Fujitsu’s Innovative Approach to GenAI: Amalgamated AI Strategies

At a new Silicon Valley facility, Fujitsu hosted about 20 industry analysts and over 200 guests for a day of presentations on emerging technologies like quantum computing and AI. The following special report reflects conversations TBR had with Fujitsu leaders and highlights Fujitsu’s role in the technology ecosystem.

Fujitsu’s Superpower: Fusing Compute Power with AI

After a year of relentless hype about the promises of generative AI (GenAI), Fujitsu Research’s leaders structured their presentations during the Fujitsu ActivateNow Technology Summit around a relatively simple and compelling story: GenAI is fundamentally AI, and Fujitsu has successfully deployed a wide range of AI-enhanced solutions.

By observing which business challenges can be addressed with AI, and then developing and productizing AI-enhanced solutions, Fujitsu has built an amalgamation of AI solutions, a collection that is worth more than the sum of its parts. The latest fad, GenAI, fits within this collection. According to Fujitsu leaders, the company has delivered over 7,000 AI-enhanced solutions, providing a strong foundation to tap into as GenAI is more widely adopted. TBR recognizes the Japan-centric nature of the majority of Fujitsu’s AI uses cases but sees the value in playing to the company’s strengths.

Among these strengths, Fujitsu’s leaders noted that the company’s superpower (TBR’s word, not theirs) comes from fusing compute power with AI. One of the guest speakers reinforced that sentiment by noting that GenAI is feasible only because of the extreme computational power utilized. Fujitsu has recognized that being good at compute is absolutely necessary to be good at GenAI.

In TBR’s view, this potentially unique combination of compute power and AI, at scale, could separate Fujitsu from peers as enterprises begin the slow process of recovering from the unfulfilled promises of GenAI hype and implementing the changes needed to progress from pilot to scaled deployments. Fujitsu’s leaders explained that their strategy to accelerate that progress started with the launch of a free AI platform, dubbed Fujitsu Kozuchi (“magic hammer” translated from Japanese), essentially a GenAI sandbox, which the company has now begun to commercialize through a freemium business model.

Critically, Fujitsu has tracked activity within the sandbox to determine which AI use cases and associated technologies gained the most client traction and have significant revenue upsides for the company. Fujitsu has been transitioning these uses cases, smartly, from free to use to pay for scale. Fujitsu’s Kozuchi platform spans seven AI areas: GenAI, Predictive Analytics, for Text, AI Trust, XAI, for Vision, and AutoML.

In TBR’s view, Fujitsu’s experimentation with AI commercial models while marrying inherent compute power to the potential of GenAI only works because of Fujitsu’s extensive experience with AI and credibility with clients and ecosystem partners. Fujitsu needed a solid foundation in both compute and AI to be well positioned for accelerated growth around GenAI.

Additionally, Fujitsu’s broad-based portfolio, including its family of HPCs (high- performance computers) as well as the lower power consumption Fujitsu ARM-based processor — the latest version is scheduled to be released in 2027 — can help the company compete for managing AI workloads, specifically machine learning ones. With security built into the hardware, these processors can also help Fujitsu better appeal to clients in highly regulated industries, including the public sector, emergency response and public safety, healthcare and telco, among others. While built-in security is not a unique feature to Fujitsu, it is a necessary building block as it enables the creation of a strong tech-led AI story around developing and managing large language models.

Exactly the Right Time to be Strong in Analytics and AI

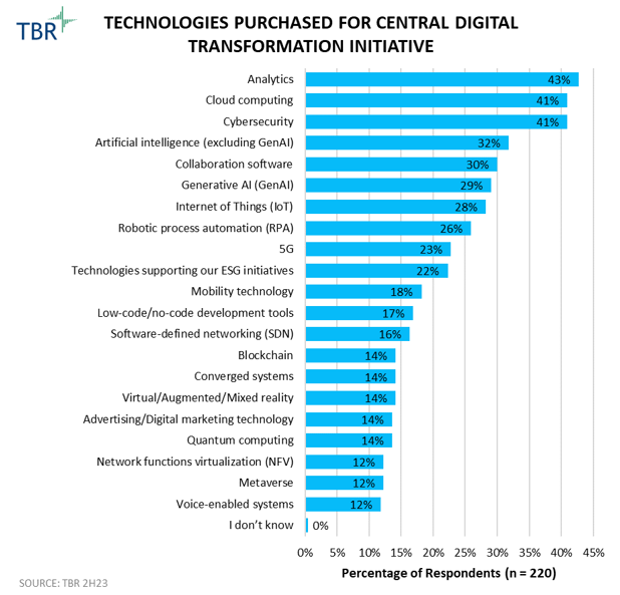

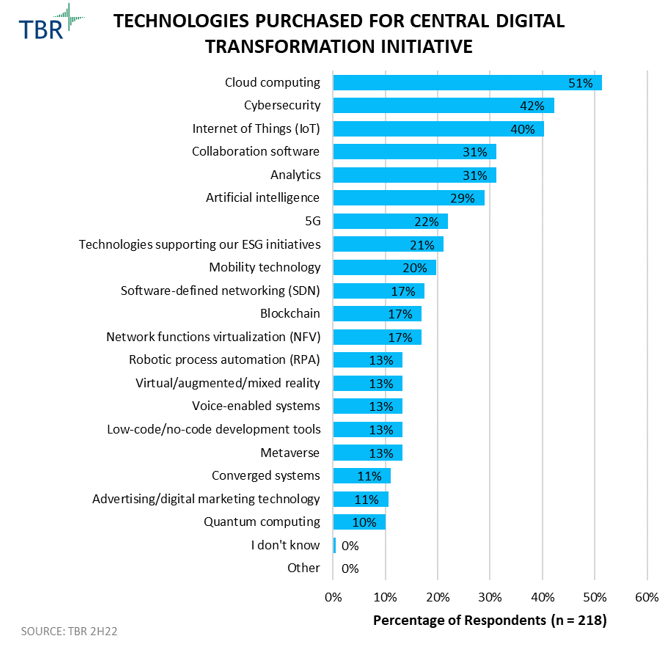

TBR’s Voice of the Customer research shows an additional component to Fujitsu’s potential GenAI-related growth. In TBR’s December 2023 Digital Transformation: Voice of the Customer Research, analytics topped the list for priority investments in technologies supporting transformation, displacing cloud and cybersecurity for the first time since TBR started tracking the data six years ago.

The report notes: “Analytics is now the top technology buyers choose to support their DT [digital transformation] programs, with AI tools and GenAI ranking in the top six, thus heightening buyers’ expectations for vendors to deliver timely ROI that is tied to ongoing business process and/or IT modernization transformation as implications of technology complexities extend beyond data science, thus creating opportunities for vendors that can manage broad-organizational relationships. Addressing multidisciplinary skills gaps will be key.”

Sustainability and Innovation

Fujitsu’s presence and history in the Silicon Valley, which spans 30 years, enabled the company to develop a deep innovation ecosystem. Fujitsu’s CEO of Research of America, Indradeep Ghosh, and Global CTO, Vivek Mahajan, discussed the expansion of the company’s innovation efforts and how Fujitsu has shifted toward sustainability impacts. At the company’s recently opened facility, Fujitsu remains in close proximity to its key partners, including technology vendors as well as smaller, more specialized firms, which can drive collaboration and innovation efforts.

Further, Fujitsu is able to work with universities including Carnegie Mellon University and the nearby Stanford University to deepen its AI, analytics, data utilization and digital twin expertise. Through its innovation efforts, Fujitsu looks to drive social change and leave a positive impact on society, in addition to gathering business intelligence.

To contribute to societal change, Fujitsu is prioritizing sustainability with a focus on slowing the impacts of climate change. Fujitsu leverages its expertise and insights to develop technologies and services that benefit the environment and society. Developing sustainability services and solutions in collaboration with U.S.-based universities and companies could encourage local enterprises to establish carbon and energy reduction goals.

While sustainability and carbon reduction initiatives have stronger traction in Europe, Fujitsu’s efforts will help transform local clients’ global operations. Fujitsu is considering the long-term impact, which will create new opportunities for the company to drive digital transformation projects across regions outside Japan.

Quantum

Quantum technologies have long been ingrained in Fujitsu’s portfolio and technologies, starting with its in-house development of computing and high-performance computing in the 1990s. Fujitsu has continued to expand the compute power of its quantum technologies enabling the company to address a wider range of challenges, with societal issues the most recent addition. Building out its base and capabilities, in addition to establishing itself as a global technology company, have helped Fujitsu explore the U.S. market. Fujitsu is pursuing two strategies around quantum that will give the company an edge over its technology-centric peers.

First, as CTO Mahajan noted during the event, “We [at Fujitsu] are very willing to transfer our IP.” The willingness to give away IP expands Fujitsu’s addressable market. This openness to IP adoption provides both Fujitsu and prospective customers with an advantage, as it raises awareness of the company’s platform and ability to expertly deliver, implement and manage quantum technology.

Second, Fujitsu’s plans include the capability to build a quantum computer at a client’s site, actually bringing the hardware to a client rather than providing quantum services from a Fujitsu site. By creating on-site hardware stacks, Fujitsu will be able to integrate with clients’ existing or preferred technologies, enabling the use of new capabilities. With the ongoing convergence of technologies, the ability to work across and with a variety of platforms will strengthen Fujitsu’s overall positioning within the space.

GenAI

Despite possessing the GenAI superpower of fusing the company’s compute power with its AI expertise, Fujitsu has, by its leaders’ own admissions, struggled to gain market recognition as a top player in the overall AI space. One approach Fujitsu has begun pursuing focuses on influencing the wealth of AI startups. TBR’s casual observance of the many startup-affiliated name tags at the ActivateNow event indicated this approach may have generated some early traction.

In TBR’s view, focusing on startups reinforces Fujitsu’s corporate culture and mindset, which view technology as central to everything Fujitsu does. The company’s leaders also stressed their efforts to leverage academic research and the broader technology ecosystem as a way to echo Fujitsu’s message of “converging technologies,” a concept that TBR believes hews closely to emerging trends (see TBR’s 2024 Professional Services Predictions and 2024 Digital Transformation Predictions).

Applying the company’s blockchain technology to its AI and GenAI assets could strengthen Fujitsu’s position in the space and grow its recognition outside of Japan. The need to regulate AI continues to expand with emerging use cases. Fujitsu’s expertise around blockchain, including Fujitsu Data & Security Technologies for Sustainability Transformation, aligns closely with data protection and regulation, creating the opportunity for the company to apply these capabilities to AI. Fujitsu’s blockchain solutions add a layer of identity and protection to verify real data and information, protecting against external threats.

Sustainability and Consulting as Critical Next Frontiers for Fujitsu

Notably, Mahajan’s first topic was global warming — as he stated, “boiling” — and the opportunity to apply technology to solve climate challenges. His comments conformed with Fujitsu leadership’s sustained message around competing globally and providing something valuable to clients, but TBR cannot recall a similar situation in which the global CTO of a technology-centric company led with global climate change.

For the rest of 2024, TBR will listen for similar emphases from CTOs and other C-Suite leaders at the start of technology events. Meanwhile, Fujitsu Uvance provides Fujitsu with resources to develop and deepen the company’s expertise within vertical markets as well as horizontal business areas, allowing the company to drive transformation projects further enhanced by ESG (environmental, social and governance) initiatives.

More specifically, Fujitsu can narrow its scope within markets as clients diverge and look to embrace sustainable solutions and achieve outcomes. Leading with the Fujitsu Uvance brand allows Fujitsu to integrate sustainable solutions within specific vertical markets including sustainable manufacturing.

Lastly, with increasing client concerns around trusted partners and technology, Fujitsu Uvance’s AI Ethics and Governance Office can help the company establish digital trust in digital transformation projects and help secure Fujitsu’s relationships. Focusing on trust and ethics for the use of AI technologies will allow Fujitsu to use AI more effectively both internally and with clients.

Amalgamation of AIs and Connected Technologies Help Tell Fujitsu’s AI Story

TBR came away from the Fujitsu ActivateNow Technology Summit with two new ideas about Fujitsu and a few questions:

- First, TBR appreciates that Fujitsu’s combination of compute power and proven AI expertise makes the company a significant competitor and/or alliance partner for nearly every player fighting to turn GenAI hype into revenue. Second, Fujitsu’s vision of “converging technologies” aligns exceptionally well with the more tectonic trends TBR has been observing in the technology space, indicating that Fujitsu’s market positioning is more strategic than transactional or opportunistic.

- Going forward, will Fujitsu be able to leverage AI startups to shift enterprise buyers’ perceptions about Fujitsu as an AI company? Can Fujitsu successfully bring Japan-centric AI use cases to clients in Europe and North America? And will Fujitsu develop an alliance strategy that plays to its strengths in compute power and emerging technologies while leveraging ecosystem partners’ strengths in other critical component areas for enterprise buyers?

TBR anticipates that Fujitsu’s concept around the amalgamation of AI solutions will become a widely shared approach to GenAI. As the hype slows down in 2024 and buyers look to trusted vendors with both scale and proven use cases, as well as the ability to connect existing technologies — especially existing AI-enabled solutions — to GenAI deployments, many of Fujitsu’s peers and alliance partners will be talking about a broader understanding and framing of AI within the enterprise.

TBR covers Fujitsu in quarterly reports and as one of 30-plus vendors in TBR’s quarterly IT Services Vendor Benchmark. In addition to this event perspective, TBR has published numerous special reports on Fujitsu events and developments over the last decade.

Nothing Found

Sorry, no posts matched your criteria