In 2023 we wrote: “Automation will lower costs and AI will transform businesses.” A year later, this trend is even more pronounced, largely accelerated by the advent of generative AI (GenAI).

GenAI is new and exciting, but buyers’ realities and priorities did not change just because GenAI came along, which will force vendors to cite tangible use cases that minimize disruption and maximize ROI.

We did not see GenAI disrupting the technology and services market to the extent it did in 2023, and we do not recall a single conversation with vendors and enterprise buyers prior to November 2022 in which the term GenAI was even mentioned. However, the increase in macroeconomic headwinds is forcing market participants to rethink how to best position their portfolios, go-to-market strategies and commercial models.

Watch 2024 Digital Transformation Predictions session: Navigating GenAI in Digital Transformation in 2024

2024 GenAI Outlook for Enterprise Buyers

The GenAI hype has raised buyers’ expectations that the implications of the technology have become more clear, increasing pressure on technology and services vendors to deliver value — starting with use cases and rapidly pivoting toward outcomes.

Of course, for any of these aspirations to happen at scale, one must take a closer look at how well prepared enterprise buyers are in their data architectures, IT stacks and, most importantly, their people. Buyers are somewhat conditioned that their third-party services and technology providers will constantly try to nudge them and introduce new technologies. The current environment is no different, but what makes GenAI more special is the hype that GenAI can optimize costs while driving new growth areas.

However, simply adding GenAI to IT modernization and/or cloud migration projects does not serve everyone well and really just prepares them for the long play. And it is certainly a long play, especially as less than 10% of global enterprises have a defined data strategy, according to industry reports.

But vendors must act now, as discretionary spending has stalled and enterprise buyers are spending only on projects that have greater organizational impact — if at all — rather than testing new frameworks or experimenting with proof-of-concept innovation-wrapped discussions. So, the most immediate opportunity for GenAI to make an impact is for vendors developing function- and/or department-specific models.

Developing large language models (LLMs) is not cheap, and organizational data typically lives in silos — departmental or functional. We see vendors starting to dabble with the idea of introducing “narrow” language models that are built off the same departmental data that for decades vendors and enterprises have aspired to make interoperable. It is possible that GenAI could force enterprises to raise their organizational walls even taller, which would necessitate different commercial and partner models.

Conclusion

Vendors must act now. Establishing more defined use cases around function- and/or department-aligned data will pave the way for the technology as vendors seek to scale adoption across industries. Even if adoption cannot be scaled in the near term, being entrenched early in a client’s GenAI journey should lead to long-tail revenue.

https://tbri.com/wp-content/uploads/2024/01/AI-in-Digital-Transformation.png10801080Bozhidar Hristov, Principal Analysthttps://tbri.com/wp-content/uploads/2021/09/TBR-Insight-Center-Logo.pngBozhidar Hristov, Principal Analyst2024-02-13 16:29:302024-02-13 18:26:39GenAI Expectations for Enterprise Buyers in 2024

An uncertain macroeconomic outlook has continued to pressure discretionary spending and consulting activities while fueling a wave of outsourcing demand around infrastructure and application modernization, productivity improvement and cost optimization.

Maintaining trust with stakeholders through transparent messaging will be key to competing in this market landscape, especially as managed services bookings take longer to convert into cash compared to consulting engagements. Multiple vendors are developing generative AI (GenAI) offerings for clients as well as using them internally. While GenAI provides a strong use case around improving productivity, it can also challenge vendors’ managed services businesses if the technology is not properly priced after accounting for the impact on staffing models.

Join Principal Analyst Patrick M. Heffernan and Senior Analyst Elitsa Bakalova Thursday, March 7, 2024, for an exclusive review of the latest insights and analysis in TBR’s IT Services Vendor Benchmark, which looks at the competitive landscape as well as the performances of 31 leading IT services providers. Don’t miss this opportunity to learn the strategies vendors are leveraging to succeed in the challenging market environment.

In This FREE TBR Insights Live Session on GenAI in IT Services in 2024 You’ll Learn:

The drivers behind IT services vendors’ positive performance

Vendors’ performance in the financial services industry and in the Americas geography

TBR’s expectations for IT services in 2024

TBR webinars are held typically on Thursdays at 1 p.m. ET and include a 15-minute Q&A session following the main presentation. Previous webinars can be viewed anytime on TBR’s Webinar Portal. For additional information or to arrange a briefing with our analysts, please contact TBR at [email protected].

https://tbri.com/wp-content/uploads/2024/02/WI_ITServicesBM_1Q24_Square.png10801080TBRhttps://tbri.com/wp-content/uploads/2021/09/TBR-Insight-Center-Logo.pngTBR2024-02-07 14:45:312024-03-18 13:09:49From Transformation to Optimization: GenAI Hype vs. IT Services Reality

As part of the Big Four, KPMG has brand permission and a breadth of services relevant to nearly every role in any enterprise. TBR believes KPMG will accelerate the scale and completeness of its offerings in the coming year, building on a solid foundation and furthering the gaps between KPMG and other consulting-led, technology-enabled professional services providers.

KPMG’s four-part framework — Connected, Powered, Trusted and Elevated — resonates with clients and technology partners, provides KPMG’s professionals with clear insight into the firm’s strengths and strategy, and underpins a transformation already well underway. The coming year will challenge KPMG’s leaders to execute on the promise of that transformation during the next wave of macroeconomic pressures, talent management battles and technology revolutions.

KPMG’s leaders described their priorities as transforming the firm’s go-to-market approach, unlocking the power of the firm’s people, reimagining ways of working, and innovating capabilities and service enhancements. Success against these priorities, in TBR’s view, will come as KPMG shifts from building a foundation to scaling alongside the growing needs of its clients.

Welcome (or Welcome Back) to Lakehouse

Breaking from the traditional form for analyst events — presentations followed by special sessions and one-on-one meetings — KPMG divided the attending analysts into three groups, rotating each group through Ignition, KPMG’s immersive innovation lab experience; presentations and demos in an Innovation Showcase; and a tour of Lakehouse. A few highlights:

In addition to walking the analysts through the typical 10-minute start of an Ignition session, recreating what KPMG’s clients experience, the firm gave the stage to a client, who shared their experiences working with KPMG. The consulting and technology solutions provided by KPMG served as useful context for the breadth of KPMG’s capabilities and the importance of using an innovation center. Most notably, the client described how their own brand depended on being a trusted partner in the communities they served and how their relationship with KPMG reinforced that trust across the full spectrum of the consultancy, the client and the client’s clients. TBR came away with a better appreciation for KPMG’s ability to extend trust and partner across its offerings and engagements.

KPMG’s technology presentations included a wide range of solutions leveraging an array of emerging technologies such as quantum and generative AI (GenAI). Taking more than the allotted hour with TBR, the KPMG team walked through a surprising number of offerings, repeatedly coming back to two critical points: These are currently active solutions, deployed with clients and moving toward scale (i.e., not ideas undergoing testing or in beta), and KPMG boasts a breadth of technology capabilities that TBR realized was far greater than our expectations prior to the event.

KPMG has continued to apply lessons around training and talent management to maximize the firm’s culture effects delivered by Lakehouse. As shared by KPMG’s leaders, small changes since Lakehouse opened have kept the employee experience fresh and the overall satisfaction with attending training or other kinds of sessions at Lakehouse exceptionally high. For example, KPMG learned that two and a half days of in-person sessions reduced the stress of being away from clients or engagements for a full week. By layering Monday to Wednesday and Wednesday to Friday training schedules, KPMG can bring more employees through Lakehouse without inducing training burnout or challenging employees to balance client demands with professional development time. In an informal discussion, an event guest (neither an analyst nor a KPMG employee) commented to TBR that she was amazed to see a facility that was designed for and dedicated to training.

KPMG’s decision to ease into an analyst event with small groups wandering around Lakehouse played to the firm’s strengths as approachable and multifaceted, with each of the three sessions quietly reinforcing the firm’s commitments to maintaining trust with clients, advancing technology-enabled solutions to business problems, and supporting the firm’s own people through professional development and firm culture.

While the firm is already leveraging the facility globally, one challenge for KPMG next year and beyond will be replicating Lakehouse globally. During a coffee chat shortly after the analyst event in Orlando, TBR and a senior KPMG consulting partner discussed how, whether and when the firm could open similar best-in-class training facilities in key geographies, such as Europe, the Middle East and Asia Pacific.

While Lakehouse requires a significant investment from KPMG’s legally separate member firms, TBR — and KPMG leaders who discussed the possibilities — has already seen Lakehouse expand from a training-only facility to a showcase for clients, reinforcing KPMG’s culture and the firm’s place in the professional services market.

Stick to the Mission and Tackle the Biggest Problems

Across the full day of presentations, KPMG repeatedly came back to highlighting its efforts to bring together the entire firm to deliver value to clients through a four-part framework: Connected, Powered, Trusted and Elevate. That value, according to KPMG’s leadership, began with trusted relationships with its clients, built when clients developed their business strategies and turned to KPMG for advice and validation.

Notably, according to KPMG’s leadership, pure technology companies often lack the strategy consulting permission (or people) as an enterprise begins a transformation, even if implementing new or modernizing existing technology will play a leading role. And when the technology is delivering business results, KPMG has the trusted advisor role and the skills to refresh an enterprise’s strategy.

Bringing this high-level view — which is not that different from what the other Big Four firms offer — to a more concrete understanding of KPMG’s value to its clients, TBR repeatedly heard two phrases during the Lakehouse event: “Let’s go after the core of the biggest problems you have” and “Stick to our mission.”

The first phrase demonstrates a willingness to take risks and tackle hard issues, not simply assist with marginal, if necessary, changes. In contrast, many of KPMG’s IT services competitors that are equally willing to help clients move from technology transformation pilots to enterprise-scale deployments still prioritize transactional engagements with a reduced risk mindset. (Note: TBR believes GenAI will strip 15% of the cost from current large-scale managed services contracts, a potentially existential threat to a few global systems integrators [SIs].)

The second phrase signals to TBR that KPMG’s leadership fully embraces the firm’s role within the larger services and technology ecosystem, to include where and when the firm needs to partner with technology vendors and even larger SIs. In a market flush with technology hype — GenAI today, metaverse in 2021, blockchain in 2019 — KPMG has resisted the temptation to chase technology discussions with technologists for technology’s sake and instead has focused on business decision makers looking for advice, a strategy and an execution plan. Stick to the mission. Go after the biggest problems.

Who Has the Money and Time to Build Their Own Bridge?

In a wide-ranging presentation and discussion around data, KPMG leaders acknowledged that every professional services firm emphasizes rigorous, standardized and methodical analysis of its clients’ data (when they can get it and its useful; see TBR’s Voice of the Customer research for how often that is the case).

To separate itself, KPMG leaders said the firm leans into experience, applicable industry knowledge, a dedication to methodology, and extracting value from existing assets. In TBR’s view, this last point illustrates a critical shift in enterprise buyers’ priorities that KPMG has picked up on and has begun to leverage.

In TBR’s view — and apparently KPMG’s as well — consulting and digital transformation clients want to move beyond the endless rounds of buying new technology solutions and reorient to extracting value from existing assets. To span that gap from existing data to modernized technology and transformed business, enterprises still need a bridge. KPMG has the blueprints and the experience in building those bridges, helping clients elevate and transform.

Solidifying Alliances Through Trust, Culture and Shared Values

Pivoting to alliances with technology partners, KPMG’s leaders spent a significant portion of the analyst event describing how the firm works with Google Cloud (Nasdaq: GOOG), IBM (NYSE: IBM), Oracle (NYSE: ORCL), Microsoft (Nasdaq: MSFT), ServiceNow (NYSE: NOW), Salesforce (NYSE: CRM), SAP (NYSE: SAP), Workday (Nasdaq: WDAY), and Verizon (NYSE: VZ). We cover SAP and Verizon in detail below, but a few elements came across as essential to how KPMG sees its role in the larger technology ecosystem:

Technology partners look to KPMG for industry experience and access to buying personas at clients that technology partners simply do not have (think: CFO).

Technology partners expect KPMG to share values, align culturally and invest in sustained relationships at multiple levels within each partner.

The first set of expectations technology partners have for KPMG do not significantly differ, if at all, from similar expectations of the other Big Four firms. The second set, in TBR’s view, demonstrates KPMG’s more focused and selective approach to alliances. Technology partners only expect cultural alignment and shared values if both parties make that a core element of the alliance.

Given the nature of other technology-plus-consultancy alliances TBR has analyzed in detail, KPMG is likely driving the emphasis around cultural fit and shared values, an effort that cannot be replicated across tens or even hundreds of alliance relationships. As will be reinforced by the following sections on SAP and Verizon, TBR sees KPMG’s alliance strategy as well suited to how the firm has built its brand around trust. As the firm continues to scale to meet clients’ needs, maintaining that emphasis on trust, culture and shared values will challenge KPMG and require careful management across the global member firms.

One final comment: One of the leaders from one of KPMG’s technology partners began their discussion by stating, “The candor and brutal honesty that they brought to the assessment reinforced KPMG’s reputation.” It is hard to imagine an endorsement more rooted in trust and shared values.

KPMG and SAP: Growing Exceptionally Fast, with Plenty of White Space Ahead

For more than a decade, KPMG’s audit relationship with SAP precluded the firm from going to market jointly with SAP and constricted KPMG’s potential relationship with the ERP giant. Unrestrained now, KPMG has the opportunity to step smartly into a competitive field currently overcrowded with services vendors looking to ride the wave of enterprises migrating to SAP S/4HANA. Separating KPMG from this pack, which includes its Big Four peers and global SI (GSI) giants like Accenture (NYSE: ACN) and Capgemini, requires executing on three key elements, in TBR’s view.

First, KPMG needs to ensure SAP’s leadership, sales teams and especially SAP S/4HANA subject matter experts understand the scale and capabilities KPMG already has and where the firm is investing — in SAP — in the near term. Convincing SAP that KPMG will bring value beyond just another consultancy or SI to SAP’s clients will help KPMG expand its small SAP footprint within existing clients.

Second, KPMG will need to continue investing in its SAP practice to ensure credible scale in a crowded marketplace in the long term. KPMG is not starting from zero, and with success in the SAP marketplace requiring integrated cloud, security and business capabilities, KPMG will have to ensure continued tight collaboration among all of these adjacent areas and the 5,000 SAP consultants it already has on its books.

Finally, with industry and domain expertise critical to successful SAP-led business transformation KPMG’s Powered Enterprise approach will be key to customer success. Aligning functional and domain expertise across SAP’s Business Technology Platform (BTP) with industry understanding will be critical to driving client value in areas like environmental, social and governance (ESG) and AI. Clients are increasingly seeking outcomes through technology investment, and the KPMG Powered approach aligns the KPMG Target Operating Model, Powered Technology and Powered Industry excellence as well as its suite of deployable assets to drive outcomes with business value.

KPMG and Verizon: Vendor Agnostic No More

If SAP is KPMG’s up-and-coming alliance, what KPMG has developed with Verizon truly distinguishes the firm from the rest of the market. In essence, KPMG and the networking giant evolved their relationship from a history of transformational engagements into what KPMG leaders describe as a collaborative “360-degree relationship” based on a foundation of trust. KPMG brings deep business intelligence and systems integration capabilities, combined with strong industry experience, going to market with Verizon and their disruptive 5G/Mobile Edge Computing technology. In addition, KPMG continues to deliver transformative work, often leveraging other key alliance partners such as ServiceNow.

Focusing initial joint go-to-market efforts around opportunities in healthcare, KPMG and Verizon have staked out complementary offerings and responsibilities. For example, as KPMG highlighted during the event, the firm “brings advanced data science and analytics capabilities through KPMG Lighthouse,” while Verizon provides “advanced multi-access edge computing and API management capabilities.” KPMG also emphasized that, specific to healthcare, the firm has launched an Innovation Lab supported by Verizon’s “private 5G infrastructure as backbone.”

Describing the array of KPMG and Verizon services, KPMG leaders noted the many offerings, such as Cloud Engineering, Platform Design & Engineering and Digital Twin, Device Simulation & Certification, that KPMG and Verizon will deliver through a joint approach, combining KPMG and Verizon professionals. In TBR’s view, this alliance stands apart from other consultancy technology alliances because of the innovation, development, go-to-market and commercialization commitments.

This is not a vendor-agnostic approach. This is picking a 5G, networking and edge provider and going all-in. Based on the presentations onstage and sidebar discussions, this all-in commitment goes both ways, with Verizon clearly seeing the value of partnering as closely as possible with KPMG.

Bringing the Right People Together and Always Making a Difference

During the afternoon sessions, TBR heard multiple client use cases, each one reinforcing KPMG’s core messages around trust, transformation, innovation and value. Three moments stood out as exemplifying precisely what makes KPMG the market-leading firm it is today:

During a discussion on cybersecurity, KPMG’s leaders noted that the firm brings security experts, industry subject matter experts and even tax professionals to Ignition Center engagements, stressing that this approach — which includes the whole KPMG team — serves multiple purposes. First, the client can appreciate the full range of KPMG’s capabilities and offerings. Second, this approach allows the client (in this case, the chief information security officer [CISO]) to see the business from others’ perspectives. Third, KPMG creates a collective, trusted, collaborative environment, focused on both innovation and core business problems.

In a presentation by KPMG, one of its clients and one of its technology partners (Oracle), the client said one key criterion in selecting KPMG was the firm’s credibility in always being able to deliver the right people at the right time who understand the right technology. Trusted relationships depend on dependability and consistent delivery. This client case proved KPMG’s commitment and reinforced that KPMG has been building needed scale.

Lastly, dinner at Lakehouse included a panel discussion featuring LPGA’s Commissioner Mollie Marcoux Samaan, and the assistant U.S. team captain, golf pro Angela Stanford, both arriving directly from the 2023 Solheim Cup in Spain, where the U.S. had its best ever score on European soil. According to the LPGA guests, KPMG provided analytics-enabled insights and on-site support to help the U.S. team pick the right pairings over the course of the tournament, bringing data and additional rigor to intensely personal and often challenging decisions. As a use case, few of KPMG’s enterprise clients will need the firm’s help pairing golfers to win a tournament, but every client will likely lean on KPMG for assistance with data-driven decisions.

At the start of 2024, KPMG has positioned itself well to sustain its core values, bring transformation to clients and continue to scale. Now comes the execution of that strategy.

Note: KPMG also shared specific details about its alliances with ServiceNow, Salesforce, Workday, Microsoft and Oracle. These details will be included in TBR’s ongoing coverage of KPMG and in upcoming ecosystem reports.

https://tbri.com/wp-content/uploads/2024/02/clint-adair-BW0vK-FA3eg-unsplash.jpg12801920TBRhttps://tbri.com/wp-content/uploads/2021/09/TBR-Insight-Center-Logo.pngTBR2024-02-05 16:39:392024-02-12 14:07:58KPMG Leaders Talk 2024 Priorities and Plans to Scale Execution

Vendors capable of playing nice in the GenAI sandbox and backing up their GenAI stories and promises with delivered results for clients will outpace peers in 2024. Vendors missing any of those components will still be able to benefit from the GenAI gold rush, but they will experience poorer results and diminishing relevance in the market. Download your free copy of TBR’s AI & GenAI Spotlight Report to read more on TBR’s GenAI market research.

What is GenAI?

Generative AI (GenAI) is a type of AI that allows users to create completely unique items, including text, images, video and audio, from written requests. The most critical difference between commonly used AI tools and GenAI is simply the difference between answering a question using available information verse creating a unique answer. AI is asking Alexa who won the Boston Celtics game last night. GenAI is asking Alexa to write a text to a friend to tell him he should have bet on the Celtics for last night’s game.

At TBR we’re continually examining the business models and financial, resource and go-to-market strategies of companies in the technology ecosystem, so we’re often looking beyond the marketing hype to the delivered value and financial results. The use of the word “stories” rather than “strategies” when it comes to GenAI highlights the critical need for use cases for this new technology. In the case of GenAI, what clearly mattered in 2023 and will continue to matter in 2024 is not nuanced strategic decisions or even fine-tuned market positioning but the need to tell a good story.

Top GenAI Uses Cases

Relentless GenAI hype has carried in its wake both credible examples of the technology deployed in pilot projects and wild speculation about use cases that could be scaled once the analytics, compute power, and change management approaches are acquired and aligned.

It is still too early to catalog credible, deployed-at-scale use cases or speculate on which vendors across the entire IT ecosystem have taken any kind of use case lead. Anticipating that kind of analysis in mid-to-late 2024, TBR instead has followed the leads provided by enterprise GenAI buyers who have noted that use cases have mostly been presented in tiers:

Short term: Productivity improvements. Notably, these use cases can most credibly and quickly be attested to by IT services vendors and consultancies applying GenAI solutions to their own operations.

Midterm: Standard enterprise applications, such as CRM, ERP, HCM and SCM. For these, while the IT services vendors and consultancies may play the role of data and ecosystem orchestrators, the heavy lifting will come from the software and cloud vendors, provided, of course, the infrastructure can support GenAI compute and storage needs.

Long term: As one PwC leader put it, “You’re talking to your business, and it talks back.”

What Makes GenAI Different From Other Next-generation Technology?

How is GenAI technology, especially the popularized applications exemplified by ChatGPT, unique? Well, exactly that popularization, for starters. Enterprise technology buyers and employees influencing technology decision making don’t cower at technical complications; rather, these personas are enthused — possibly terrified, but that’s a short-term phenomenon — by what GenAI can do for them. Plus, most people respond to a story, not a strategy.

A good story around deploying GenAI will stand out in an overhyped market. In the countless discussions around GenAI that TBR has had with clients in the last 13 months, we’ve frequently been asked about use cases, which are, essentially, stories about a company finding a way to use this new magic. Without these use cases, there are no stories around GenAI and, therefore, no excitement. Use cases will remain necessary to GenAI strategy in 2024, but “playing nice in the GenAI sandbox” will increasingly become the clearest marker of a successful GenAI strategy.

While GenAI became the tech world’s darling in 2023, a pivot to ecosystems dominated how TBR began thinking about the changing technology market landscape. At the request of clients and built on decades of deep research around individual vendors, we launched dedicated analysis of how companies we cover interact, including interdependencies, revenues realized, and alignment challenges.

Among the constant themes: Companies that partner well outperform peers. The traditional boast of “end-to-end” makes no sense in today’s technology environment, particularly when one considers the implications of wider GenAI adoption, including challenges around talent, compute power, and compliance. “Playing nice in the GenAI sandbox” will be the difference between making money from GenAI and making a business out of GenAI.

Learn More About the GenAI Landscape

At TBR we’re covering GenAI from nearly every market angle. We publish a wide-ranging view of the GenAI sandbox, from management consultancies to cloud vendors and infrastructure providers to device and chip manufacturers.

Our analysis on how companies will interact around GenAI and, critically, what these companies will look for in alliance partners is just the tip of the iceberg for TBR’s research on the technology. Our recently published new research stream, AI & GenAI Market Landscape, covers GenAI from the perspective of TBR’s Telecom, Devices, Cloud, Infrastructure, IT Services and Consulting experts. Additional market-specific AI research will publish later in the year.

https://tbri.com/wp-content/uploads/2024/01/AI-GenAI-Promo-Image_Square.png10801080Patrick Heffernan, Practice Manager and Principal Analysthttps://tbri.com/wp-content/uploads/2021/09/TBR-Insight-Center-Logo.pngPatrick Heffernan, Practice Manager and Principal Analyst2024-01-26 15:51:552024-02-13 18:24:14GenAI and the Power of the Use Case

Up to a 75% reduction in time to introduce new services

Up to a 99% reduction in time to upgrade or update existing services

Average total cost of ownership reduction of 10% to 30%

The above are just a few examples of the real-world business outcomes leading service providers are realizing from their IT modernization projects. These outcomes are critical to ensure service providers can adapt and stay competitive in their respective markets as well as grow revenue.

AI, automation, containers, cybersecurity, hybrid cloud, machine learning and virtualization are all examples of the types of technologies service providers are incorporating into their IT modernization initiatives to yield these cost-efficient, flexible and agile outcomes. AI (especially generative AI) is of particular interest of late following technological breakthroughs from OpenAI’s ChatGPT platform, which has demonstrated that generative AI has developed to a point that it is able to bring useful outcomes to businesses and consumers alike.

Generative AI holds tremendous promise for service providers to further improve business outcomes, primarily thanks to the advanced automation the technology can enable. Though generative AI technology is still nascent, it is likely to be incorporated across service providers’ IT estates, from call centers to cybersecurity to billing systems, bringing cost savings, time savings and resource savings.

The outcomes derived from IT modernization become even more important for service providers as they prioritize fiscal responsibility. With high interest rates and a weakening macroeconomic outlook, service providers need to increase their focus on cost efficiencies. Rather than scale back IT modernization initiatives amid fiscal constraints, service providers should double down on these projects because they can help achieve corporate financial objectives.

IT modernization should be thought of as an iterative journey, starting small and expanding the scope over time. Leading service providers that have significant experience with this journey advise that focused prioritization — a step-by-step, iterative approach that tends to require limited upfront financial commitment and ties up fewer resources — is the best approach because the benefits can be rolled into (built upon) next steps in the journey. This contrasts with a boil-the-ocean approach, which typically encompasses a pan-IT estate lift and shift. This approach tends to be risky and expensive and rarely yields the desired results. Another important factor to yield desired outcomes is to ensure the business is aligned with the IT department on every modernization initiative, because when these stakeholders are not in sync, the desired objectives and outcomes are often not realized.

For a closer look at how the key technologies and processes come together to drive telecommunications IT modernization outcomes (AI, machine learning, automation, hybrid cloud, containerization, cybersecurity and more), download “Adapt, compete and grow: A guide to modernizing telco and cable IT.”

To watch a webinar on this topic, “Telecommunications and cable service providers: Modernize IT to adapt, compete and grow,” click here.

https://tbri.com/wp-content/uploads/2024/01/towfiqu-barbhuiya-joqWSI9u_XM-unsplash-scaled.jpg17082560Chris Antlitz, Principal Analysthttps://tbri.com/wp-content/uploads/2021/09/TBR-Insight-Center-Logo.pngChris Antlitz, Principal Analyst2024-01-19 16:55:122024-01-19 16:55:12Service Providers: IT Modernization Isn’t Flashy, but It Leads to Tangible Savings. Here’s How …

Update: For the latest developments in the U.S. federal IT market, check out our December 2024 blog Federal IT Spending Will Remain Robust in FFY25 Amid AI Prioritization, which highlights the proposed budget for FFY25 and its potential impact on federal systems integrators. Click here to read the full blog.

Current State of the Federal IT Services Market

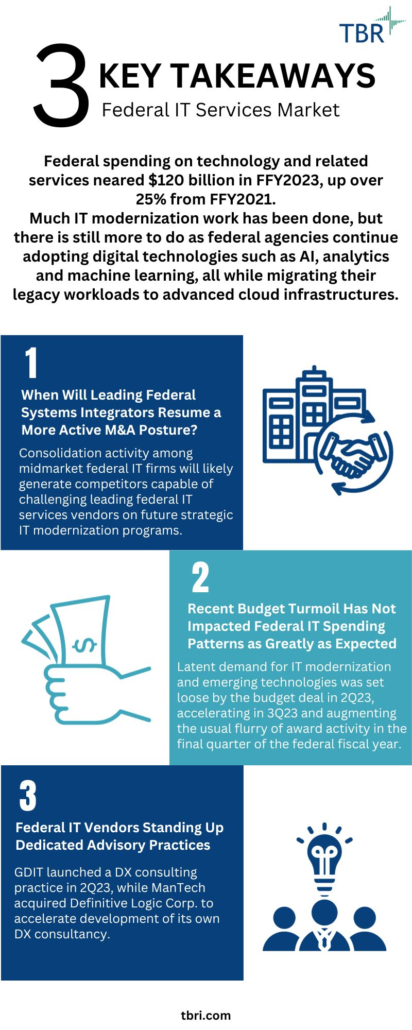

The most intensive bull market in federal IT spending continues, and the federal IT services market will remain robust through federal fiscal year 2024 (FFY2024). Much IT modernization work has been done, but there is still more to do as federal agencies continue adopting digital technologies such as AI, analytics and machine learning, all while migrating their legacy workloads to advanced cloud infrastructures. Federal spending on technology and related services neared $120 billion in FFY2023, up over 25% from FFY2021 and on a trajectory to surpass $130 billion by FFY2025.

The below infographic contains the three key takeaways from TBR’s latest research on the U.S. federal IT services market and what these events mean for you.

Top 3 Takeaways for 2024

When Will Leading Federal Systems Integrators Resume a More Active M&A Posture?

Consolidation activity among midmarket federal IT firms remains very robust and will likely generate competitors with the scale and the depth of digital capabilities to challenge the leading federal IT services vendors on future strategic IT modernization programs.

Recent Budget Turmoil Has Not Impacted Federal IT Spending Patterns as Greatly as Expected

Overall growth in the federal IT sector in 3Q23 was the most aggressive TBR has observed since launching its coverage of the market in 2008. The debt ceiling agreement in June 2023 provided a much-needed respite for the federal IT market from the budget turmoil that had impeded growth through FFY2022 and early FFY2023. Latent demand for IT modernization and emerging technologies was set loose by the budget deal in 2Q23, accelerating in 3Q23 and augmenting the usual flurry of award activity in the final quarter of the federal fiscal year.

Federal IT Vendors Standing Up Dedicated Advisory Practices

General Dynamics Information Technology (GDIT) launched a digital transformation (DX) consulting practice in 2Q23, leveraging its network of Centers of Excellence and Emerge Labs, as well as the expertise gained from the more than 4,000 research initiatives that have provided its clients actionable market insights on emerging technologies like AI.

On the heels of GDIT’s announcement, ManTech acquired Definitive Logic Corp. to accelerate the development of its own digital transformation consultancy, adding 330 employees skilled in digital transformation services like data engineering.

What This Means for You

Leading federal integrators will keep a close eye on their midmarket IT services peers, perhaps ahead of renewed M&A activity by the top-of-the-market firms. There is still the threat of a government shutdown during FFY2024, and top-tier integrators have all factored that into their plans for 2024.

Expanding advisory capabilities points not only to the capabilities needs of the vendors that are launching consulting operations but also to the importance of advisory competencies in federal digital transformation.

Conclusion

Technology procurement by federal agencies in 2024 is likely to continue at a brisk pace, as evidenced by expanding outlays for IT initiatives in the Biden administration’s FFY2024 budget across the civilian, defense and intelligence sectors. Several federal systems integrators have also tendered projections for continued robust top-line growth in 2024, even if there is a government shutdown during FFY2024.

As such, TBR is confident there is headroom for growth for not only the legacy federal IT vendors but also their smaller, Tier 2 federal integration peers as well as commercially centric technology companies looking to make inroads into the federal space.

Subscribe to TBR’s Insights Flight to receive exclusive federal IT services content, including excerpts from our top research and invitations to upcoming TBR Insights Live sessions with our subject-matter experts.

https://tbri.com/wp-content/uploads/2024/01/TBR_INFOGRAPHIC_Gimme3_FedITServicesBM_1Q24.png2000800John Caucis, Senior Analysthttps://tbri.com/wp-content/uploads/2021/09/TBR-Insight-Center-Logo.pngJohn Caucis, Senior Analyst2024-01-18 17:03:052025-01-06 11:34:12Top 2023 Takeaways for the Federal IT Services Market [Infographic]

On Jan. 3, 2024, SoftwareOne announced its acquisition of Novis Euforia, a Spain-based SAP and cloud services boutique. This special report reflects TBR’s discussion with Pierre-Francis Grillet, SoftwareOne’s global lead for SAP Services, immediately following the announcement, as well as TBR’s ongoing analysis of SoftwareOne and the SAP landscape.

With New Talent and IP, SoftwareOne Extends Into SAP S/4HANA

According to Grillet, SoftwareOne intends to improve its position in the overall SAP ecosystem by moving beyond helping clients with cloud migrations into a more comprehensive SAP S/4HANA transformation role. To meet that aspiration, SoftwareOne’s acquisition of the Spain-based SAP boutique Novis Euforia adds experience and competencies around technically driven SAP S/4HANA migrations and positions SoftwareOne to better address growing client demand for modernization with minimal disruption and transformation through the journey to SAP S/4HANA.

While only a 35-person company, Novis Euforia marks about an 8% increase in SoftwareOne’s SAP practice, which Grillet said would be further bolstered by 15 senior functional data architects who are focused on finance and supply chain as well as ongoing growth in traditional SAP technical areas. Grillet believes the Novis Euforia acquisition and the new hires will significantly improve SoftwareOne’s SAP revenues, adding to his assessment that SAP has high growth potential for SoftwareOne.

Upcoming TBR Insights Live: Join TBR’s Cloud team for a deep dive into how vendors will capitalize on new GenAI-led opportunities to combat the general slowing of cloud market opportunity growth in 2024!

Expanding on clients’ current concerns around SAP, Grillet noted that larger-scale competitors, such as the global systems integrators (GSIs), have increasingly embraced clean core as a means to rein in the rampant customizations often blamed for slowing migration to SAP S/4HANA and limiting innovation on SAP.

In SoftwareOne’s experience, according to Grillet, customizations fall into three categories: unused and therefore nonconsequential; used but no significant remediation required; and used with more complex remediation required. Notably, Grillet added, “a good part of remediations can be automated, further reducing the impact of customizations on the conversion to SAP S/4HANA effort.” A GSI’s greenfield engagement can be relatively expensive, in Grillet’s view, in contrast to SoftwareOne’s focus on preparation prior to a pragmatic and manageable approach to SAP modernization.

Further, Grillet said SoftwareOne has positioned itself well for negotiating a client’s best deal with SAP, given SoftwareOne’s vast experience around licensing and usage. Massive-scale enterprises undoubtedly need GSIs’ capabilities in complex SAP transformations, but many large and most small and midsize enterprises, in SoftwareOne’s view, can be better served through an incremental approach to transformation, framed by a deeper appreciation for customizations’ true hurdles.

Grillet also noted that, “Data, in particular, is relevant in the context of the Novis acquisition, as SNP automates the data transformation and conversion from ECC (ERP Central Component) to SAP S/4HANA, enabling, for example, company code and chart of account rationalization when moving to SAP S/4HANA.”

Gorging on a Massive Pie

The services opportunity around SAP S/4HANA transformations is immeasurable as credible estimates vary widely and, to some degree, do not matter. Services vendors with the available talent and credibility will not lack customers seeking help, especially as SAP’s self-imposed 2027 ECC deadline relentlessly approaches.

SoftwareOne’s latest acquisition helps the company address a larger range of client challenges and expands its footprint in Spain, with expectations of extending into Latin America and South America. While SoftwareOne’s SAP practice, at 500-plus SAP-trained professionals, lacks the scale of the largest GSIs, the vast majority of clients are not dismissing potential services providers because of scale — if you have the talent available now, you are hired. (OK, it is not that dramatic of a seller’s market now, but it will be before the end of 2027.)

Grillet also noted to TBR that one of the company’s “biggest assets is the fact that most of [SoftwareOne’s] professionals are dual-certified and also hold certifications for the three main hyperscalers: Microsoft, AWS and Google. They have a deep understanding not only of the SAP systems but also the platform they run on.”

In TBR’s view, SoftwareOne has consistently played to its own strengths, such as a deep inside view of midsize and large enterprise IT environments, to include spending and actual software usage. This recent acquisition continues that strategy, comes amid a slow-growing rush to add talent around SAP S/4HANA, and should allow SoftwareOne to extend its client base for SAP services over the next few years.

With six successful acquisitions in recent years, SoftwareOne has proven to be adept at integrating capabilities and leveraging IP. This seventh will continue SoftwareOne’s good fortune and make the vendor a must-watch competitor in the SAP space. Success will also depend on SoftwareOne’s ability to use the 15 senior functional data architects it is gaining as a bridge between existing cloud migration capabilities and SAP S/4HANA business transition opportunities, thus helping the company elevate the brand’s permission around SAP, a necessary step to avoid getting stuck in the increasingly commoditized migration services space.

Grillet summed up SoftwareOne’s position by noting that, “The ability to bridge between cloud migration to SAP S/4HANA conversion will depend on more than just these 15 new resources. It will be achieved through the extension of the services portfolio and its [the portfolio’s] underlying tools and IP — including adoption and embedding of the SNP tooling — successfully engaging in the early advisory and preparation engagements, and building an ecosystem of culturally aligned, functionally oriented partners in the various markets where SoftwareOne delivers its SAP services.”

https://tbri.com/wp-content/uploads/2024/01/network-5113917_1280.jpg8531280Patrick Heffernan, Practice Manager and Principal Analysthttps://tbri.com/wp-content/uploads/2021/09/TBR-Insight-Center-Logo.pngPatrick Heffernan, Practice Manager and Principal Analyst2024-01-18 16:47:512024-01-18 16:47:51SoftwareOne Aims for More Comprehensive SAP S/4HANA Transformation Role With Novis Euforia Acquisition

Everyone has an opinion on how generative AI (GenAI) will change the world. At TBR, we have analysis on how companies across the technology space, from consulting firms to hardware vendors, have adjusted investments, business models and alliance strategies to take advantage of the hype and position themselves for the coming reality of GenAI.

Join TBR Principal Analyst Patrick M. Heffernan and Principal Analyst Boz Hristov Thursday, Feb. 15, 2024, at 1 p.m. EST/10 a.m. PST for a free 30-minute TBR Insights Live discussion and Q&A on one of our newest research report, the AI and GenAI Market Landscape. The pair will review specific examples of technology companies’ activities in 2023 as well as what to expect across the GenAI landscape in 2024.

In This FREE TBR Insights Live Session on GenAI Use Cases in 2024 You’ll Learn:

Which strategies leading tech companies have followed to leverage the attention around and investment in GenAI to gain an advantage in their respective markets

How tech companies are using alliances to extend their reach within enterprises and across the larger GenAI — and emerging tech — ecosystem

Which consultancies, IT services vendors, cloud and software companies, and infrastructure players are best positioned for the next wave in GenAI

TBR webinars are held typically on Thursdays at 1 p.m. ET and include a 15-minute Q&A session following the main presentation. Previous webinars can be viewed anytime on TBR’s Webinar Portal. For additional information or to arrange a briefing with our analysts, please contact TBR at [email protected].

https://tbri.com/wp-content/uploads/2024/01/TBR_WI_AIGenAIML_1Q24_RegisterNow_Square-1.png10801080TBRhttps://tbri.com/wp-content/uploads/2021/09/TBR-Insight-Center-Logo.pngTBR2024-01-16 16:12:172024-03-18 13:09:15Beyond the Proof of Concept: GenAI Use Cases in 2024

On Jan. 9, 2024, HPE and Juniper announced they had entered a definitive agreement through which HPE intends to acquire Juniper Networks for approximately $14 billion in cash. The planned acquisition is expected to close in late 2024 or early 2025 should the agreement receive regulatory and Juniper shareholder approval. By acquiring Juniper, HPE’s networking capabilities, especially around AI-enabled networking, will be immediately bolstered. Naturally, the acquisition would also support HPE’s edge-to-cloud vision. Additionally, TBR predicts Juniper’s SaaS assets will be integrated into HPE’s GreenLake platform, which would strengthen GreenLake’s value proposition and expand the audience of enterprise customers.

Acquiring Juniper Networks Will Bolster HPE’s Edge-to-cloud Networking Capabilities

Demand for networking solutions that securely connect, protect and analyze companies’ data will continue to rise as AI workloads proliferate across a variety of industries and organizations increasingly leverage hybrid cloud architecture. Recognizing these trends, Hewlett Packard Enterprise (HPE) has been increasing its focus on networking to meet the demands of existing infrastructure customers and further differentiate from its main infrastructure OEM competitors.

Meanwhile, Juniper Networks also identified opportunities presented by trends in AI and hybrid cloud, understanding that customers were seeking simplified networking solutions with an emphasis on flexibility in consumption and deployment. As such, the company prioritized the expansion of capabilities associated with empowering cloud-managed, AI-enabled networking operations.

HPE’s Road to Enterprise Networking Prominence Began with Aruba

With the development of mobile technologies enabling internet-based data transmission, enterprises began to realize the need for network modernization, supporting the ramping of cloud-driven digital transformation initiatives in the early 2010s. This gave rise to the wireless or mobile enterprise model, which is a near requirement in today’s business landscape.

However, at this time, HPE’s networking expertise was somewhat limited to wired switching. The company knew it would have to expand its portfolio of wireless mobility solutions to remain competitive, and in March 2015, HPE announced plans to acquire Aruba Networks, a leading provider of network access solutions for the mobile enterprise.

After closing the acquisition in May 2015, HPE immediately began to see a return on its investment, with the company’s networking segment revenue growing approximately 8% year-to-year in 2015, driven primarily by Aruba’s inorganic revenue contribution to the business, which centered on wireless local area network (WLAN) products.

In addition to accreditive top-line impacts, the Aruba acquisition drove increasing gross profitability at the corporate level. Over the next few years, HPE leaned further into the WLAN space, leveraging its acquired Aruba assets. In 2018 HPE reorganized its reporting structure, forming its Intelligent Edge segment, which consists of two subsegments, HPE Aruba Products and HPE Aruba Services, and unified the company’s WLAN, campus and branch switching, and edge compute networking solutions.

The formation of HPE’s Intelligent Edge segment promoted deeper portfolio synergies, supporting the development of new Aruba software and services offerings, including “as a Service” and consumption models for the Intelligent Edge portfolio of products, which benefited the company’s GreenLake “as a Service” business, boosting HPE’s annual recurring revenue (ARR) and the strength of the company’s Network as a Service (NaaS) capabilities.

The importance of HPE’s Intelligent Edge segment as it relates to the company’s corporate performance was further underscored in recent years as demand for traditional servers and storage stagnated and began to decline due largely to market cyclicality. In the trailing 12-month (TTM) period ending 3Q22, HPE’s compute and storage revenues fell 10.2% and 6.3% year-to-year, respectively, while Intelligent Edge segment revenue soared, growing 41.6% year-to-year.

To further contextualize the segment’s growth, what started out as 9.9% of HPE’s total revenues in 2018 quickly grew to represent 13.3% of the company’s revenue in 2022, and in the nine months ended 3Q22, Intelligent Edge contributed over 19% of the company’s corporate top line. On top of this, since 2020 Intelligent Edge has contributed a disproportionately high amount to total segment operating income relative to the segment’s revenue contribution. In 2020, 2021 and 2022, Intelligent Edge accounted for 13.4%, 15.9% and 18.1% of HPE’s total segment operating income, respectively, highlighting the opportunity to provide high-value products and services to customers.

Juniper’s Cloud-managed, AI-enabled Networking Solutions and Expertise Add Another Dimension to HPE’s Intelligent Edge Portfolio

As more and more organizations embarked on cloud-driven digital transformation journeys, it became clear that consumption and deployment flexibility were key priorities among most organizations. Recognizing this, Juniper acquired Mist Systems, a leader in AI-powered, cloud-managed wireless networks, in 2019. Mist’s AI-driven WLAN platform was a strong complement to Juniper’s wired LAN, SD-WAN and security solutions, laying the groundwork for Juniper’s Mist AI platform, which has been key to the company’s growth since the closing of the acquisition.

In 2020 Juniper continued its acquisition spree with the purchase of 128 Technology, a networking company known for its session-smart networking technology that enables customers to create user-experience-centric fabric for WAN connectivity that is not only simplified and secured but also efficient and agile, basing networking decisions on real-time user sessions as opposed to static network policies. By incorporating 128 Technology’s session-smart technology into Juniper’s AI-driven enterprise network portfolio, Juniper sought to accelerate the adoption and development of modern AI-driven networks aimed at optimizing the user experience from edge to cloud.

Through these acquisitions, Juniper became a leader in AI-driven enterprise networking, which supported the company’s expanding top line. In the TTM periods ending 3Q20, 3Q21 and 3Q22, Juniper’s AI-Driven Enterprise operating segment revenue, which includes Mist and Technology 128 offerings, has grown 20.4%, 22.7% and 45.9%, respectively, year-to-year. For context, Juniper’s corporate revenue expanded just 5.1%, 10.6% and 9.6%, respectively, year-to-year over the same TTM periods, highlighting Juniper’s focus on AI-Driven Enterprise as well as the market’s strong appetite for these offerings.

HPE to Solidify Its Presence as an Industry Leader in the Networking Space by Integrating Juniper’s Mist AI Platform into its Existing Portfolio

Juniper’s portfolio of solutions somewhat overlaps that of HPE; however, much of this overlap is complementary. For example, both companies have competency in WLAN, SD-WAN, and enterprise and campus switching, but Juniper’s AI-native networking technology and expertise will bolster the capabilities of HPE’s existing offerings.

Uniquely, Juniper’s Mist AI platform leverages AI, machine learning and other data science techniques to simplify operations across wireless access, wired access and SD-WAN domains in a way that optimizes the user experience from the edge to the cloud. Essentially, Mist AI brings greater insight and automation to network operators, which improves the end-user experience and is a compelling reason why HPE is moving to acquire the company. Additionally, Juniper’s portfolio lends HPE net-new competencies around WAN routing as well as network firewalls.

HPE has been vocal in expressing its commitment to grow its highly profitable Intelligent Edge segment revenue stream as the company recognizes the massive opportunity presented by the onset of the generative AI (GenAI) revolution. Should the acquisition close, HPE is expecting to double its networking business, integrating Juniper’s solutions and expertise, especially as it relates to the Mist AI platform, with its own rapidly expanding Intelligent Edge segment.

By integrating Juniper’s Mist AI platform with its existing technologies and offerings, HPE will further differentiate from its infrastructure OEM peers as an AI-driven networking provider, building a networking portfolio rivaling that of Cisco (Nasdaq: CSCO). However, HPE’s acquisition of Juniper would arguably propel HPE’s portfolio past that of Cisco and other major networking players in terms of technological advancement specifically through an AI-driven networking lens. Juniper’s deep relationships with telcos and service providers and the company’s large router install base will also expand HPE’s addressable market.

Similar to how HPE integrated Aruba’s management platform into GreenLake, should the Juniper acquisition close, TBR expects HPE will fold Juniper software and services into GreenLake, bolstering HPE’s GreenLake for Networking solution, formerly GreenLake for Aruba. This anticipated move would enhance HPE’s GreenLake value proposition compared to Dell APEX and Lenovo TruScale while fueling continued GreenLake ARR growth, supporting the company’s edge-to-cloud strategy and improving its profitability.

Additionally, TBR believes that if the acquisition closes, HPE will integrate Juniper’s product offerings into HPE’s “as a Service” portfolio, further augmenting the company’s NaaS offerings.

https://tbri.com/wp-content/uploads/2024/01/Acquisition-Hologram-Futuristic-Interface-Augmented-Virtual-Reality_Rolling-Cameras_Canva.png10801080Ben Carbonneau, Senior Data Analysthttps://tbri.com/wp-content/uploads/2021/09/TBR-Insight-Center-Logo.pngBen Carbonneau, Senior Data Analyst2024-01-12 17:33:202024-01-12 19:19:33HPE Doubles Down on Edge-to-cloud Vision with Acquisition of Juniper Networks

As Peraton considers going public, it needs to generate predictable revenue and profit streams to avoid pitfalls like failing to meet the company’s forecasted metrics. When the Carlyle Group took Booz Allen Hamilton public in 2010, it ensured investors that the business was in a position to keep expanding and succeed long-term. Peraton’s and Veritas’ leadership teams will undoubtedly take a similar approach. Peraton has become increasingly competitive over the years, and TBR believes it has facilitated sales expansion each year, but it remains to be seen whether Peraton is fully realizing the benefits of cost-saving measures or if it is consistently meeting its revenue goals. If it is not doing either, it will not go public.

General Dynamics Information Technology (GDIT) and other unencumbered industry peers have been making rapid investments in emerging technologies like generative AI over the last few years. With Peraton no longer focused on fully integrating its assets, it began to broaden its AI and cloud capabilities more noticeably during 2023 by pursuing strategic relationships with SoftIron and UiPath. These two partnerships, in particular, enable Peraton to leverage SoftIron’s HyperCloud technology as well as the UiPath Business Automation Platform while the company helps clients with establishing their respective cloud networks and streamlining their workflows.

TBR anticipates that Peraton will continue to expand its partner network to operate as a cloud services broker. Peraton is positioning itself to capitalize on federal agencies that are increasingly utilizing an “as a Service” cloud environment model to build their own platforms with desired third-party capabilities as well as the steady funding to accelerate agencies’ digital modernization journeys, which is expected to persist for the foreseeable future.

If Peraton falters with this strategy, it can still continue pursuing opportunities related to next-generation national security. TBR estimates that approximately 45% of Peraton’s sales in 2023 came from the DOD and the IC. Peraton focuses on underpinning missions of consequence that have high barriers of entry and receive bipartisan funding, like protecting space systems, in addition to supporting national security initiatives.

Veritas disclosed in 3Q24 that it had over $40 billion in assets under management. With interest rates expected to remain at elevated levels through 2024, it is unlikely Veritas will make any more multibillion-dollar acquisitions to further augment Peraton. Veritas has demonstrated flexible ownership over the years to work with Peraton. While Veritas has helped take Peraton to new heights and could pursue a sub-$200 million acquisition to broaden Peraton’s capabilities with emerging technologies, Veritas will cash out sooner rather than later.

Peraton has undergone several high-profile leadership changes this year but the most notable announcement is that Steve Schorer will succeed Stu Shea as CEO, president and chairman of the board in September. Schorer was the CEO of Alion Science and Technology before it was acquired by Huntington Ingalls Industries in 2021. Most recently, Schorer has been operating as a senior advisor at Veritas Capital. TBR remains confident that Peraton will go public in 2025 given its recent activity.

Peraton in 2024

The megamerger has given Peraton the necessary portfolio depth and scale to regularly vie with industry leaders such as Leidos for enterprise IT contracts in the $500 million to $2 billion range in the federal civilian and health spaces while also capitalizing on Department of Defense (DOD) Intelligence Community (IC) needs. Now that Peraton’s assets are fully integrated, TBR believes that Peraton is on course to surpass $8.0 billion in annual sales during 2024.

Additionally, Peraton’s backlog was last reported at $24.4 billion in the middle of 2022. The company has been placing around 1,200 bids a year worth approximately $40 billion in total. Peraton has not disclosed its current operating margins.

How Peraton Septupled in Size

Private equity firm Veritas Capital officially bought Harris Corporation’s government IT services business for $690 million in 2Q17. The new assets were quickly spun into a stand-alone company, Peraton, helmed by Stu Shea to pursue opportunities in the communications, cybersecurity and space markets.

When he was first brought on as Peraton’s president, CEO and chairman of the board, Shea expected that Veritas would financially back his plans for three years before cashing out since the fund was for five years. As part of Shea’s growth strategy, Peraton purchased Strategic Resources International to augment the company’s telecommunication services portfolio in 2Q18 and Solers in 2Q19 to expand its space capabilities. While Peraton did not share the financial values of these transactions, the latter enabled Peraton to generate over $1 billion in annual revenue.

An Arduous Integration Process

In 4Q20, more than three years after appointing Shea, Veritas’ leadership team approached him about Veritas acquiring the IT services operations of three Northrop Grumman business units (collectively referred to as NGIT) and federal IT vendor Perspecta and rolling these assets into Peraton. Veritas purchased NGIT for $3.4 billion in 1Q21, before acquiring Perspecta for $7.1 billion in 2Q21 and bolting on ViON’s cloud operations to Peraton in 3Q23.

Anecdotally, Peraton entered this megamerger with industry-leading margins. Following the merger, Peraton’s sales septupled to between $7.0 billion and $7.2 billion in 2021, according to TBR’s estimates, while its headcount surged from 3,500 to 24,000.

The largest privately owned federal IT contractor faced hundreds of thousands of obstacles at the start of this integration process, according to Shea. As the leadership team streamlined policies and processes while optimizing the business, they made several notable decisions, such as divesting the systems engineering, integration and support services business to a portfolio company of Veritas. (These assets would later become Arcfield and are still owned by Veritas.)

By divesting this business, Peraton ensured it was fostering ethical business practices by mitigating potential corporate conflicts while narrowing its focus on core operations. In addition to the divestment, Peraton reduced its physical footprint from 150 facilities to less than 100. The company also made sweeping workforce rationalizations, shrinking its post-merger headcount from 24,000 in 2021 to 18,000 by the end of 2022. Concurrent with implementing these optimization efforts, Peraton had to contend with an array of impeding factors that plagued other vendors across the industry including supply chain disruptions, macro inflation and a sustained bid protest environment.

Despite this onslaught of obstacles, Peraton has been able to consistently disrupt in the public sector market. The company has been able to successfully compete with Tier 1 vendors to secure high-profile contracts such as the Special Operations Forces IT Enterprise Contract III worth up to $2.8 billion. By August 2022, Shea claimed Peraton only had a few hundred items left to address in its integration master schedule.

https://tbri.com/wp-content/uploads/2024/01/IPO-just-ahead-road-sign-concept_Getty-Images_Canva.png10801080James Wichert, Analysthttps://tbri.com/wp-content/uploads/2021/09/TBR-Insight-Center-Logo.pngJames Wichert, Analyst2024-01-11 19:02:252024-09-09 15:52:50Peraton Could Surpass $8B in Sales in 2024, but Will It Go Public?

We may request cookies to be set on your device. We use cookies to let us know when you visit our websites, how you interact with us, to enrich your user experience, and to customize your relationship with our website.

Click on the different category headings to find out more. You can also change some of your preferences. Note that blocking some types of cookies may impact your experience on our websites and the services we are able to offer.

Essential Website Cookies

These cookies are strictly necessary to provide you with services available through our website and to use some of its features.

Because these cookies are strictly necessary to deliver the website, refusing them will have impact how our site functions. You always can block or delete cookies by changing your browser settings and force blocking all cookies on this website. But this will always prompt you to accept/refuse cookies when revisiting our site.

We fully respect if you want to refuse cookies but to avoid asking you again and again kindly allow us to store a cookie for that. You are free to opt out any time or opt in for other cookies to get a better experience. If you refuse cookies we will remove all set cookies in our domain.

We provide you with a list of stored cookies on your computer in our domain so you can check what we stored. Due to security reasons we are not able to show or modify cookies from other domains. You can check these in your browser security settings.

Other external services

We also use different external services like Google Webfonts, Google Maps, and external Video providers. Since these providers may collect personal data like your IP address we allow you to block them here. Please be aware that this might heavily reduce the functionality and appearance of our site. Changes will take effect once you reload the page.

Google Webfont Settings:

Google Map Settings:

Google reCaptcha Settings:

Vimeo and Youtube video embeds:

Privacy Policy

You can read about our cookies and privacy settings in detail on our Privacy Policy Page.