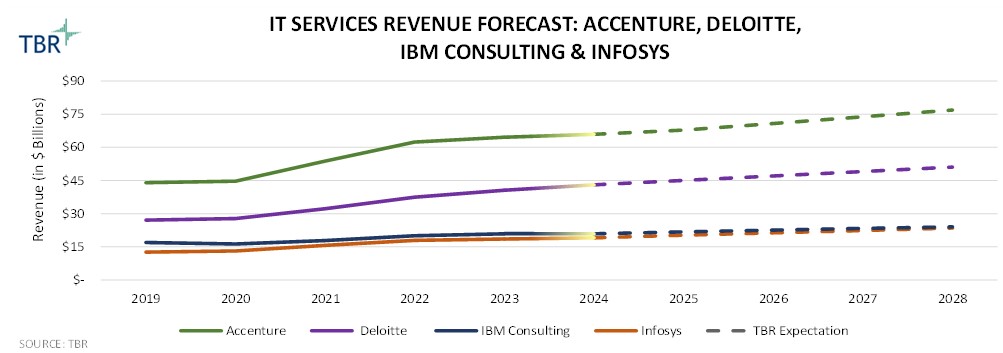

IT services vendors currently face client discretionary spending headwinds, resulting in increasingly long decision cycles. According to TBR’s IT Services Vendor Benchmark, year-to-year revenue growth for the 31 vendors decelerated from 13.8% in 1Q19 and 8.6% in 1Q22 to 2.1% in 1Q24.

In response to these headwinds, Deloitte, IBM Consulting and Infosys are slowing their hiring pace and focusing on reskilling and upskilling existing professionals. Accenture will likely follow suit, although it currently maintains its skills-based hiring approach. A closer look shows that Accenture has started slowing organic hiring, but acquisitions are helping the firm offset some of the headcount growth deceleration. As part of its resource management strategy, Accenture is rotating the skills composition of its workforce with the goal of maintaining a large enough bench to meet booked demand while ensuring quality (bookings increased 22.1% year-to-year to $21.1 billion in FY3Q24, putting Accenture on track to reach $80 billion during FY24).

As discussed in detail in TBR’s quarterly reports, Accenture and Deloitte are expected to have uneven revenue growth through the remainder of 2024. Amid persistent macroeconomic uncertainty, every IT services company and consultancy is reporting greater customer interest in digital transformation and projects centered on cost optimization and operational efficiency. According to TBR’s December2023 Digital Transformation: Voice of the Customer Research, “Improving IT operations remains the top DT [digital transformation] initiative for most buyers, but this objective is reaching maturity as more buyers are in the true Transformation stage and are now focusing on extracting benefits from existing assets.”

Investments in Industry Expertise and GenAI Will Position Vendors for Growth in the Market

Not surprisingly, IT services companies are investing in generative AI (GenAI) and industry expertise to capitalize on growth opportunities as they must demonstrate knowledge in both of these areas to stand out among competitors.

In TBR’s view, Deloitte and Accenture have invested extensively in industry expertise and GenAI compared to other vendors and have done well in marketing themselves as leaders, helping them better position for near-term growth in demand for operational efficiency and longer-term opportunities around GenAI governance. Deloitte’s broad portfolio and training investments closely align with many of its IT services peers, which is not surprising, given the firm’s position within the value chain.

To differentiate, Deloitte’s release of industry use cases as a thought leadership platform is a striking contrast to the approach of its most immediate rival, Accenture, suggesting Deloitte will stay true to its industry-wrapped, consulting-led value proposition. Accenture’s release of its useful “switchboard” tool, which helps clients select the best foundational model for their needs, aligns well with Accenture’s technology heritage.

Similar growth pathways are not out of reach for IBM Consulting and Infosys. The former could utilize tuck-in acquisitions to drive specialization and continued collaboration with technology partners and academia to support portfolio build-out and strengthen its position in the market. At the same time, IBM Consulting could leverage hybrid cloud and AI solutions, its incumbency with clients, and its ability to deliver small and large projects at scale to expand wallet share. Meanwhile, Infosys will continue to execute on its strategy to pursue large-scale deals as the company recalibrates and enhances its portfolio offerings to address buyers’ needs. The recent acquisitions of InSemi and in-tech highlight Infosys’ efforts to add skills and capabilities in areas such as chip design and product engineering, supporting the company’s goals of expanding wallet share and capitalizing on its existing relationships while gradually drifting away from commoditized portfolio areas.

If Vendors Fall, They Will Fall for Different Reasons but Will Have Similar Outcomes

What Could Go Wrong?

In the worst-case scenario, IBM Consulting’s and Infosys’ revenue could begin to take a negative trajectory for similar reasons: drifting away from hybrid cloud and AI (IBM Consulting) and away from services in pursuit of GenAI-related software licensing sales (Infosys).

Unsurprisingly, Deloitte could face quality issues related to its overemphasis on growing the firm’s IT services offerings. In contrast, according to TBR’s 2Q24 Accenture report view, an Accenture slide could come from accelerated GenAI adoption, pressuring “Accenture’s legacy applications and business process management services so much that it cannibalizes revenue to a greater extent than originally anticipated.”

For all four vendors, a loss of trust could lead to client retention issues, which would accelerate any downward momentum. To be clear, TBR does not expect any of these companies will experience their worst-case scenarios, but the market pressures and potential for strategic mistakes remain entirely real.

Conclusion

TBR expects IBM Consulting will be the growth leader among this foursome yet will likely continue to trail the overall IT services market, absent a massive GenAI-induced upheaval. Accenture and Deloitte continue to be best positioned to outperform TBR’s projections, although Infosys has been a surprisingly strong player in the market over the last couple of years, reflecting its strong leadership.

To access years of full analysis and proprietary TBR datasets for Accenture, Deloitte, IBM Consulting and Infosys, sign up for your TBR Insight Center™ free trial today!

https://tbri.com/wp-content/uploads/2024/09/network-technology-information-data_liulolo_getty-images_canva-pro.png10801080Jill Cookinhamhttps://tbri.com/wp-content/uploads/2021/09/TBR-Insight-Center-Logo.pngJill Cookinham2024-09-30 09:52:462024-09-30 09:52:46IT Service Vendors Shift Focus to Operational Efficiency and GenAI Investments Amid Economic Uncertainty

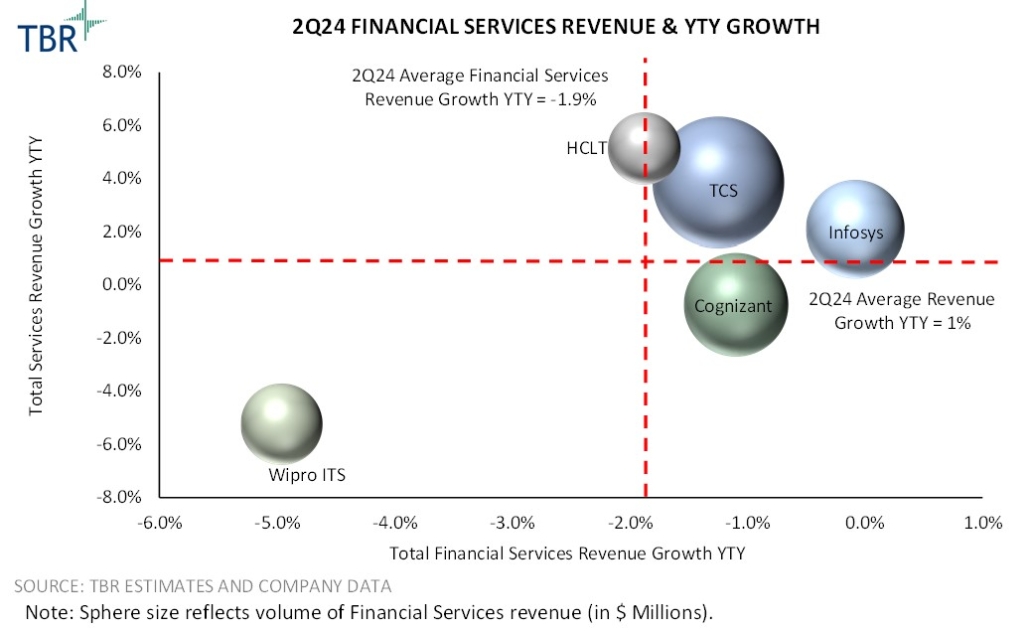

In late 2023 and thus far in 2024, the companies within TBR’s IT Services coverage faced pressures within their respective financial services practices, experiencing industry declines from a revenue perspective as higher interest rates limited opportunities and hindered growth trajectories.

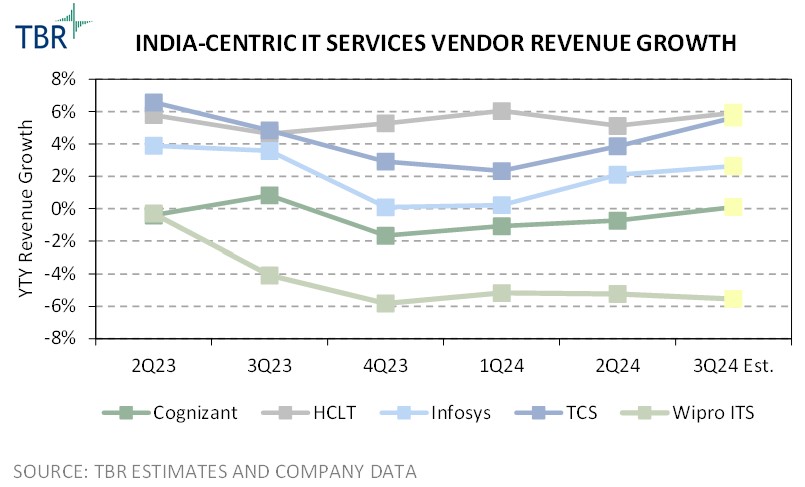

The India-centric vendors TBR covers — Cognizant, HCLTech, Infosys, Tata Consultancy Services (TCS) and Wipro IT Services (ITS) — experienced these financial services revenue declines, despite their efforts to embed automation, AI and efficiency-driven services.

The five vendors experienced mixed performance in terms of overall revenue in 2Q24 and pursued varying portfolio expansions and strategy directions. Growth leaders HCLTech, Infosys and TCS have benefited from demand for cloud migration, application management and digital services, which helped to offset declines in financial services revenue. Digital services enabled by innovation-led frameworks remain an important sales engine for Infosys, helping the company build a foundation for future performance.

While HCLTech also leverages Digital Workplace Services, the company’s engineering expertise provides an avenue of differentiation as well as relationship building through developed infrastructure and solutions. HCLTech’s integration of its Engineering and R&D Services sales with its IT and Business Services practice enables the company to better address demand for transformation services that stretch across multiple segment groups, driving value creation.

Meanwhile, demand for next-generation solutions across connected plants, connected services and intelligent product engineering is boosting TCS’ Digital Transformation Services revenue.

Revenue growth for both Cognizant and Wipro ITS was more sluggish during 2Q24 as the companies struggled to capture new opportunities amid limited discretionary spend. Cognizant is experiencing longer contract periods from larger engagements, which extends the revenue generation but leads to smaller pockets of revenue recognition. Wipro is in a slightly more precarious position as it appoints new leadership and establishes new strategic directions. While the investments and leadership transitions will help Wipro evolve its portfolio, the company will continue to struggle to accelerate revenue growth and expand market presence.

Financial Services

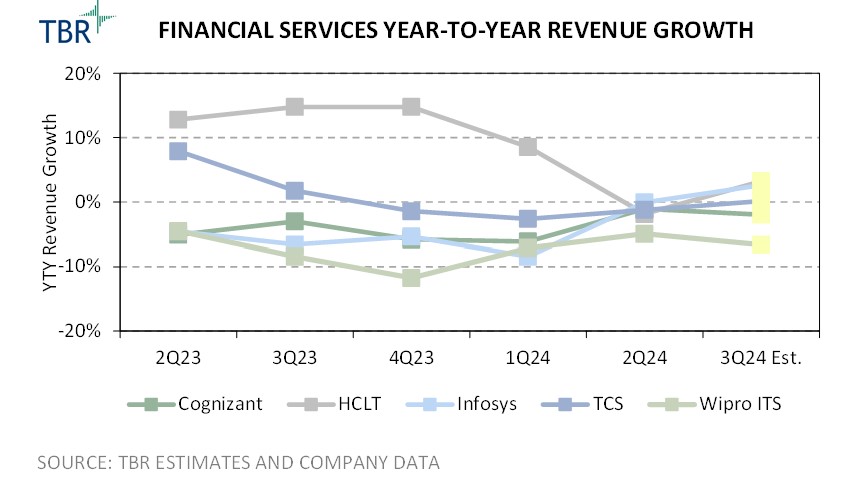

For the India-centric IT services vendors, financial services revenue performance has been hit harder relative to overall revenue as the macro environment remains challenged. Inflation rates, higher interest rates and ongoing economic uncertainty have pushed financial services companies, primarily within the banking space, to reduce budgets and prioritize cost cutting. While financial services companies look to invest in data, AI, cloud and digital platforms, spending restrictions have led to a focus on cost optimization through cloud and digital services.

Wipro experienced the greatest impacts on its financial services revenue, owing largely to overall market pressures. The company continues to struggle to fully capitalize on existing client relationships and create upselling opportunities. Leveraging its AI solutions and services for modernization could support the company’s efforts to forge additional discussions among insurance clients but will not offset limited interactions within the banking space. Wipro will likely prioritize engaging with insurance clients rather than banking institutions to generate revenue streams during 2024.

Infosys followed Wipro in terms of financial services performance, as a contract renegotiation within the financial services vertical reduced revenue growth by 100 basis points, which negatively impacted Infosys’ P&L and pressured margins. However, there are signs of improvement for Infosys in the segment, with increased activities in the U.S. and six large financial services deals signed in 1Q24. The deals likely comprise a mix of both insurance and banking clients. High inflation and interest rates are limiting client spend, pushing more vendors to prioritize workload and operations optimization.

Cognizant also experienced the impacts of limited budgets among its financial services clients. As conditions begin to improve, however, Cognizant management has highlighted new activities around personalization services as well as infrastructure and platform modernization, bringing in opportunities in the industry. Cognizant aims to grow its industry knowledge and specific offerings to better engage with clients and deliver personalized solutions. To address demand, Cognizant will look to create customer experience solutions and workload optimization offerings that leverage AI to strengthen its connection with clients in the sector.

TCS leverages the TCS BaNCS platform to deliver digital transformation services to a variety of financial services clients using a SaaS model or through the cloud. The platform supports infrastructure, application and workflow transformation, enabling users to modernize their environments, enhance customer engagement, utilize data and analytics, and accelerate innovation efforts. The platform allows TCS to deliver core banking transformations for clients and provides more personalized financial management services that can be aligned with budgets.

With demand around cloud and AI transformation projected to increase, TCS will develop new capabilities and functions such as TCS BaNCS for Intelligent Experience, allowing for the utilization of data and AI services across banking environments.

HCLTech offset a good amount of financial services pressures, benefiting from its digital marketing, data management, digital workplace services and IT transformation. The company was better able to withstand macroeconomic impacts, owing to its software application portfolio as well as experience around data services. Further, the company’s client management strategy enables HCLTech to solidify client relationships, allowing it to capture smaller-scale budget-friendly projects that are geared toward improving business operations and client interactions.

Conclusion

Vendors have taken different approaches to capitalize on financial services opportunities as macroeconomic challenges ease. One approach is to focus on the insurance sector, which was more protected from the impacts of reduced customer budgets than the banking sector.

While HCLTech maintained a steady performance, generating growth in financial services when excluding 2Q24, its peers invested in portfolio offerings that aligned with trends and demand for data, customer experience, cloud migration and IT modernization. During the remainder of 2024 and into 2025, HCLTech and TCS will likely be stronger candidates for financial services engagements, leveraging large platforms and solutions such as the TCS BaNCS platform to lead the technology-driven transformation across the industry.

Further, Infosys could pressure its India-centric peers, leaning on recent investments to strengthen its professional services positioning, such as through the acquisition of in-tech, which bolstered the company’s engineering services.

TBR publishes quarterly assessments of these IT services companies as well as others in the IT services, cloud, software, consulting, telecom, infrastructure and devices spaces. To access all current and historical data and analysis, start your TBR Insight Center™ free trial today.

https://tbri.com/wp-content/uploads/2024/09/business-development-concept_airdone_getty-images_canva-pro.png10801080Kelly Lesiczka, Senior Analysthttps://tbri.com/wp-content/uploads/2021/09/TBR-Insight-Center-Logo.pngKelly Lesiczka, Senior Analyst2024-09-25 13:52:502024-09-25 13:52:50How India-centric IT Services Vendors Are Navigating Economic Pressures in 2024

Ericsson’s Enterprise Wireless Solutions unit is exhibiting strong revenue growth and serves as a bright spot amid the company’s broader challenges. Ericsson has a compelling 5G-related portfolio that addresses the unique needs of enterprises ranging from SMBs to large industrial entities. Ericsson’s focus on enhancing its enterprise portfolio in areas including private cellular networks (PCNs), neutral host networks, fixed wireless access (FWA) and IoT will generate new revenue that will help to partially offset declining consolidated revenue, which is being negatively impacted by most Tier 1 operators decreasing network capex as they enter the later stages of 5G deployments.

Ericsson’s Enterprise segment has experienced challenges, however, namely declining revenue within its Global Communications Platform division, which includes Vonage. Ericsson appeared to overpay ($6.2 billion) for its acquisition of Vonage, which fits awkwardly within Ericsson’s historical core business and was primarily considered a down payment on developing a network API business with an unproven business model when it closed in 2022, and Ericsson has essentially confirmed that notion.

In October 2023 the company booked an SEK 32 billion ($3 billion) impairment charge on Vonage’s goodwill, writing off half of the acquisition price. The company took a further SEK 11.2 billion ($1.1 billion) noncash charge on the Vonage acquisition in July 2024. TBR believes Ericsson is correcting course, however, by more deeply collaborating with industry partners through its new network API joint venture, which will reduce fragmentation in the market and make it easier for developers to innovate and create new apps and use cases.

The joint venture will also provide Ericsson with a more risk-averse approach to tackling the network API opportunity by pooling funding and resources from the partners as the long-term market size for network APIs is uncertain. Ericsson will need to split proceeds from the joint venture with its partners, however, which will limit long-term revenue potential.

Ericsson Realizes the Need to Collaborate with Industry Partners to Accelerate Network API Development

The composition of Ericsson’s new network API joint venture, which currently does not have a formal name and is expected to close in early 2025 pending regulatory approval, entails Ericsson holding 50% equity in the venture, with the following telecom operators holding the remaining 50% of equity: America Móvil, AT&T, Bharti Airtel, Deutsche Telekom, Orange, Reliance Jio, Singtel, Telefonica, Telstra, T-Mobile, Verizon and Vodafone.

Vonage and Google Cloud will serve as channel partners for the joint venture, providing access to their ecosystems of millions of developers as well as their partners, and additional communication service providers (CSPs) and channel partners will be invited to join the entity in the future (Ericsson would maintain its 50% share in the venture if additional CSPs join). The goal of the joint venture is to create a platform that will provide network APIs to an ecosystem of developers, including hyperscalers, Communications Platform as a Service (CPaaS) providers, systems integrators and independent software vendors. The joint venture will be in alignment with existing industry network API initiatives, including the GSMA’s Open Gateway and the Linux Foundation’s CAMARA Project.

TBR believes the main benefit of the joint venture will be incentivizing developers to focus on the network API market by providing them with a simpler way to create apps at scale. For instance, developers currently need to engage with CSPs on a one-on-one basis to procure network APIs, which can be a slow and complex process. The joint venture aims to accelerate market development by providing combined common APIs that can work from any location or network. Reduced fragmentation will also speed market development as developers will be able to more fully concentrate on new use cases and applications rather than spending time modifying existing applications to make them compatible with networks on an operator-by-operator basis.

Industry projections for the network API market are wide ranging, with Ericsson citing McKinsey & Co.’s projections that the market will generate around $100 billion to $300 billion in incremental connectivity and edge computing-related revenue for operators by 2030 and that an additional $10 billion to $30 billion in revenue will be generated from the APIs themselves.

TBR believes the market size of the segment will mainly hinge on network APIs being able to provide developers with differentiated and compelling capabilities that are distinct from existing 5G capabilities that are available independent of network API access. Enhanced capabilities enabled by network APIs include differentiated connectivity, device-based location, security (e.g., authentication) and network insights.

Current primary use cases for network APIs include simplified secure login for devices and advanced network authentication to strengthen fraud prevention. Other main use cases include enabling enhanced location verification and more reliable connectivity to support point-of-sale platforms, as well as optimizing the user experience for entertainment services such as video streaming and gaming applications.

Ericsson’s joint venture will create competitive pressures for Nokia, which is providing network API solutions via its Network as Code platform. Nokia has at least 14 Network as Code CSP partners as of June and aims to have more than 30 partners by the end of 2024. Nokia may be challenged in meeting this goal, however, due to potential CSP partners possibly being swayed by the ecosystem and benefits provided by Ericsson’s joint venture. Ericsson’s CSP partners are not tied exclusively to the joint venture, however, and have the option to join Nokia’s ecosystem as well.

For IT Services Companies and Consultancies, the New Joint Venture Could be a Promising Change Agent in the Broader Ecosystem

From the perspective of global IT services companies and consultancies, such as Accenture, Infosys and Deloitte, Ericsson’s event theme, “Capture the value of enterprise 5G,” remained focused on Ericsson’s opportunities with and through telco operators while providing a modest opening for increased go-to-market and alliance activity.

Based on the event presentations, sidebar discussions with Ericsson leaders, and TBR’s analysis of Ericsson over the last two decades, we see two opportunities for Ericsson to enhance its ecosystem plays with IT services companies and consultancies that align well with Ericsson’s overall strategy.

First, TBR’s recent Voice of the Partner research shows that cloud and software vendors, OEMs, and IT services companies see 5G as a promising source of near-term growth, nearly on par with generative AI. To address their enterprise clients’ growing 5G needs, IT services companies and consultancies will need closer alliances with incumbent telcos and OEMs, including Ericsson. IT services companies and consultancies will not try to sell their own connectivity solutions but will readily partner to bring those solutions to their enterprise clients if informed, aligned and incented, particularly if the five-to-eight-times revenue multiplier applies to services attached to Ericsson’s hardware.

Second, TBR’s ecosystem reports, which cover a dozen leading global IT services companies’ relationships with Amazon Web Services (AWS), Google Cloud, Microsoft Azure, Adobe and Salesforce, confirm that scale remains a key differentiating characteristic, both for alliances managers across the ecosystem and enterprise clients looking for multiparty, well-orchestrated technology solutions. Ericsson’s joint venture with Google and the 12 operators could be highly appealing as an alliance partner, bringing IT services companies and consultancies into contact with new personas within their enterprise clients, which will create an expanded playing field for professional and managed services companies. In short, Ericsson’s new joint venture could be an ecosystem catalyst, provided the joint venture finds a go-to-market focus and well-led partnerships with the right IT services companies and consultancies.

Ericsson Launches Private 5G and Neutral Host Network Solutions Under its Ericsson Enterprise 5G Segment

At Ericsson Enterprise Industry Analyst Day in September, Ericsson reintroduced its Ericsson Enterprise 5G portfolio, which includes three solutions:

Ericsson Private 5G: A converged LTE/5G PCN solution with industry and licensed spectrum support

Ericsson Private 5G Compact: A U.S. CBRS-based solution designed for enterprises requiring connectivity that is more reliable than Wi-Fi. The solution was previously branded as Cradlepoint NetCloud Private Networks.

Ericsson Enterprise 5G Coverage: A turnkey neutral host solution that features certification from all Tier 1 U.S. operators. The solution can support up to three carriers per radio.

The relaunch of the Ericsson Enterprise 5G portfolio, in addition to the legacy Cradlepoint business now branded under this segment, will help Ericsson strengthen its messaging within the PCN market and better compete against Nokia, which TBR estimates is the second-largest PCN vendor by revenue globally (behind Huawei) and the largest when excluding China.

Ericsson Enterprise 5G Coverage is certified by AT&T, T-Mobile and Verizon, which will be a significant benefit as Ericsson aims to gain headway within the neutral host networks market. Neutral host networks are gradually gaining traction as they are easier to deploy compared to legacy distributed antenna systems (DAS) and can provide significant cost savings as they enable a single neutral host network to support customers from multiple operators without requiring each operator to deploy its own separate infrastructure.

Industrial sites, schools and hospitals are the primary locations where neutral host networks are initially being deployed, and Ericsson’s early customers for the solution include Toyota Forklifts in Indiana and engine manufacturer Cummins in New York.

Conclusion

TBR believes Ericsson is effectively positioning to capitalize on 5G-based solutions within the telecom enterprise space, including network APIs, PCNs and neutral host networks. Ericsson is aware that industry collaboration is essential for these segments to reach their peak potential, evidenced by the vendor’s initiatives including the formation of the network API joint venture and gaining certification from AT&T, T-Mobile and Verizon for its neutral host network solution.

Ericsson’s success in areas including network APIs, PCN and multi-access edge computing will be impacted by coopetition from hyperscalers within these segments. Though Ericsson has established partnerships with AWS, Google Cloud and Microsoft Azure within multiple portfolio segments, the company’s revenue opportunities will be limited as hyperscalers take a portion of revenue from enterprise deployments.

https://tbri.com/wp-content/uploads/2024/09/navigation_erdikocak_getty-images_canva-pro.png10801080Steve Vachon, Senior Analysthttps://tbri.com/wp-content/uploads/2021/09/TBR-Insight-Center-Logo.pngSteve Vachon, Senior Analyst2024-09-25 13:49:192024-09-25 13:49:19Ericsson Aims to Accelerate Network API Market Development via New Venture with Leading Global Telcos

TBR Perspective: Nokia’s Fixed Networks Business Unit

Nokia is the largest vendor of fixed network access infrastructure by revenue in the Western economic bloc, a position of strength that exposes the vendor to a range of opportunities that arise in the market. While Nokia remains focused on its fiber-based platform, the vendor is also supporting fixed-wireless access (FWA), which is a rapidly growing service offering in the telecom industry.

Though revenue in Nokia’s Fixed Networks business unit has been uneven over the past few years (primarily due to the disruptions caused by the COVID-19 pandemic), the unit is poised to be one of the biggest beneficiaries of government-supported broadband programs and ongoing internet service provider (ISP) investment in high-speed broadband access technologies, driving a positive revenue trend over at least the next three to five years.

Nokia is focused on expanding access to broadband (through fiber and/or FWA) and introducing a future-proof platform for ISPs to build upon. The company is trying to be everything to everyone in this domain by providing a near complete portfolio (only DOCSIS is missing).

Despite Nokia’s favorable market position and government-induced tailwinds for the broadband infrastructure domain, TBR notes that the supply-and-demand dynamics as well as the timing of investments are prone to be disjointed, lengthening the time required to meet infrastructure deployment objectives compared to what was originally expected by the government and the telecom industry.

Additionally, TBR remains steadfast in its belief that building fiber out to every household is not economically feasible (despite what the government and stakeholders in the market say they want) and that alternative broadband access technologies (such as FWA and satellite) are going to increase in the global mix to connect the unconnected and underserved peoples of the world.

Impact and Opportunities for Nokia

BEAD Program Will Likely Stretch to the Mid-2030s due to Challenges and Delays

Broadband Equity, Access, and Deployment (BEAD) Program-supported projects are now slated to begin deployments in 2025, more than a year later than originally planned. There is a long list of reasons (most of which are related to mapping integrity and political processes) why the program has been delayed thus far, and there is a growing list of reasons that suggest it will take longer for the program to fully ramp up and complete its objective (i.e., spend all of the $42.5 billion allocated to the program).

Among the biggest challenges that lie ahead for the BEAD Program is a shortage of skilled labor (e.g., fiber splicers and trenching machine operators) and industrial equipment, such as boring machines, that will be required to deploy fiber to an estimated 5.5 million households across the U.S. Shortages of products that meet the Build America Buy America (BABA) requirements associated with the BEAD Program could also cause a timing and supply issue.

Taken together, TBR now believes the deployments tied to the BEAD Program will begin next year and it could take as long as the mid-2030s for all the program’s funding to be disbursed, more than five years longer than the government and market ecosystem originally anticipated. Nokia is doing as much as it can to mitigate and alleviate these potential challenges in the market.

For example, Nokia is proactively educating stakeholders in the ecosystem and working with its partners to better match supply with demand for products and resources. This orchestration of the ecosystem will help align stakeholders and enable the industry to put its best foot forward in carrying out this infrastructure build-out program as well as position Nokia to maintain and grow its leading share in the broadband infrastructure market.

Do Not Forget About Non-BEAD Government Programs for Broadband

Though the telecom industry likes to focus on the BEAD Program (likely because it is the largest program by dollar amount in the broadband ecosystem in the U.S. market), there are a variety of other government-supported programs that also deal with broadband, including the American Rescue Plan Act (ARPA), the Rural Digital Opportunity Fund (RDOF), the U.S. Department of the Treasury’s Capital Projects Fund, the Tribal Broadband Connectivity Program, and the U.S. Department of Agriculture’s ReConnect Loan and Grant Program.

In aggregate, TBR estimates there is more than $80 billion in direct and indirect government stimulus allocated for broadband-related projects in the U.S. market alone, all of which is slated to be spent by the mid-2030s. There are also a few hundred billion dollars in aggregate in similar broadband-implicated programs in other regions, most notably in China, the European Union, the U.K. and Australia.

Fiber Access Technology Capabilities Exceed Usability, Creating a Conundrum for Vendors

Technological innovations pertaining to fiber access have become so advanced and the bandwidth available through fiber access so massive that the capabilities of the technology far exceed what most end customers could possibly need or use. This disconnect creates a conundrum for vendors such as Nokia that supply the broadband infrastructure market.

Though fiber broadband infrastructure is, and will remain, in high demand, most ISPs will be loath to adopt the most cutting-edge technologies because they far exceed what customers would need and put unnecessary additional cost burden on the operator.

There are exceptions, such as what Google Fiber and Frontier Communications are deploying (specifically 50G and 100G connections, respectively), but TBR believes most ISPs will focus on 10G or lower connections, which is more than enough bandwidth for the vast majority of households and businesses and are likely to be future-proof for many years to come.

Overbuilding and One-upmanship Risks New Price War for High-speed Internet Service

The government funding boost, coupled with technological advancements and new entrants into the ISP domain, is creating a situation that is ripe for a price war for broadband services. Specifically, many more markets across the U.S. are likely to have three or more (in some cases up to seven) providers of high-speed broadband service in a given area, including xDSL, FTTx, HFC (via DOCSIS) as well as FWA and satellite (mostly delivered via low Earth orbit [LEO] satellites).

Given that a provider typically needs to have more than 30% market share in a given area to achieve profitability in the broadband services market, an increasing number of options puts more power into the hands of end users, which historically suggests the pricing environment will be extremely competitive.

In response to the hotter competitive environment, providers that are multiservice-oriented are trying to attract and lock in market share by offering converged (aka bundled) solutions, usually giving end users a discount as an incentive to sign up and stay.

Additionally, TBR notes that ISPs are increasingly engaging in one-upmanship (which is also a symptom of the existence of too many options in a given market), meaning ISPs are marketing ever higher broadband speeds to customers to position their offerings as better than the competition while attempting to incrementally increase average revenue per user.

Though this strategy has been effective in years past, it is likely to lose efficacy after speeds surpass the level at which the benefits of faster speeds become imperceptible to end users. Therefore, in aggregate, TBR expects the pricing environment in the U.S. for broadband service to be increasingly competitive through at least the remainder of this decade.

Private Equity Comes into the Fixed Broadband Market

Private equity firms are entering the telecom infrastructure market in a big way, gobbling up assets and forging joint ventures with telcos that want to (or need to) raise capital and hedge their risks. Some private equity-sponsored entities are also now building out their own greenfield fiber-based networks (such as Brookfield Infrastructure Partners’ Intrepid Fiber Networks) and are even moving the market toward wholesale, shared and other forms of open-access models.

Though the inclusion of private equity into the broadband infrastructure domain is bringing large pools of fresh capital into the market, this trend also risks fueling overinvestment, price compression and disruption of incumbent ISPs’ business models. Regardless, expect private equity to remain attracted to assets that offer consistent cash flow over a long duration, and their inclusion in the telecom ecosystem is likely a net positive for overall market development and evolution.

Existing Government Stimulus May Still Not be Enough for FTTP; Alternatives Will Likely be Called on at Scale to Fill in the Gaps

Though governments (and most of the stakeholders in the telecom ecosystem) across the world want full fiber to each premises, this is still not economically feasible. For example, it is not uncommon for some locations in the U.S. to cost upward of $1 million per premise to connect with fiber, a price that will be politically difficult to justify and that is not supported by normal market conditions. In these extreme situations, it is highly likely that governments will allow and embrace alternatives, such as FWA and satellite-based connectivity.

TBR notes that FWA and LEO constellations can easily deliver sustained speeds in excess of 100Mbps at a fraction of what it would cost to deploy fiber to the premises (FTTP). With that said, of the estimated 5.5 million households that the government has identified as needing broadband connection in the U.S., TBR would not be surprised if up to 25% of that number of households is ultimately connected via FWA or satellite (enhancements to DOCSIS and xDSL are also potential options to close the underserved gap). In other countries, that percentage could be even higher.

New Business Models Hold Promise to Connect Low-income Households in Emerging Markets

Upstart ISPs, such as fibertime and Vulacoin in South Africa, have established innovative solutions to cost-effectively provide high-speed broadband services to low-income areas. The architecture of the network emphasizes leveraging FWA and Wi-Fi with a relatively low amount of fiber and the business model is focused on selling units of time (in minutes), which is more affordable for lower-income end users.

TBR notes this model requires scale and high time of use to achieve profitability, meaning it is best suited for dense areas, especially impoverished neighborhoods. TBR also notes that obtaining access to high-speed internet is a key avenue in which areas can strengthen their local economies and help reduce levels of poverty.

In addition to South Africa, Brazil is also exploring the use of this model. This approach is also likely to be leveraged in other parts of Africa as well as in parts of India and Southeast Asia.

Conclusion

Government and private equity involvement in the broadband market may prove to be a mixed blessing. Though there are concerning indicators suggesting there are too many broadband providers in some key markets (especially the U.S.) and that broadband access businesses are becoming overvalued, these market dynamics actually represent tailwinds for Nokia, which is best positioned to garner a disproportionate amount of investment slated for broadband infrastructure in the Western economic bloc, which includes North America, Europe, developed APAC and select developing markets such as India.

Nokia’s outsized and unique position in the broadband infrastructure ecosystem enables the company to play a key role in orchestrating partners and customers to achieve their objectives in the most optimal way possible. Fiber will remain the coveted access medium for high-speed broadband, but the world will also employ other broadband access mediums to a large extent.

New ISP and hyperscaler business models, coupled with sustained investments by incumbent ISPs and supported by government stimulus, create an environment ripe for moving the world closer to full broadband coverage for all people.

https://tbri.com/wp-content/uploads/2024/09/business-growth-concept_in-future_getty-images_canva-pro.png10801080Chris Antlitz, Principal Analysthttps://tbri.com/wp-content/uploads/2021/09/TBR-Insight-Center-Logo.pngChris Antlitz, Principal Analyst2024-09-24 10:14:192024-09-24 10:14:19Nokia’s Fixed Networks Unit Poised for Long-term Growth Despite Market Challenges

What is the Current State of the Market for Leading U.S. Operators?

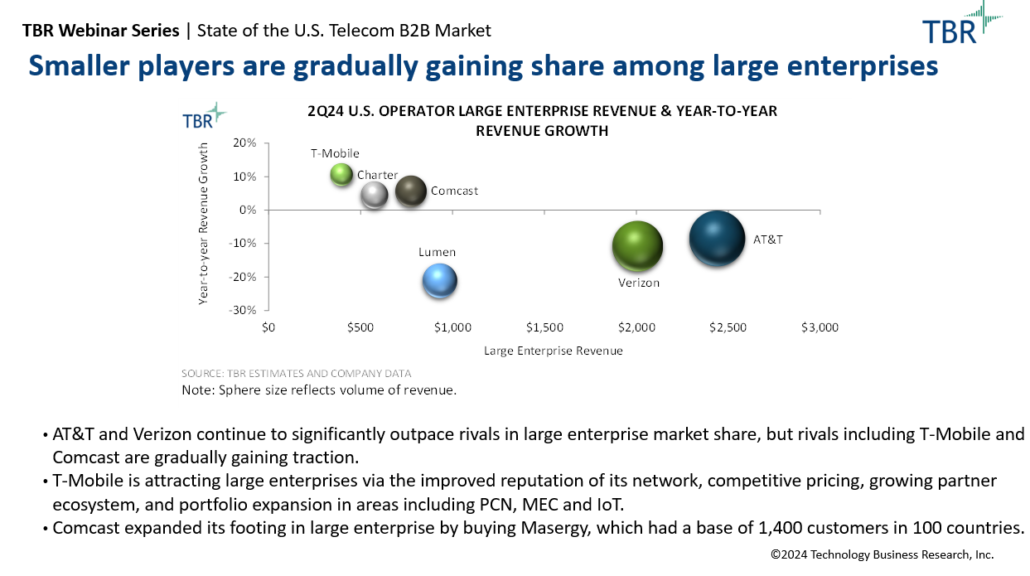

AT&T and Verizon remain the largest players by a wide margin in the U.S. telecom B2B market from a revenue perspective, largely due to the companies’ established footing in the B2B market among businesses of all sizes. However, competitors are gradually gaining market share, especially T-Mobile, which is attracting businesses through its relative advantage in 5G network quality and value-based pricing as well as portfolio expansion in nascent growth areas including multi-access edge computing (MEC) and private cellular networks (PCN).

Charter Communications and Comcast are also gradually gaining market share, aided by the companies not facing erosion from legacy wireline solutions to the extent of AT&T, Lumen Technologies and Verizon as well as their ability to attract SMBs via their new B2B wireless offerings.

In this TBR Insights Live session, TBR Telecom Senior Analyst Steve Vachon shares an in-depth update on the U.S. telecom B2B market. Key points of discussion include TBR’s latest data on financial and go-to-market performance of leading U.S. operators that sell to enterprises as well as recent key developments that are impacting the U.S. B2B market.

TBR’s U.S. enterprise operator research stream details and compares the initiatives, strategies and performances of the largest U.S. operators, including AT&T, Verizon, Lumen Technologies, Comcast, T-Mobile and Charter Communications.

In the Above TBR Insights Live Session on the State of the U.S. Telecom B2B Market You’ll Learn:

B2B revenue comparison of leading U.S. operators, supported by data and analysis from TBR’s most recent S. Telecom Enterprise Operator Benchmark

Macroeconomic and telecom industry trends that are impacting B2B customer segments, including SMBs, large enterprises and the public sector

The impact of recent and upcoming partnerships and mergers & acquisitions on the competitive landscape of the U.S. telecom B2B market

How U.S. operators are positioning to capitalize on opportunities within key growth areas, including converged services, mobility, fiber broadband, fixed wireless access (FWA), MEC, IoT and PCN

Excerpt from State of the U.S. Telecom B2B Market: Trends and Strategies Impacting the Competitive Landscape

Smaller Players Are Gradually Gaining Share Among Large Enterprises

AT&T and Verizon continue to significantly outpace rivals in large enterprise market share, but rivals including T-Mobile and Comcast are gradually gaining traction.

T-Mobile is attracting large enterprises via the improved reputation of its network, competitive pricing, growing partner ecosystem, and portfolio expansion in areas including PCN, MEC and IoT.

Comcast expanded its footing in large enterprise by buying Masergy, which had a base of 1,400 customers in 100 countries.

TBR Insights Live sessions are held typically on Thursdays at 1 p.m. ET and include a 15-minute Q&A session following the main presentation. Previous sessions can be viewed anytime on TBR’s Webinar Portal.

https://tbri.com/wp-content/uploads/2024/09/State-of-US-Telecom-B2B-Market-Webinar_4Q24_Square-Site-Image.png10801080TBRhttps://tbri.com/wp-content/uploads/2021/09/TBR-Insight-Center-Logo.pngTBR2024-09-16 10:02:122024-10-17 16:27:32State of the U.S. Telecom B2B Market: Trends and Strategies Impacting the Competitive Landscape

Making Data-driven Decisions in Sell-with, Build-with Alliance Partnerships

More enterprise IT spend is being driven by and through ecosystem partnerships than ever before, and spend is only forecasted to grow over the coming years. How do global systems integrators (GSIs), channel partners, hyperscalers, independent software vendors (ISVs), managed service providers (MSPs) and OEMs maximize limited resources to staff, market and manage vital go-to-market partnerships across their ecosystems?

In this TBR Insights Live session, TBR principal analysts Patrick Heffernan and Allan Krans give viewers an exclusive look at how TBR’s revenue, headcount and investment data can guide your firm’s quarterly management of alliance strategy. Additionally, our experts discuss critical intelligence on annual performance, trends and opportunities for all sides of these multivendor partnerships, which are responsible for more than 50% of global enterprise spend.

In the above TBR Insights Live replay on strategic alliance management you’ll learn:

How both services revenue and industry-vertical revenue can guide your firm’s alliance strategy

How quarterly ITO revenue can help your firm benchmark partner teams for QBRs with validated and independent data

Which GSI may be the right partner for your firm, and why the biggest partner may not be the best

Excerpt From Strategic Alliance Management: Case Study of a TBR Use Case

TBR’s Top Emerging Use Case: Ecosystem Intelligence

Estimating and evaluating the revenues jointly generated by ecosystem partners allow TBR’s clients to accurately benchmark their role in the ecosystem, learn from market leaders and target investments toward high growth potential areas.

Companies that are not yet playing in an ecosystem use TBR’s analysis to determine opportunities and understand catalysts for faster growth with ecosystem-dominating players.

Ecosystem Intelligence Examples

A leading global management consultancy used TBR’s ecosystem intelligence to evaluate its relative position with hyperscalers and software vendors, informing decisions around training, staffing, marketing, and joint go-to-market initiatives.

Midtier IT services companies have used TBR’s research around ecosystem best practices to reshape their partnering and go-to-market motions to better appeal to leading technology companies.

A leading cloud platform partner organization uses revenue, headcount, and ISV partner counts to guide quarterly decision making.

TBR Insights Live sessions are held typically on Thursdays at 1 p.m. ET and include a 15-minute Q&A session following the main presentation. Previous presentations can be viewed anytime on TBR’s Webinar Portal.

https://tbri.com/wp-content/uploads/2024/09/Strategic-Alliance-Management-Webinar_4Q24_Square-Site-Image.png10801080TBRhttps://tbri.com/wp-content/uploads/2021/09/TBR-Insight-Center-Logo.pngTBR2024-09-16 09:52:322024-10-15 11:09:52Strategic Alliance Management: Case Study of a TBR Use Case

Atos, the worldwide IT partner for the Summer and Winter Olympic and Paralympic Games, invited a group of industry analysts to the 2024 Paris Olympics. The goal of the event was to show Atos in action during the Games with a tour of the Technology Operations Center in Paris, which is one of the three locations responsible for delivering IT services and keeping the Games running. The analysts also attended a swimming competition event at Paris La Defense Arena, to experience the secure and digital experience provided by Atos and its partners in running the IT systems behind the Games.

The Olympics Must Run Flawlessly; There Are No Second Chances

Atos utilized its well-established expertise in the sports and entertainment industry to provide IT services for the 2024 Paris Olympics and Paralympics and enable a secure and digital experience for end users, which typically amounts to a total of approximately 4 billion viewers globally. Atos has been providing services for the Olympic Movement since 1989. Atos established its relationship with the International Olympic Committee (IOC) as a Worldwide IT Partner in 2001 and provided IT services for the first Winter Olympics in 2002 in Salt Lake City. Providing uninterrupted running of the IT systems behind the Olympics every two years requires dedication and strict execution of processes and timelines.

According to Angels Martin, general manager Olympics at Atos, “Olympics challenges are similar to other projects; the difference is visibility [of the Games]. No one will postpone the opening ceremony because Atos is not ready.” Martin also explained that cybersecurity management is a vital activity that Atos provides as the Games are one of the most targeted events in terms of cyberattacks, which could threaten the smooth functioning of the Olympics. She also stated that the Games are complex to manage with multiple parties, such as the IOC, sports federations, broadcasters and journalists, requiring services and access to information 24/7 from anywhere on any device. Martin also noted that demand for information has changed significantly since the first engagement 30 years ago, and today Atos is applying AI-driven solutions to enable processes for the Games. For example, Atos used AI solutions for the 2024 Paris Olympics to support the Organising Committees for the Olympic Games in providing scenarios for matching volunteers with job positions based on skills and abilities. In the 2020 Tokyo Olympics Atos provided an AI solution for facial recognition for venue access using accreditation.

Atos Integrates Critical IT Systems and Manages Partners to Run the Games

Atos is responsible for integrating critical IT systems, managing programs with IT vendors that deliver services for the Organising Committees for the Olympic Games, supporting critical applications for the Games and providing security services to enable smooth and uninterrupted running of the Games. For example, for the 2024 Paris Olympics and Paralympics Atos operated the Olympic Management System, which included a volunteer portal, a workforce management system, athlete voting applications, sport entries and qualifications, competition schedule and accreditation. Atos was responsible for the Olympic Diffusion System, which contained Olympic data feed, web results, mobile apps for results, a Commentator Information System, an information system for journalists called MyInfo, and a print distribution system. Atos was also responsible for cloud orchestration between private cloud, public cloud services and data centers at venues.

Additionally, Atos applied its expertise around working with a diverse group of technology partners to help run the Games and provided systems integration of applications with other IT providers and partners. Atos integrated partners, such as technology providers, media, the IOC, Organising Committees for the Olympic Games, and security providers, to ensure efficient delivery, operations, timelines and venue management activities. Atos also helped coordinate responses on daily activities and addressed critical events when they occurred. For example, Atos worked with Omega, the timing and scoring sponsor of the 2024 Paris Olympics, to relay results and data to spectators globally in real time. Omega captured raw data around timing and scoring, fed the results into scoreboards and videoboards at venues jointly with Panasonic, and provided data to Atos to feed into the Commentator Information System.

Atos’ Olympics and Paralympics Achievements

Achievements from the 2020 Tokyo Olympics and the 2024 Paris Olympics show the magnitude of work Atos provides. There are approximately 900 events that Atos has to manage to be able to transmit results instantly from competition and noncompetition venues. The company utilized the volunteer portal to process 200,000 volunteer applications prior to the 2020 Tokyo Olympics, and the number of volunteer applications swelled to 300,000 for the 2024 Paris Olympics. According to Atos, one of the most complex activities around managing people for the Olympic and Paralympic Games is assigning volunteers to the large number of necessary positions. For the 2024 Paris Olympics and Paralympics, Atos innovated the volunteers’ assignment process by implementing an optimized pre-assignment scenario model and an AI-based solution that utilized constraint logic programming to improve position matchups. At the 2020 Tokyo Olympics Atos issued 535,000 accreditations through the system and established 350 accreditation checkpoints with facial recognition in all competition and noncompetition venues. Additionally, cloud usage at the 2020 Tokyo Olympics enabled Atos to reduce by 50% the number of physical servers at the 2020 Tokyo Olympics and improve sustainability.

Every Two Years Atos Organizes Upcoming Games

Typically, pre-project activities for each Olympic Games begin six years prior to the event. For example, pre-project activities for the 2024 Paris Olympics and Paralympics began in 2018, and planning began in 2020 with the development of a master plan and strategy and related responsibilities matrix. In November 2020 Atos appointed the first core team for the 2024 Paris Olympics and Paralympics. In 2021 Atos began designing business requirements and systems infrastructure and established a test lab, and in 2022 the company initiated the building of systems and expanded the testing facility. In June 2023 Atos launched testing activities such as integration tests, acceptance tests, systems tests, events tests and multisport tests to prepare for operating the Games in 2024. During the first several months of 2024, Atos worked on venue deployment, disaster recovery and technical rehearsals.

For example, between May 13 and May 17 Atos completed the final technology rehearsal for the 2024 Paris Olympics and Paralympics. The rehearsals, which took place across different locations in Paris and other sites of the Olympic and Paralympic Games, were designed to test IT policies and procedures and how well IT teams can collaborate and handle real-time situations that may impact the Games. Atos is the IT integration leader and coordinates with the Organising Committee for the Olympic Games and with experts and technology partners. The technology rehearsals were conducted in 39 venues, including Atos’ Central Technology Operations Center in Barcelona, Spain, and venues specific to the Games, such as Atos’ Technology Operations Center in Paris, the Main Press Center, The Stade de France and competition venues.

The Olympic Games resemble a large-scale international corporation mobilizing approximately 300,000 people for the duration of the Games. Atos provides IT services with teams located in the host city and in Atos’ facilities in Poland, Morocco and Spain, and serves more than 4 billion customers globally competition results. While every two years Atos must set up a new organization for each Summer and Winter Games, the company has a well-established process and experience with starting over again. Every two years Atos establishes a Technology Operations Center (TOC) in the host city of the Summer and Winter Games. The TOC is the technology command and control center that houses teams from Atos, the IOC, the Organising Committees for the Olympic Games and other technology partners. The TOC consists of approximately 300 people who are coordinated by Atos and available 24/7 while the Olympics and Paralympics are running. Atos also has a Central Technology Operations Center (CTOC) in Barcelona, which is organized in a similar manner as the TOC in the host city. The CTOC delivers remote support during competitions and critical events, such as the volunteer campaigns, and orchestrates applications for the Games, and consists of approximately 80 people who provide services around operations, architecture, security, infrastructure and data management. Atos also has an Integration Testing Lab in Madrid that manages system testing for the Games.

Atos Adds New clients in the Sports and Entertainment Industry

Atos’ engagement with the IOC ends with the 2024 Paris Olympics and Paralympics. However, Atos has been expanding its client roster in the sports and entertainment industry, applying its vast experience gained from the Olympics. In December 2022 Atos signed an eight-year deal with the Union of European Football Associations (UEFA) to be the official technology partner for men’s national team competitions. Atos is assisting UEFA in managing, improving and optimizing its technology landscape and operations. Atos is also managing and securing the hybrid cloud environment and infrastructure that hosts UEFA’s services, applications and data. In July Atos announced that it had successfully delivered key IT services and applications supporting the UEFA EURO 2024 from June 14 to July 14. Atos supported UEFA systems such as accreditation, access control solutions and competition solutions. Atos managed core IT systems through its football service platform and stored and distributed UEFA football data to stakeholders. Atos is the official IT partner of UEFA National Team Football until 2030.

Conclusion

Atos has a well-established position and history of operating in the sports and entertainment industry. Expanding its client roster with organizations such as UEFA will help the company maintain its reputation as a reliable IT services provider and innovation partner for major events. Enabling the running of complex events such as the Summer and Winter Olympic Games and the UEFA EURO 2024 championship provides global visibility of Atos’ capabilities and brand and enables the company to augment its client base in the industry.

https://tbri.com/wp-content/uploads/2024/09/Atos-Paris-Olympics-2024.png10801080Elitsa Bakalova, Senior Analysthttps://tbri.com/wp-content/uploads/2021/09/TBR-Insight-Center-Logo.pngElitsa Bakalova, Senior Analyst2024-09-10 10:23:102024-09-11 10:34:32Atos Powers 2024 Paris Olympics and Paralympics with Cutting-edge IT and AI Solutions

GenAI requires massive investment now for a chance at massive long-term returns

For most new technologies and trends in the IT space, actual business momentum and revenue generation typically take years to develop. In fact, in many cases, particularly with new technologies available to consumers, monetization may never develop, as the expectation of free trials or advertising-led revenue streams never leads to sustainable business models.

The history around monetizing new technologies is what makes the rise of generative AI (GenAI) over the past 18 months so notable. In such a short period of time, we have tangible evidence from some of the largest IT vendors that billions of dollars in revenue have already been generated in the space, with the expectation that even more opportunity will develop in the coming years.

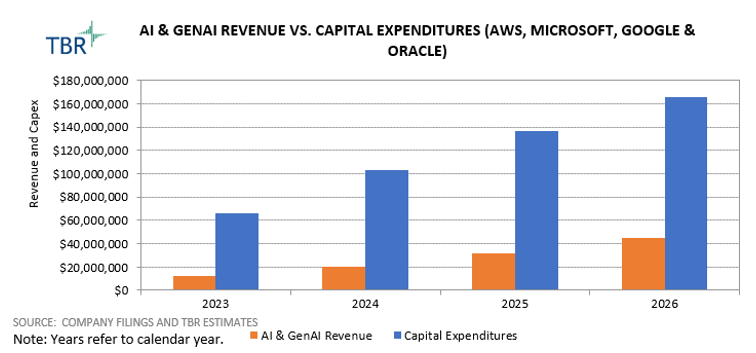

AI and GenAI revenue streams have not come without investment, however, as the infrastructure required to enable the new technology has been significant. The three major hyperscale cloud providers have borne the brunt of this required investment, outlaying billions of dollars to build out data centers, upgrade networking and install high-performance GPU-based servers. Amazon Web Services (AWS), Microsoft, Google and other cloud platform providers were already spending tens of billions annually to maintain and expand their cloud service offerings, and GenAI adds significantly to that investment burden.

The early revenue growth resulting from GenAI offerings has been promising, but put in the context of the increased investment required, it becomes clear that the business impacts of the technology will play out over an extended time period. Most public companies execute quarterly, plan annually and, as a stretch, project their expectations out over three to five years.

The impact of GenAI extends even further, as Microsoft CFO Amy Hood stated on the company’s fiscal 4Q24 earnings call: “Cloud and AI-related spend represents nearly all of our total capital expenditures. Within that, roughly half is for infrastructure needs where we continue to build and lease data centers that will support monetization over the next 15 years and beyond.” That means not only that Microsoft spent $19 billion on capital expenditures during a single quarter to support cloud and AI but also that the time horizon for the returns on that investment stretches beyond a decade.

Microsoft is, in this way, representative of all cloud platform peers, investing huge sums of capital expenditures now to realize modest new streams of revenue in the short term and anticipating significant revenue opportunity over the next 20 years.

AI-related revenue is already considerable, with growth expected to persist

TBR estimates the four leading cloud platform vendors generated more than $12 billion in revenue from AI and GenAI services in 2023, which is in and of itself a sizable market. On top of that, we expect revenue from those four vendors to increase by 71% during 2024.

Below are examples from some of the largest monetizers of GenAI so far, with estimates on the current size of their respective businesses and the strategies they use. A market of that scale and growth trajectory is notable in an IT environment where much more modest growth is the norm. While we expect growth to gradually slow and normalize over the coming years, the AI and GenAI markets remain attractive nonetheless. Insights follow about how some of the current leaders in this space are monetizing.

Microsoft (estimated $1 0 billion in GenAI revenue annually): While Microsoft did not quite meet Wall Street’s lofty expectations for AI-related revenue growth, the company posted a solid quarter in 2Q24. In TBR’s opinion, Microsoft’s GenAI strategy is on the right track, and its financial results align closely with our expectations. In 2Q24 Azure AI services contributed 8% of Azure’s 29% year-to-year growth, while Copilot was cited as a growth driver for Office 365.

Nevertheless, with Office 365 revenue growth decelerating compared to past quarters, it is clear the monetization of GenAI will take time to materialize. Still, given Microsoft’s current capex spend and capex forecast, the company is committed to its AI strategy. Management stated nearly all $19 billion of capital expenditures this quarter was focused on the cloud business, with roughly half going toward data center construction and the other half used to procure infrastructure components like GPUs.

This hefty commitment indicates that GenAI will remain at the forefront of Microsoft’s product development, go-to-market and partner strategies for years to come as the company looks to turn an early lead into an established position atop the AI and GenAI market.

AWS (estimated $2.5 billion in GenAI revenue annually): During AWS’ New York City Summit event in July, Matt Wood, the company’s VP of AI Products, noted that GenAI had already become a multibillion-dollar business for the company. Amazon CEO Andy Jassy has also spoken confidently about the future of AI, publicly proclaiming the company’s belief that GenAI would grow to generate tens of billions in revenue in the coming years.

The fact that AWS has been playing in AI infrastructure, with custom chip lines for both training and inference, well before the GenAI hype cycle is notable. Customers are not likely to go through the daunting task of moving off industry standard hardware, so these custom offerings can still be a more cost-effective source for net-new workloads, which is one of the reasons they signify a lot of potential for GenAI.

AWS’ custom offerings, coupled with tools that customers use to build and fine-tune models, such as Bedrock and SageMaker, will continue to spin the EC2 meter. AWS does have other GenAI monetization plans with a two-tiered pricing model for Amazon Q Business and Q Developer. However, it is still early days for these offerings, and Microsoft Copilot entering the mix, at least from the line-of-business (LOB) perspective, clearly indicates AWS faces an uphill battle.

Google Cloud (estimated $2 billion in GenAI revenue annually): Unlike some of its peers in the industry, Alphabet has not clearly quantified the impact that GenAI is having on Google Cloud’s top line. However, on Alphabet’s recent earnings call, executives said that GenAI solutions have generated billions of dollars year to date and are used by “the majority” of Google Cloud’s top 100 customers.

These results, coupled with a 40-basis-point acceleration in Google Cloud’s 2Q24 revenue growth rate, to 28.8%, signal that while GenAI is having an impact on Google Cloud Platform (GCP) revenue growth, it is very early days. Steps Google Cloud is taking to boost developer mindshare — with over 2 million developers using its GenAI solutions — and align with global systems integrator (GSI) partners to unlock new use cases, leave us confident Google Cloud can more aggressively vie for GenAI spend through 2025.

ServiceNow (less than $100 million in GenAI revenue annually): With Now Assist net-new annual contract value (NNACV) doubling from last quarter, ServiceNow’s steady momentum selling GenAI to the enterprise continues. Now Assist was included in 11 deals over $1 million in annual contract value (ACV) in 2Q24, showing positive early signs that the strategy of packaging premium digital workflow products based on domain-specific large language models (LLMs) is resonating.

At 45%, ServiceNow’s Pro SKU penetration rate, which represents the percentage of customer accounts on Pro or Enterprise editions of IT Service Management (ITSM), HR Service Delivery (HRSD) and CSM products, is already very strong. Upgrading these already premium customers to Pro Plus SKUs with GenAI, for which ServiceNow has already realized a 30% price uplift, could signify an opportunity for ServiceNow valued at well over $1 billion. Naturally, a big focus is expanding the availability of Pro Plus outside the core workflow products.

IBM (less than $2 billion in GenAI revenue annually): Approximately 75% of IBM’s reported $2 billion in GenAI book of business to date stems from services signings, and IBM lands nearly all watsonx deals thorough Consulting. Companies need help getting started with GenAI in the cloud, and IBM’s ability to lead with Consulting and go to market as both a technology and consulting organization will continue to prove unique in the GenAI wave.

On the software side, overcoming challenges with the Watson brand and deciding how much it wants to compete with peers have been obstacles, but IBM is now strategically pivoting around the middleware layer, hoping to act as a GenAI orchestrator that helps customers build and run AI models in a hybrid fashion. This pivot has resulted in a series of close-to-the-box investments, including Red Hat’s InstructLab project, which allows customers to fine-tune and customize Granite models, and IBM Concert for application management.

According to IBM, these types of GenAI assets have contributed roughly $0.5 billion to IBM’s AI book of business. By adopting a strategy to embed its AI infrastructure software into the cloud ecosystem of GenAI tools and copilots already widely accepted by customers, IBM ensures it stays relevant with these cutting-edge workloads.

Oracle (less than $100 million in GenAI revenue annually): With the Oracle Cloud Infrastructure (OCI) GenAI Service hitting general availability in January and a code assist tool only recently launched into preview, Oracle has been late to the GenAI game. But the company has highlighted several multibillion-dollar contracts for AI training on OCI, which speaks to its tight relationship with NVIDIA and ample supply of GPUs.

As an API-based service providing out-of-the-box access to LLMs for generic use cases, the OCI GenAI Service on its own does not necessarily differ from what other hyperscalers are doing. What does stand out is that Oracle offers the entire SaaS suite. Given that all Fusion SaaS instances are hosted on OCI, where the GenAI service was built, Oracle can deliver GenAI capabilities to SaaS customers at no added cost.

This means Oracle’s GenAI monetization will be purely from an infrastructure perspective. GPU supply and the cost efficacy of OCI will help Oracle bring new workloads into the pipeline, and we will see a bigger impact to growth in 2025. For context, Oracle’s remaining performance obligations balance (though some includes Cerner) is $98 billion.

Dive Into the Future of GenAI with TBR Analysts Patrick Heffernan, Bozhidar Hristov and Kelly Lesiczka

Beyond revenue generation, cost savings is part of the value proposition for cloud vendors and customers alike

Many of the leading IT vendors’ GenAI strategies have centered on investing in solutions for customers. However, vendors have also been serving as customer zero for the technology by implementing it internally. The results from their early implementations seem very much like end-customer use cases, which focus on cost savings and efficiency as the easiest benefits to realize. While many IT vendors have seen operating expenses and headcount level off over the past couple of quarters, implying that AI has had some impact on company efficiency, IBM and SAP have both explicitly stated AI’s impact on their operating models.

IBM was one of the earliest vocal proponents for the labor-saving benefits AI could bring to its business. In mid-2023 CEO Arvind Krishna announced a hiring freeze and shared an expectation that AI would replace 8,000 jobs. IBM remains focused on driving productivity gains, which it is largely doing by lowering the internal cost of IT and rebalancing the global workforce. This includes using AI to automate back-office functions. Such efforts have IBM on track to deliver a minimum of $3 billion in annual run-rate savings by the end of 2024.

Meanwhile, SAP’s decision to increase its planned FTE reallocation from a previous target of 8,000 to a new range of between 9,000 and 10,000 FTEs shows the company is committed to improving operating efficiency. While the bulk of the restructuring will consist of reallocating FTEs into lower-cost geographies and strategically important business units, taking a customer-zero approach with GenAI is also a component. SAP is leveraging business AI tools focused on areas like finance & accounting and human resources to reduce the labor intensity within the respective business units.

Just like end customers, vendors are investing significantly now in hopes of generating long-term GenAI returns

As seen in TBR’s Cloud Customer Research streams, customers have been investing in GenAI solutions with some haste, forgoing clear ROI measurements or typical budgeting procedures. Customers, as well as the major vendors we cover, have a sense of urgency around GenAI and share the feeling that if they do not embrace these new solutions now, it could place them at a long-term competitive disadvantage. If customers are not making full use of GenAI capabilities, their competitors will be more efficient and productive and capture more growth opportunities. For vendors, the ability to not only deliver GenAI capabilities but also do so at scale will be a competitive necessity for decades to come.

In this regard, customers and vendors find themselves in a similar situation, investing in GenAI now just for the possibility of a future advantage, but the scale of investments required are quite different. Customers have the good fortune of leveraging scalable, subscription-based services for many of these GenAI technologies. Customers are still extending their IT budgets and paying more to incorporate GenAI, but they do not have large fixed costs and long-term commitments at this point.

Vendors, on the other hand, need to make significant investments, even beyond the already huge levels of investment to support cloud services, to capitalize on the GenAI opportunity. The scale of investment cannot be understated for the largest cloud platform providers like AWS, Microsoft, Google and Oracle. All of these vendors were already investing tens of billions of dollars annually to support data center and infrastructure build-outs.

The unique data center and infrastructure requirements to deliver GenAI solutions, including the GPU-based systems, are driving double-digit to triple-digit increases in capex spending for leading vendors. Not only is the level of spending noticeable, the time periods for the returns are also lengthy. In communicating those increased expenses to investors and Wall Street analysts, vendors like Microsoft messaged the returns from these investments playing out over the next 15 years, a time horizon seldom mentioned previously.

https://tbri.com/wp-content/uploads/2024/09/stock-investment-chart_marcus-millo_getty-images_canva-pro.png10801080Catie Merrill, Senior Analysthttps://tbri.com/wp-content/uploads/2021/09/TBR-Insight-Center-Logo.pngCatie Merrill, Senior Analyst2024-09-09 09:20:302024-09-11 09:54:40Investing Big in GenAI Today: The Key to Unlocking Massive Long-term Returns

TBR’s Enterprise Edge Compute Market Landscape provides insights on marketwide trends among 16 vendors across the edge stack. The research focuses on the infrastructure, software and services that facilitate edge data processing and analysis. Vendor coverage includes Amazon Web Services, Google Cloud, IBM, Amazon Web Services, IBM, Hewlett Packard Enterprise and more. To access the entire report and dataset, sign up for your TBR Insight Center™ free trial today!

Cloud adoption is on the rise, but for many customers, particularly those deploying workloads across multiple clouds, latency, data flow, privacy and overall business resiliency remain core challenges.

Edge computing is an emerging segment in IT, giving customers a way to supplement their cloud and IT core investments by processing data locally for minimum latency and backing it up to an adjacent environment for use cases like analytics and application development.

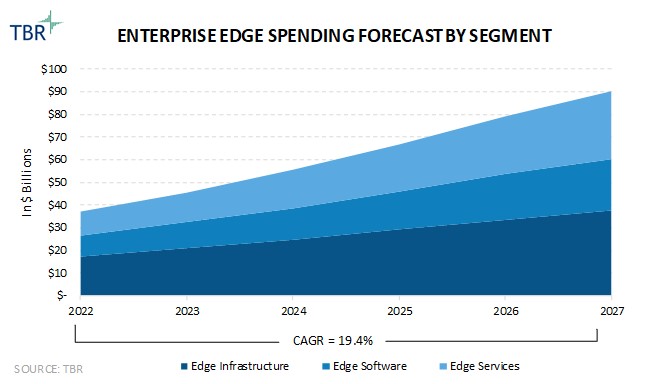

Enterprise Edge Computing Market Forecast

TBR research estimates the enterprise edge computing market will grow at a 19.4% CAGR from 2022 to 2027, surpassing $90 billion by 2027. Professional and managed services will remain the fastest-growing segment, followed by software, at estimated CAGRs of 23.2% and 19.8%, respectively.

We continue to revise our enterprise edge computing market forecast to account for the pullback in spending across traditional IT and cloud markets. Deceleration of growth in the edge market will not be as severe as in other markets due to the strategic nature of edge investments.

Further, although the enterprise edge market will benefit from the hype surrounding AI in 2024, many pilot projects may not enter production and more concrete use cases around edge AI need to be developed.

Enterprise Edge Computing Adoption Remains Sluggish, With Other ROI-friendly Alternatives Taking Precedence

Edge Computing Expansion Lags Compared to Other Deployment Methods

According to TBR’s 2Q24 Infrastructure Strategy Customer Research, 34% of respondents expect to expand IT resources at edge sites and branch locations over the next two years. But this is noticeably lower than the 55% who plan to expand IT resources within centralized data centers, while the central cloud and managed hosting are also gaining more traction.

The possibility of large capital outlays and an unclear path to ROI remain the biggest adoption hurdles to edge technology, with some customers exploring other alternatives that have a clearer path to ROI.

CrowdStrike Outage Reinforces Edge Computing’s Role in Decentralized IT

There are many lessons to take away from the CrowdStrike incident in July, where a faulty update caused Microsoft Windows to fail, resulting in a major disruption to global businesses. The issue extends well beyond cybersecurity and speaks to the risk of having a centralized IT architecture with limited disaster recovery and backup solutions in place.

The CrowdStrike outage has been called out by many edge computing advocates and business leaders, including ZEDEDA CEO Said Ouissal, who argues that a distributed architecture that uses more autonomous capabilities, including edge-specific operating systems, is a much more efficient approach, as opposed to having to manually reset multiple endpoints, as was the case with CrowdStrike.

This message certainly has merit, as distributed architectures that are built from the ground up and can effectively extend resources from cloud to edge have been gaining traction among customers and vendors. But securing these distributed architectures remains a big challenge, and vendors have a lot of work to do to assure customers their data is secure across the entire infrastructure landscape.

Hyperscalers Continue to Address the Edge Opportunity, and GenAI May Exacerbate This Trend

AI and generative AI (GenAI) have the potential to gain a lot of traction at the edge, and the hyperscalers are well positioned to address this opportunity. With their vast access to data, the hyperscalers will be a natural choice for customers that do not want to move their GenAI solutions to a separate compute ecosystem but want to process the data closer to the point of use.

We continue to see hyperscalers move into the edge space, with Google Cloud’s air-gapped configuration of Google Distributed Cloud and the continued expansion of Amazon Web Services Local Zones, including Dedicated Local Zones, among the key examples.

https://tbri.com/wp-content/uploads/2024/08/cloud-computing-technology_just-super_getty-images_canva-pro.png10801080Catie Merrill, Senior Analysthttps://tbri.com/wp-content/uploads/2021/09/TBR-Insight-Center-Logo.pngCatie Merrill, Senior Analyst2024-09-09 07:11:002024-08-30 10:18:58Edge Computing’s Role in Tackling Latency, Privacy and Resiliency Challenges

Mature alliance partnerships have enabled vendors across the spectrum to collaborate as they realize the value of the ecosystem. Cultural, portfolio and leadership DNA have shaped vendors’ behavior when it comes to go-to-market efforts and partner strategies, which is not surprising given that vendors often lean on what they do best when pursuing opportunities. Go deeper in ecosystem research with our new Voice of the Partner Ecosystem Report. Access the entire report with a free trial of TBR Insight Center™. Sign up today!

GenAI Could Disrupt Existing Relationships If Partners Cannot Demonstrate Agility Backed by Common Governance

State of the Ecosystem Landscape

With new technologies including generative AI (GenAI) influencing vendors’ strategies, we expect new relationships to emerge, whether bidirectional or multidimensional, as vendors realize that positioning themselves as end-to-end providers is a thing of the past. We understand that the buyers will be the ultimate judges of these efforts, but laying the groundwork, backed by robust common governance and accountability, will separate leading and lagging alliances.

Overall, vendors across the profiled groups are satisfied with their alliance partners, despite differences in commercial, staffing and client management models. We believe the value of the ecosystem has placed some pressure on vendors to think creatively about ways to monetize opportunities with partners.

Thus far, the services vendors have demonstrated greater agility compared to other vendors, such as OEMs, that are often stuck in their traditional ways of doing business. Industry specialization appears to be one area where all vendors agree, and we believe this industry focus provides the connecting tissue between relationships, as clients — direct and joint — are all part of a particular vertical, compelling vendors to either demonstrate value through industry know-how or rely on partners.

Vendor and Partner Expectations

Differences in expectations around what will drive the business in the next two years provide a reality check that vendors’ priorities do not always align with their partners’ views. One can attribute some of this difference to vendors’ place in the traditional technology life cycle.

For instance, OEMs try to accelerate the hardware refresh cycle and sell more infrastructure to support growth in newer areas such as 5G and edge, whereas cloud vendors remain focused on spinning the meter to support ongoing cloud initiatives.