Strategy returns, pyramids crumble and everyone plays together nicer in the sandbox

TBR expects monumental changes to the digital transformation landscape in 2025, from the resurgence of strategy consulting to generative AI (GenAI) adoption impacting everyone in the IT services and consulting ecosystem. Underpinning these changes will be leaders’ sharpened focus on how partners across the ecosystem go to market together, align sales teams and enhance knowledge sharing.

In this TBR Insights Live session, TBR’s Professional Services analyst team, Patrick M. Heffernan, Boz Hristov and Kelly Lesiczka give an exclusive review of TBR’s 2025 Digital Transformation Predictions special report, Digital Transformation in 2025: From Optimization Fatigue to Business Model Reinvention. Don’t miss this opportunity to learn how the latest industry challenges will impact your company’s strategy in the coming year!

In the above session on the digital transformation outlook for 2025 you’ll learn:

Why strategy consulting will rebound in 2025, and which consultancies will benefit

Discussion of ERP consolidation (e.g., S4Hanna, Main frame modernization)

Cloud migration services, custom apps development and workflow management

How GenAI-enabled solutions will upend organizational structures and business models for IT services and consultancies, with follow-on effects for partners

How the emergence of ecosystem intelligence as a strategic priority will impact IT services companies, consultancies and technology alliance partners

Discussion points from Digital Transformation Outlook: Strategy Rebound, GenAI Impact and Ecosystems Importance in 2025

Strategy consulting market has stagnated for a few years but is changing

Among management consultancies and IT services companies, strategy consulting has lagged in recent years.

What conditions will create a better market for strategy consulting?

Which companies will benefit from an uptick in demand for strategy consulting?

Visit this link to download this session’s presentation deck here.

TBR Insights Live sessions are held typically on Thursdays at 1 p.m. ET and include a 15-minute Q&A session following the main presentation. Previous sessions can be viewed anytime on TBR’s Webinar Portal.

https://tbri.com/wp-content/uploads/2024/12/Digital-Predictions-Webinar_Square.png10801080TBRhttps://tbri.com/wp-content/uploads/2021/09/TBR-Insight-Center-Logo.pngTBR2024-12-23 11:54:122025-02-27 16:53:05Digital Transformation Outlook: Strategy Rebound, GenAI Impact and Ecosystems Importance in 2025

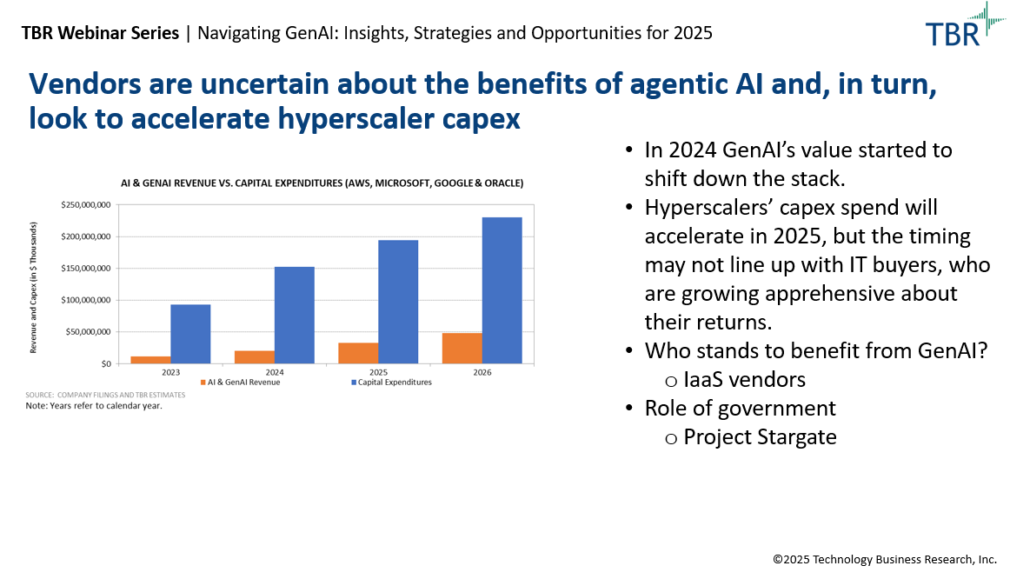

Cloud market growth will slow in 2025, but will activity follow?

Given the scale and maturity of the cloud market, TBR expects the pace of revenue growth to slow in 2025. In terms of activity, we expect vendors and end customers to make pivotal changes to their cloud strategies in 2025.

In this TBR Insights Live session, TBR’s Cloud team — Principal Analyst Allan Krans, Senior Analyst Catie Merrill and Analyst Alex Demeule — on discuss how generative AI (GenAI) will impact cloud vendors’ long-term position in the market and cloud customers’ adoption efforts in 2025.

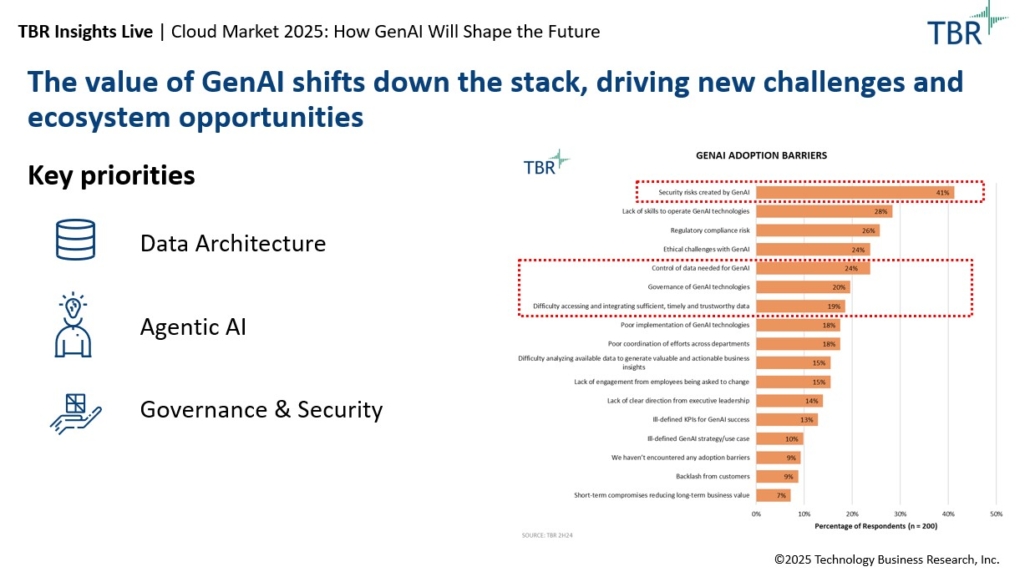

Discussion points from Cloud Market 2025: How GenAI Will Shape the Future

The value of GenAI shifts down the stack, driving new challenges and ecosystem opportunities

Key priorities: Data architecture, agentic AI, and governance and security

Visit this link to download this session’s presentation deck here.

TBR Insights Live sessions are held typically on Thursdays at 1 p.m. ET and include a 15-minute Q&A session following the main presentation. Previous sessions can be viewed anytime on TBR’s Webinar Portal.

https://tbri.com/wp-content/uploads/2024/12/Cloud-Predictions-Webinar_Square.png10801080TBRhttps://tbri.com/wp-content/uploads/2021/09/TBR-Insight-Center-Logo.pngTBR2024-12-23 11:45:202025-02-07 09:35:43Cloud Market 2025: How GenAI Will Shape the Future

GenAI boom times ahead for companies embracing their own business model disruption

The waning generative AI (GenAI) hype has exposed underlying issues such as expensive cloud commitments and fragmented data strategies, creating opportunities for companies that emphasize ROI, complementary technologies and cost management. Adding to the complexity, rising energy costs and heightened awareness of GenAI-related security risks are further shaping this uncertain yet opportunity-filled environment.

In this TBR Insights Live session Principal Analyst Patrick Heffernan, Principal Analyst Boz Hristov and Senior Analyst Kelly Lesiczka give an exclusive review of TBR’s AI and GenAI Market Landscape, which highlights expectations for both individual leading vendors and the GenAI space overall. The trio also discuss buyers’ GenAI maturity and review specific examples of services and technology companies’ activities in 2024 as well as what to expect across the GenAI landscape in 2025. Don’t miss this opportunity to learn how GenAI will impact your strategy in the coming year!

In the above session on navigating GenAI in 2025 you’ll learn:

How GenAI is impacting buyer-vendor relationships and what is next in the evolution of their business models

How tech and services companies are using alliances to extend their reach within enterprises and across the larger GenAI — and emerging tech — ecosystem

Which consultancies, IT services vendors, cloud and software companies, and infrastructure players are best positioned for the next wave of GenAI adoption

Visit this link to download this session’s presentation deck here.

TBR Insights Live sessions are held typically on Thursdays at 1 p.m. ET and include a 15-minute Q&A session following the main presentation. Previous sessions can be viewed anytime on TBR’s Webinar Portal.

https://tbri.com/wp-content/uploads/2024/12/GenAI-Predictions-Webinar_1Q24_Square.png10801080TBRhttps://tbri.com/wp-content/uploads/2021/09/TBR-Insight-Center-Logo.pngTBR2024-12-23 11:35:072025-01-31 11:34:14Navigating GenAI: Insights, Strategies and Opportunities for 2025

6G’s Fate Will Likely Be Determined by the Level of Government Intervention

The telecom industry continues to struggle with realizing new revenue and deriving ROI from 5G, even after five years of market development. Due to this persistent challenge, to which TBR continues to see no clear solution or catalyst on the horizon to change the situation, communication service providers’ (CSP) appetite and scope of investment in 6G will likely be limited. This lack of clear ROI for the private sector to justify investing sufficiently in 6G puts the fate of the technology into the hands of the government.

In this TBR Insights Live session TBR Telecom Principal Analyst Chris Antlitz gives an exclusive review of top predictions from 6G’s Fate Will be Determined by the Level of Government Intervention, part of TBR’s 2025 Predictions special report series. Don’t miss this opportunity to learn how 6G will impact your strategy in the coming year!

In this above session on 6G you’ll learn:

What spectrum bands 6G will likely leverage

How 6G will shape CSPs’ capex investments

How governments might get involved to ensure 6G becomes a reality

Discussion points from 6G: How Government Intervention Globally Will Shape the Next Generation of Telecom

Telecom industry’s struggles with 5G are likely to extend to 6G

CSPs have spent several hundred billion dollars on 5G infrastructure and spectrum globally thus far, with ROI (i.e., new, profitable revenue growth) still absent.

5G investment has been justified thus far as a way to reduce cost per bit and as a marketing play to retain customers.

Fixed wireless access (FWA) has been successful but does not significantly offset overall 5G investments.

Only about 20% of CSPs globally have begun deploying 5G core (standalone architecture) thus far, which is a prerequisite for 6G.

Technological complexity is increasing (e.g., open vRAN, AI, edge computing, network slicing, security), hindering progress.

Sustained, higher interest rates = higher cost of capital = tighter capex environment

Visit this link to download this session’s presentation deck here.

TBR Insights Live sessions are held typically on Thursdays at 1 p.m. ET and include a 15-minute Q&A session following the main presentation. Previous sessions can be viewed anytime on TBR’s Webinar Portal.

https://tbri.com/wp-content/uploads/2024/12/6G-Predictions-Webinar_Square.png10801080TBRhttps://tbri.com/wp-content/uploads/2021/09/TBR-Insight-Center-Logo.pngTBR2024-12-23 11:17:502025-01-24 13:46:016G: How Government Intervention Globally Will Shape the Next Generation of Telecom

AI PCs Must Define a New Era of Personal Computing

The introduction of the neural processing unit (NPU), a dedicated processor for AI-related tasks, has created an opportunity for AI PCs to shift from a niche use case to a product that can be consumed by the masses in both consumer and commercial users.

Despite this new potential, hurdles exist in AI PCs, spurring a new wave of PC purchasing. First, buyers need significant education on what an AI PC is, what it can be used for and how they stand to benefit from purchasing one. Second, the ISV ecosystem needs to catch up to the pace of hardware innovation and create more compelling use cases that leverage the NPU.

In this TBR Insights Live session Senior Analyst Ben Carbonneau and Research Analyst Alek Maxfield give an exclusive review of TBR’s 2025 Devices Predictions special report, AI PCs: Progress, Potential and Hurdles in Redefining the Market in 2025. Don’t miss this opportunity to learn how the latest industry challenges will impact your strategy in the coming year!

In the above session on AI PCs you’ll learn:

The potential impact of AI PCs on PC refresh cycles in 2025

How PC makers will set themselves apart

Expectations for the PC market overall in 2025 based on TBR’s latest research and analysis

PC market revenue will increase by single digits during 2025

Demand is expected to accelerate in the second half of the year, with commercial demand continuing to outpace consumer

PC market refresh drivers for 2025:

Large, aging install base

End of life for Windows 10

AI PCs – ongoing advancements and new use cases

TBR Insights Live sessions are held typically on Thursdays at 1 p.m. ET and include a 15-minute Q&A session following the main presentation. Previous sessions can be viewed anytime on TBR’s Webinar Portal.

https://tbri.com/wp-content/uploads/2024/12/AI-PC-Predictions-Webinar_Square.png10801080TBRhttps://tbri.com/wp-content/uploads/2021/09/TBR-Insight-Center-Logo.pngTBR2024-12-23 10:56:452025-01-17 11:37:41AI PCs in 2025: Unlocking Mass Appeal and Overcoming Market Challenges

Utilizing AI Is the Top IT Organization Priority for the Next 2 Years

The industry enthusiasm surrounding AI has quickly led to shifts in organizations’ strategic priorities and expected investments such as demand for servers. Despite the hype, few organizations have operationalized GenAI to date. Instead, most are focused on overcoming initial barriers to adoption, including understanding the business implications of this new technology frontier.

The buzz around AI has permeated the minds of IT leaders at many organizations, with 44% of respondents* indicating that utilizing AI is a top priority for the next two years, outpacing all other priorities surveyed.

GenAI Has Generated Significant Interest Among IT Buyers of All Verticals and Company Sizes, But Few Have Implemented the Technology to Date

Generative AI (GenAI) is a hot topic, but only 22% of respondents* indicated their organization is using GenAI-based technology in day-to-day operations, suggesting that many organizations want to leverage GenAI to drive transformation but are unsure of where to begin. Most respondents are in a conceptual phase, with 57%* currently discussing GenAI use cases or testing GenAI technologies.

Not all organizations wish to build their own bespoke GenAI solutions, with 18% of respondents indicating they are waiting for turnkey solutions that can be applied to their business. Only 3% of respondents* are not considering GenAI at all.

There were no major differences in current levels of GenAI adoption relative to organization size.

Respondents from the industrials and technology verticals are slightly ahead of others in terms of using GenAI in day-to-day operations. Public sector lags considerably, with only 9% of respondents using GenAI today.

Healthcare respondents were most likely to be in the testing phase, at 47%.*

Watch On Demand: Next-generation AI PCs: What It May Mean for the Next Refresh Cycle

Most Respondents Expect to Use GenAI Solutions Tailored to Their Use Case, While a Smaller Subset Will Adopt Software With Embedded GenAI Features

Overall, 65% of respondents* using or considering GenAI will run GenAI on their own infrastructure, and 45%* will use public cloud, signaling that GenAI projects will take on a hybrid strategy. It is worth noting that the respondents answering this survey are decision makers for purchasing IT infrastructure, and therefore may be more biased toward using their organization’s private infrastructure for GenAI versus individuals who are focused on public cloud.

For some organizations, using GenAI will be based solely on enhancements to ISV applications and not their own custom build-outs. Of the respondents using or considering GenAI, 13%* expect to only use software and applications with GenAI features and do not plan to build GenAI use cases in public cloud or on their own infrastructure.

Enterprises appear to be most wary of using public cloud for GenAI technologies.

Vendors Engaging Customers on GenAI Will Need to Start the Journey by Establishing Trust in Handling Data and Navigating Legal and Ethical Concerns

The greatest barriers to organizations adopting GenAI are those at the heart of the GenAI debate: ensuring data privacy and assessing the legal and ethical risks of using GenAI technology. IT decision makers are expected to ensure their organizations are operating according to standards; however, they are inexperienced with the technologies to be adopted and vendors have limited use cases to showcase at this time to assuage these concerns.

More tactical challenges, such as long lead times to purchase AI-enabled servers or structuring data for machine learning, are farther down the list but may become greater barriers over time when organizations move from conceptualization to implementation of GenAI solutions.

Enterprises are by far the most concerned with ensuring data privacy, as 56% of enterprise respondents* consider it a top barrier compared to 31% of respondents overall.

Obtaining budget is of greater concern to small and midsize businesses than to enterprises.

Financial services respondents were most likely to be concerned with more tactical issues, such as addressing hardware shortages, structuring data and finding vendors to help deploy GenAI solutions.

Access all of TBR’s customer research data on GenAI adoption in IT infrastructure with a subscription to TBR Insight Center™. Start your free trial today!

*Survey data and analysis in this section are excerpts from TBR’s 2Q24 Infrastructure Strategy Customer Research. The survey was fielded in April and May of 2024 and focuses on the overall investment strategies of IT infrastructure purchasers. Survey respondents are IT decision makers based in the U.S. who are responsible for servers and storage purchase decisions at companies with 250 or more employees. Small business was defined as organizations with 250 to 999 employees, medium business as organizations with 1,000 to 4,999 employees, and enterprise as organizations with 5,000 or more employees.

https://tbri.com/wp-content/uploads/2024/12/hand-plaing-wooden-geometric-shapes_dalaifood_canva-pro.png10801080Ben Carbonneau, Senior Analysthttps://tbri.com/wp-content/uploads/2021/09/TBR-Insight-Center-Logo.pngBen Carbonneau, Senior Analyst2024-12-20 13:00:382024-12-09 13:01:27AI Buzz Sparks IT Infrastructure Shifts, but Privacy and Strategic Challenges Are Impacting Adoption

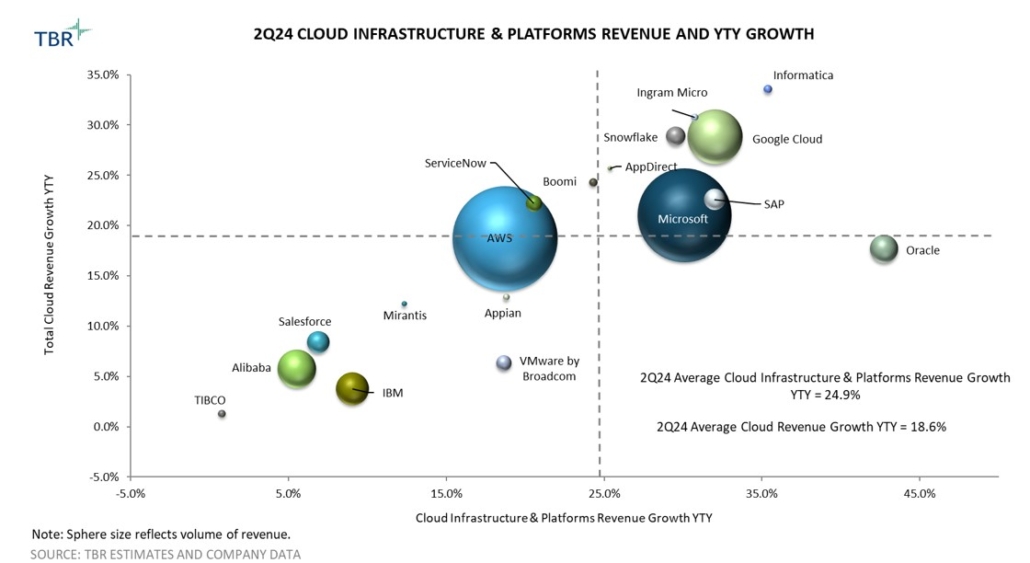

Enterprise Migrations and Large-Scale M&A Are Influencing the IaaS and PaaS Market

Current State of the Infrastructure as a Service Market

Among benchmarked Infrastructure as a Service (IaaS) vendors, average revenue growth increased 21% year-to-year in 2Q24, marking the fourth consecutive quarter of acceleration. There are two primary factors at play: enterprise IT modernization activity, which is much stronger now than it was this time last year, and generative AI (GenAI).

Top hyperscalers Amazon Web Services (AWS) and Microsoft are capturing legacy Oracle and SAP workloads as customers continue to migrate to the cloud to not only outsource their IT operations but also drive lasting business value. Though the geopolitical outlook is increasingly uncertain, we expect customers will continue to prioritize more traditional “lift and shift” migrations, and steps vendors are taking to deliver more integrated solutions could help. For instance, by the end of 2024, Oracle’s database services will officially be available on AWS, Microsoft Azure and Google Cloud Platform (GCP), which could be a big growth tailwind for these vendors. For context, converting Oracle’s remaining database support install base to the cloud represents a roughly $18 billion incremental revenue opportunity for these hyperscalers, including Oracle itself.

Regarding GenAI, investments in AI compute and new data centers are translating into top-line growth. Most vendors report they have multibillion-dollar AI and GenAI businesses, though this is minuscule compared to the tens of billions of dollars these vendors are investing. Vendor capex guidance for 2025 suggests that the level of investment will only increase, although we do expect this is when GenAI fatigue will hit and many customers may begin to re-evaluate their IT priorities.

Current State of the Platform as a Service Market

The Platform as a Service (PaaS) market is similarly growing behind GenAI adoption, as many customers, who still have a fear-of-missing-out mentality, are spinning up new workloads natively in the cloud with services like Amazon Bedrock, Microsoft Azure OpenAI and Google Vertex AI.

The PaaS market will similarly be impacted by GenAI disillusionment, but we believe this trend will also cause customers to focus more on the data layer, prompting them to take a second look at strategies around governance, data quality and integration for long-term AI success.

Another key trend driving PaaS market growth is M&A. IT leaders are acquiring to enter new markets and access IP they can ultimately sell as part of an entire end-to-end suite of offerings, as customers continue to crave more simplified, integrated solutions. By far the best example is Cisco’s acquisition of Splunk, which added $960 million to Cisco’s top line in 2Q24 and is quickly making Cisco a rising force in PaaS with its observability portfolio. IBM’s proposed acquisition of HashiCorp, which is expected to close by the end of this year, would be another transformative deal that would put IBM squarely into the Terraform space and deliver synergies with Red Hat that will be attractive to unsatisfied VMware customers.

Cloud Infrastructure and Platform Revenue Leaders

Steps Microsoft Is Taking to Elevate Its Data Portfolio as Part of the Broader AI Strategy Will Fuel Azure Growth and Marginalize AWS’ Segment Lead

Amazon Web Services: AWS continues to ride a wave of accelerating revenue growth and will cross the $100 billion threshold in annual sales by the end of 2024. Making it as easy as possible for customers to build GenAI applications in the cloud with Amazon Bedrock’s unified API, and adjacent developer tools like App Studio and SageMaker, is integral to AWS’ strategy and ability to drive IaaS growth. At this point, there are probably well over 10,000 customers using Amazon Bedrock for a range of generic use cases like text generation and virtual assistants.

Microsoft: Though AI infrastructure constraints caused Azure revenue to dip 2 percentage points to 29% in 2Q24, Azure is growing faster than AWS despite becoming larger and closing in on AWS’ revenue volume. Steps Microsoft is taking to advance its PaaS strategy through solutions like Fabric will continue to fuel Azure growth and help protect Microsoft’s lead in the AI space. For context, the number of Azure AI customers also using Microsoft’s data and analytics tools grew nearly 50% year-to-year in 2Q24, while Microsoft Fabric has now reached 14,000 paid customers.

Google Cloud: Recognizing that GenAI leadership stems from the infrastructure foundation, Google Cloud has been heavily building out its infrastructure portfolio by supporting not only NVIDIA’s Blackwell chips, which are expected to be available on GCP in early 2025, but also its own hardware. This includes Axion, Google Cloud’s first Arm-based processor that will support a range of GCP services, including data services key for GenAI like Dataproc and Dataflow. In 2Q24 Google Cloud also announced its sixth-generation TPU (tensor processing unit).

https://tbri.com/wp-content/uploads/2024/12/cloud-computing-concept_monster-ztudio_canva-pro.png10801080Catie Merrill, Senior Analysthttps://tbri.com/wp-content/uploads/2021/09/TBR-Insight-Center-Logo.pngCatie Merrill, Senior Analyst2024-12-19 12:52:512024-12-09 12:56:28GenAI, IT Modernization and Strategic M&A Drive Infrastructure as a Service and Platform as a Service Growth

2025 Predictions is a series of special reports examining market trends and business changes TBR expects in the coming year for AI PCs, cloud market share, digital transformation, GenAI, ecosystems and alliances, and 6G.

Top Predictions for Ecosystems & Alliances in 2025

Cloud providers will have their hands full juggling ecosystem investments amid a changing technology landscape

The most successful IT services companies and consultancies will be the ones that partner best

The strategic shift to ecosystem intelligence in 2025

In the last few years, ecosystem intelligence has gained ground on competitive intelligence as the use case clients most frequently employ to leverage TBR’s IT services, professional services and digital transformation data and analysis, often in an effort to answer the following questions:

Can your alliance partners tell your clients what makes you special?

Do your alliance partners’ sales teams know what value you bring to the ecosystem?

Are you sure you placed your strategic ecosystem bets on alliance partners that are well positioned for the next growth wave?

Are your competitors gaining ground with your common alliance partners through sales programs, go-to-market motions and training that you are not doing?

This shift to ecosystem intelligence reflects three broader trends:

Enterprise buyers want to deal with fewer technology vendors, increase transparency around their IT spend and realize faster returns on technology investments.

Portfolio and capability expansion — PwC has expanded into managed services, HCLTech into software, Amazon Web Services into professional services and Lenovo into consulting — has created a more fluid ecosystem, where partnering with competitors and competing against alliance partners have become the norm.

Perhaps running as a crosscurrent to the other two trends, the top-performing companies have chosen to play primarily to their strengths, staying in their lane and partnering better, rather than building out capabilities and scale.

In 2025 IT services companies and consultancies will refine their alliances, winnowing lists of 100-plus technology partners to the handful that drive more than 90% of their business, articulate a clear joint value proposition, and align at both the leadership and sales force levels. A technology- and partner-agnostic approach was always a bit of a fiction and in the coming years will become a relic of the past. To make all that happen, IT services companies, cloud and on-premises infrastructure vendors, and consultancies will invest in ecosystem intelligence and elevate alliance management within their organizations.

To read the entire 2025 Ecosystems & Alliances Predictions special report, request your free copy today!

https://tbri.com/wp-content/uploads/2024/12/TBR-Ecosystem-Predictions-2025-Site.png10801080Patrick Heffernan, Practice Manager and Principal Analysthttps://tbri.com/wp-content/uploads/2021/09/TBR-Insight-Center-Logo.pngPatrick Heffernan, Practice Manager and Principal Analyst2024-12-19 09:57:452026-01-09 13:06:33Ecosystem Intelligence: Key Strategic Changes for 2025

2025 Predictions is a series of special reports examining market trends and business changes TBR expects in the coming year for AI PCs, cloud market share, digital transformation, GenAI, ecosystems and alliances, and 6G.

Top Predictions for GenAI in 2025

GenAI will continue to revolutionize mission-critical functions and day-to-day operations at federal civilian, defense and intelligence agencies

Cloud vendors will splurge on AI investments even as customers grow apprehensive

Infrastructure vendors’ focus will shift from serving cloud companies to making a massive push in enterprise AI

The energy problem is likely to slow the pace of AI market development significantly

GenAI upends pyramids, even as enterprises slow their AI roll

In 2024 the AI and generative AI (GenAI) landscape faced four key challenges: rising costs, driven by growing investments in data and infrastructure; talent and training gaps; regulatory uncertainty; and macroeconomic pressures. These obstacles will persist into 2025, with additional challenges in the GenAI space becoming increasingly evident.

According to TBR research, the waning GenAI hype has exposed underlying issues, including expensive cloud commitments and fragmented data strategies, creating opportunities for companies that emphasize ROI, complementary technologies and cost management. Adding to the complexity, rising energy costs and heightened awareness of GenAI-related security risks are further shaping this uncertain yet opportunity-filled environment.

But after two years of GenAI disruption, a clear trend is emerging across the ecosystem: strategic partnering is becoming essential. Companies such as McKinsey & Co, Wipro, Dell Technologies, Amazon Web Services (AWS) and NVIDIA are adopting this approach, recognizing that no single organization can deliver comprehensive GenAI-enabled solutions alone. Instead, success increasingly depends on leveraging the technology and expertise of ecosystem partners.

https://tbri.com/wp-content/uploads/2024/12/TBR-GenAI-Predictions-2025-Site-Imag.png10801080Patrick Heffernan, Practice Manager and Principal Analysthttps://tbri.com/wp-content/uploads/2021/09/TBR-Insight-Center-Logo.pngPatrick Heffernan, Practice Manager and Principal Analyst2024-12-18 12:29:272024-12-18 12:29:27GenAI in 2025: Revolutionizing Agencies and Reshaping Ecosystems

2025 Predictions is a series of special reports examining market trends and business changes TBR expects in the coming year for AI PCs, cloud market share, digital transformation, GenAI, ecosystems and alliances, and 6G.

Top Predictions for Digital Transformation in 2025

Transformation comes roaring back

GenAI upends pyramids, even as enterprises slow their AI roll

Ecosystem intelligence becomes a strategic advantage

Of the three major focus areas for TBR’s 2025 predictions — strategy consulting, generative AI (GenAI) and ecosystem intelligence — the first may seem a long shot, the second too obvious to be new, and the third too well established to be changing much. All three will upend expectations in 2025 with wildly varying results for the IT services companies and consultancies that TBR tracks and for their technology partners.

When OEMs first started releasing AI PCs, they shared expectations that the advent of this new product category would help drive the next major PC refresh cycle. However, even as vendors continue to roll out new generations of AI PCs containing increasingly powerful NPUs, adoption remains relatively slow. This is because the presence of an NPU itself does nothing to increase the value of AI PCs compared to other similar devices, and AI PCs require an additional layer in the form of applicable software that makes AI-enabled features easily accessible and user-friendly.

Strategy consulting’s rebound will come from a renewed push for growth, underpinned by business model reinvention. GenAI will profoundly change the structures and business models of IT services companies and consultancies, all while enterprises struggle to take GenAI to scale (and hey, how about some strategy consulting to help with those struggles?).

The need to stand out in a crowded market will compel technology leaders to better align their strategic partnerships, elevating the need for refined and tested ecosystem intelligence and taking alliance management from a good-to-have to strategically critical.

https://tbri.com/wp-content/uploads/2024/12/TBR-Digital-Predictions-2025-Site-Im.png10801080Patrick Heffernan, Practice Manager and Principal Analysthttps://tbri.com/wp-content/uploads/2021/09/TBR-Insight-Center-Logo.pngPatrick Heffernan, Practice Manager and Principal Analyst2024-12-16 09:22:392024-12-16 09:22:39Digital Transformation in 2025: From Optimization Fatigue to Business Model Reinvention

We may request cookies to be set on your device. We use cookies to let us know when you visit our websites, how you interact with us, to enrich your user experience, and to customize your relationship with our website.

Click on the different category headings to find out more. You can also change some of your preferences. Note that blocking some types of cookies may impact your experience on our websites and the services we are able to offer.

Essential Website Cookies

These cookies are strictly necessary to provide you with services available through our website and to use some of its features.

Because these cookies are strictly necessary to deliver the website, refusing them will have impact how our site functions. You always can block or delete cookies by changing your browser settings and force blocking all cookies on this website. But this will always prompt you to accept/refuse cookies when revisiting our site.

We fully respect if you want to refuse cookies but to avoid asking you again and again kindly allow us to store a cookie for that. You are free to opt out any time or opt in for other cookies to get a better experience. If you refuse cookies we will remove all set cookies in our domain.

We provide you with a list of stored cookies on your computer in our domain so you can check what we stored. Due to security reasons we are not able to show or modify cookies from other domains. You can check these in your browser security settings.

Other external services

We also use different external services like Google Webfonts, Google Maps, and external Video providers. Since these providers may collect personal data like your IP address we allow you to block them here. Please be aware that this might heavily reduce the functionality and appearance of our site. Changes will take effect once you reload the page.

Google Webfont Settings:

Google Map Settings:

Google reCaptcha Settings:

Vimeo and Youtube video embeds:

Privacy Policy

You can read about our cookies and privacy settings in detail on our Privacy Policy Page.