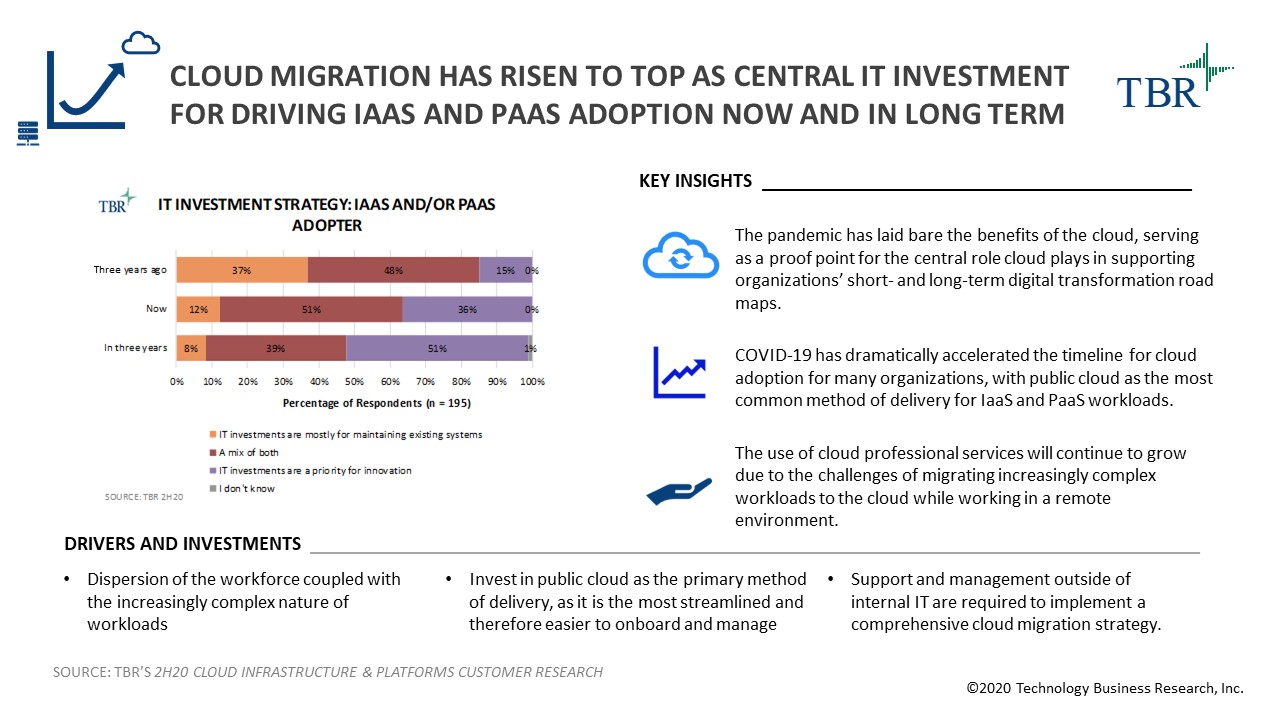

The pandemic has laid bare the benefits of the cloud, serving as a proof point for the central role cloud plays in supporting organizations’ short- and long-term digital transformation road maps.

COVID-19 has dramatically accelerated the timeline for cloud adoption for many organizations, with public cloud as the most common method of delivery for IaaS and PaaS workloads.

The use of cloud professional services will continue to grow due to the challenges of migrating increasingly complex workloads to the cloud while working in a remote environment.

TBR’s Cloud Applications Customer Research tracks how customers are modernizing application environments and choosing between different cloud delivery methods. Leveraging in-depth conversations between TBR and enterprise customers, the Cloud Infrastructure & Platforms Customer Research provides subscribers with actionable insight that they can use to better understand their customers’ behavior and win cloud infrastructure deals. Topics covered for both reports include public, private and hybrid delivery options; decision-making involvement and criteria; leading vendor perception; field positioning and competition guides; and the impact of emerging trends (e.g., containers, security, platforms).

https://tbri.com/wp-content/uploads/2021/01/TBR_CloudInfrastructureCR_2Q20_Cloud_Infog.jpg7201280adminhttps://tbri.com/wp-content/uploads/2021/09/TBR-Insight-Center-Logo.pngadmin2021-01-20 11:30:002022-10-05 16:07:00Cloud migration rises to top as central IT investment for driving IaaS and PaaS adoption

Pandemic-related cloud adoption continues, with more multiproduct, mission-critical SaaS implementations planned for 2021

The outbreak of COVID-19 led to constraints around enterprise IT budgets, but the emergence of a digital workforce resulted in accelerated adoption of cloud applications, particularly those related to productivity and customer-facing suites in the front office. Enterprises needed to rapidly shift operations to the cloud to support remote workforces, increasing the value of service arms and IT services partners to mitigate client risk in the form of cloud road-mapping, migration and implementation services.

In the long term, internal service capabilities and IT services partners will become critical to enabling enterprises’ digital transformations, particularly as front-office cloud deployments mature and as clients explore migrating more customized environments like ERP to cloud or pursue industry-based solution deployments in highly regulated industries like healthcare and the public sector.

The bulk of enterprises are employing a best-of-breed approach to the development of their cloud IT architectures, evidenced by 42% of respondents stating that they currently use three or more SaaS vendors. As a result, application vendors have been driving alliance activity with infrastructure providers to give clients more flexibility around how they consume cloud, evidenced by SAP’s decision to offer SAP Business Suite 4 HANA with leading infrastructure players like Microsoft Azure and Amazon Web Services. While best-of-breed IT will remain prevalent, cloud players have increasingly driven investments to tighten the integrations of complementary suites to expand share of client wallet by enabling multiproduct deals, a tactic that has been effectively employed by Salesforce and Microsoft in 2020.

Cloud players aim to accelerate the proliferation of their IP by employing industry-based go-to-market capabilities to provide clients with prebuilt data models that alleviate concerns around data compliance and governance. This tactic aligns with clients’ needs, as 51% of respondents who deployed industry solutions cited compliance and regulatory standards as a key benefit. To strengthen the value of industry clouds to clients, vendors are offering prebuilt integrations with leading data providers, such as Microsoft’s integrations with electronic health record providers through Cloud for Healthcare. These types of integrations will be critical to accelerating client time to value, while ensuring the integrity of data by meeting industry-specific regulations.

TBR’s Cloud Applications Customer Research tracks how customers are modernizing application environments and choosing between different cloud delivery methods. Leveraging in-depth conversations between TBR and enterprise customers, the Cloud Infrastructure & Platforms Customer Research provides subscribers with actionable insight that they can use to better understand their customers’ behavior and win cloud infrastructure deals. Topics covered for both reports include public, private and hybrid delivery options; decision-making involvement and criteria; leading vendor perception; field positioning and competition guides; and the impact of emerging trends (e.g., containers, security, platforms).

https://tbri.com/wp-content/uploads/2020/01/cloud-2457632_1920.jpg13571920TBRhttps://tbri.com/wp-content/uploads/2021/09/TBR-Insight-Center-Logo.pngTBR2021-01-20 11:30:002021-01-20 11:30:00Accelerated cloud adoption will persist even after COVID-19 pandemic subsides

The STEM field is growing, creating tremendous opportunity for well-trained applicants. While STEM has traditionally been a male-dominated field, cultivating interest at the undergraduate level can help draw in more women who may have the necessary skills but have never considered STEM as a career path. In TBR’s monthly series Women in STEM, we discuss how female leaders have successfully pursued careers in STEM and are encouraging more female representation by passing on the lessons they’ve learned to other women who are pursuing this path.

Meet Jennifer Glick, a quantum computing applications researcher at IBM

Jennifer Glick received her doctorate in physics in 2017 for her work on the quantum information theory of measurement. In 2020 Glick was selected as one of MIT Technology Review’s 35 Innovators Under 35 for her work in quantum computing.

Jennifer Glick, IBM Quantum Computing Applications Researcher

In her current role at IBM, Glick identifies promising quantum applications and develops proofs of concepts that drive advancements in quantum algorithms and methods. This work is essential to moving quantum computing from labs to the real world. In our recent discussion with Glick, she spoke of viewing college with an outcome mindset and boosting learning through free online resources as well as navigating the science path to a quantum career.

Encourage women to pursue STEM careers by being available to answer questions

Navigating the transition from academia to the corporate world can be difficult as universities do not always provide significant scaffolding during students’ academic career. For the highly specialized STEM fields, this is particularly true. But Glick recommends embracing this perceived roadblock with a growth mindset. “It turns out, [a growth mindset] is a great antidote to the impostor syndrome. Strategically seek out new experiences, ideas and challenges that get you out of your comfort zone,” says Glick. “It’s surprising how much you can learn just by observing the people around you.”

Glick adds that leaders in STEM fields can encourage young women to pursue careers in STEM by helping foster their initial interest and supporting them as that interest flourishes. Glick practices what she preaches, having mentored high school, undergraduate and graduate students while working toward her Ph.D.

View college with an outcome mindset, and then build backward with coursework

Many companies take a solutions outcome approach to their technology investments. Customers seek a particular outcome, and vendors then build architectures behind the scenes to enable that outcome. The customer does not necessarily know or care what underlying infrastructure they obtain as long as the desired outcome is achieved.

Education and how it relates to career choice can be thought of in a similar way. We compartmentalize education as something you complete before you start a career, but the reality is that lifelong learners are more likely to have successful careers. Glick’s advice to women considering a career in quantum computing is, “Study a combination of quantum physics, computer science and applied mathematics. A Ph.D. in physics is not strictly a prerequisite for working in quantum computing.”

Retool your existing skills via free online resources

For many, the idea of going back to college for additional degree work is unattainable. For those without existing degrees in quantum-related areas, Glick recommends leveraging free online resources to learn as much as you can on your subject of interest. As the field of quantum computing matures and expands, many related jobs in the industry are emerging, including around software engineering, sales, marketing and design. A variety of skills are necessary for the field of quantum computing to have long-term success. “Pay attention to key thought leaders in quantum computing — they can offer insight into where the field might be headed in the years to come,” says Glick.

Additionally, Glick recommends finding internships within the industry. Well-established STEM fields frequently offer internships to help apprentice young people seeking to work in fields with skills shortages. As careers in STEM become more technical, undergraduate degrees lay the foundational knowledge but on-the-job-training is the most valuable way to obtain the specialized skills necessary to succeed in STEM. A longstanding challenge with internship access has been physical location. However, COVID-19, for all of the hardships it has created, has connected the world digitally more than ever before. Young people in rural locations can now access internships and training at major metropolitan corporations virtually, which removes this physical location roadblock.

Don’t be daunted by the science: Quantum is a growing field with nonscientific opportunities as well

Perhaps Glick’s most important piece of advice is the reminder that emerging and complex scientific technologies are accessible. “Start using quantum computers,” says Glick. “Contribute to open-source software, try the circuit composer on the IBM Quantum Experience, use Qiskit to design and test quantum circuits and algorithms.” IBM has provided ways for people interested in a career in quantum computing, or simply interested in the technology as a hobby, to access it and not only learn from the technology but also eventually teach others. Leveraging online resources and courses, such as the Qiskit Textbook and Qiskit Global Summer School, in conjunction with playing around with IBM’s accessible quantum assets are ways to become smarter around a STEM technology.

https://tbri.com/wp-content/uploads/2021/01/Women-in-STEM-featured-image.jpg8501280adminhttps://tbri.com/wp-content/uploads/2021/09/TBR-Insight-Center-Logo.pngadmin2021-01-15 08:52:002021-01-15 08:52:00Women in STEM: IBM’s Jennifer Glick on navigating the quantum career path

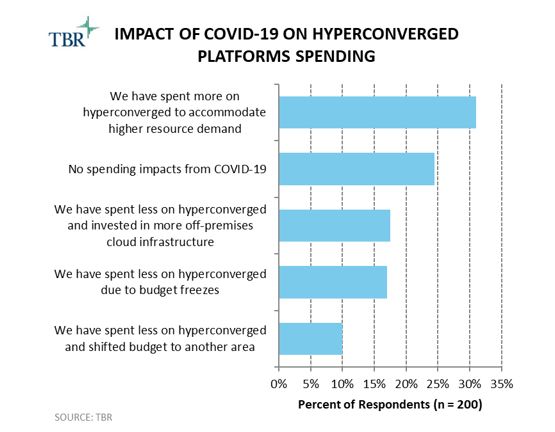

Accelerated demand due to COVID-19 has more vendors focusing aggressively on the HCI market opportunity

Over 40% of data center customers already consume hyperconverged infrastructure and have relatively strong loyalty to their incumbent HCI vendor. Still, 33% of respondents in TBR’s 2H20 Hyperconverged Platforms Customer Research report do not use HCI at this point in time, and HCI vendors will be focusing on this opportunity for market expansion.

Customers increasingly leverage HCI for digital-transformation-related workloads. The edge appears to be a key location for HCI installments, as the technology by definition is well suited for such deployments. IT modernization continues to increase demand for storage and compute capacity in remote and edge locations, and HCI is often the hardware of choice for such use cases.

Because there remains significant opportunity for private cloud and edge infrastructure — two uses for which HCI is heavily leveraged — competition is strong both from within and outside the HCI market landscape. Nontraditional competitors such as Amazon Web Services and ODMs increase their appeal by offering white-box private cloud hardware alternatives. At the same time, HCI vendors increasingly compete against each other and public cloud alternatives by offering new pricing models, as hardware commoditization squeezes the potential for differentiation through infrastructure innovation alone.

TBR’s Hyperconverged & Converged Market Landscape provides a high-level view of both markets, including key trends, recent alliance and acquisition activity, and analysis of the customer adoption cycle, including total market data. This report’s unique differentiator is its inclusion of nine deep-dive vendor profiles. This report largely focuses on which vendors are leaders, laggards and up-and-comers in the hyperconverged and converged markets, providing deep analysis into which vendors are differentiating themselves and how. TBR’s Hyperconverged Platforms Customer Research, which surveys 400 decision makers annually, addresses hyperconverged infrastructure (HCI) vendors’ customer-centric questions, drilling down into key categories such as adoption and budget, purchase drivers, workloads and attributes, purchase patterns, and vendor selection.

https://tbri.com/wp-content/uploads/2021/01/Impact-of-COVID-19-on-Hyperconverged-Platforms-Spending.jpg432555adminhttps://tbri.com/wp-content/uploads/2021/09/TBR-Insight-Center-Logo.pngadmin2021-01-14 13:01:442021-01-14 13:01:44COVID-19 shifts demands in the HCI space, creating opportunity for nimble vendors

On Jan. 13 news broke that Intel CEO Bob Swan will retire and be replaced by Intel alum and current VMware CEO Pat Gelsinger, effective Feb. 15. Although Intel is facing challenges and has suffered setbacks in the last few years, it would be an exaggeration to say the company is in trouble. It dominates PC and server CPUs market share and extracts much greater profits from those devices than do their manufacturers.

Despite share gains by AMD, Intel’s hegemony over the x86 instruction set and its related silicon will assure continued profits for many years, as any transition in such critical components is slow and careful. Swan came to the corner office when Intel was struggling with issues that have persisted, and, in some cases, intensified. Some of these challenges have been self-inflicted from an inside-out perspective, while others have been outside-in threats that internal deficiencies have compounded. Notwithstanding, a growing number of activist investors have been pressuring Intel’s board for leadership change.

The inside-out challenge is to marry manufacturing scale and agility

Intel has enforced the rule of Moore’s Law on the industry for years. Faster, better, cheaper form factors have almost single handedly underpinned the digitization of business and the consumerization of IT throughout much of our daily lives. The inexorable march has seen the rapid rise and fall of business entities as proprietary minicomputer architectures gave way to the Microsoft Windows/Intel CPU, or Wintel, juggernaut that enjoyed a near virtual lock on the market. Intel built its share dominance on two core best practices: chip design and manufacturing.

Each new generation of CPUs requires both a thorough redesign and a massive technically challenging improvement in the chip manufacturing process. For decades, Intel has relied not only on its technical skills but also on its massive revenue to stay ahead of competitors. Other chip vendors rely on third-party chip factories, called foundries. Over the past three years, the main independent foundry, Taiwan Semiconductor Manufacturing Company (TMSC), has outperformed Intel, as has Samsung. The technology race in chip manufacturing is closely related to the thinness of the substrate. Intel has not yet produced its promised 7nm chip, and its current road map states it will not produce 5nm chips until 2023; whereas TMSC and Samsung produced 5nm chips in sample quantities in 2019.

Because of the delay in manufacturing technology, Intel has not been able to meet demand, resulting in PC vendor backlogs. These backlogs have been beneficial for PC vendors, reducing price competition and increasing margins. Intel margins are down, but not severely. The constrained supply made it easier for Intel’s main competitor in PC CPUs, AMD, to gain market share, but because of buyer conservatism and the long lead time necessary to design new PCs, the erosion has been small.

On the server side, Intel has to embrace a more agile manufacturing philosophy and a willingness to essentially become a contract manufacturer of third-party designs as the consolidated Wintel form factor gives way to multiple designs in what is commonly called accelerated computing. At the same time, market uniformity and scale are also giving way. Powerful, small, low-cost form factors are going to proliferate as digitization continues. Edge compute and various smart things will contribute to this shift, and the ability to run smaller manufacturing runs will become paramount.

Revamping Intel’s development process and pivoting to more agile manufacturing will be two core internal challenges confronting Gelsinger, but not the only ones. The outside-in pressures will mount as well.

https://tbri.com/wp-content/uploads/2021/01/martin-katler-7wCxlBfGMdk-unsplash-scaled-1.jpg25601438adminhttps://tbri.com/wp-content/uploads/2021/09/TBR-Insight-Center-Logo.pngadmin2021-01-14 10:02:472023-01-17 15:10:04Can Gelsinger restore the rule of Moore’s Law?

“Elitsa Bakalova, Senior Analyst at research firm Technology Business Research, Inc, said in a report that the Atos-DXC transaction could form the world’s second-largest global IT services vendor, closer to the size of Accenture ($45 billion revenue in 2020) and larger than TCS ($22 billion revenue in 2020). IBM Services, after the Global Technology Services spin-off, is estimated to have a revenue of $23 billion in 2021.” —The Hindu

https://tbri.com/wp-content/uploads/2021/11/TBR-In-the-News.png12001200adminhttps://tbri.com/wp-content/uploads/2021/09/TBR-Insight-Center-Logo.pngadmin2021-01-13 09:47:542022-11-03 20:13:09TCS may lose spot as world’s third largest IT services firm

Nascent trends in the edge computing market should worry telcos

Webscales have various initiatives underway that will disrupt aspects of telcos’ business model, posing a direct threat to their connectivity businesses and ability to capitalize on new value created from 5G and edge computing. Webscales’ rapidly expanding presence in the edge compute space and keen focus on private cellular networks — particularly in the U.S. — are prime examples of this trend.

Though webscales are posturing like they want to partner with telcos on new opportunities, edge compute partnerships involving a webscale and telco to date are more exploitative than cooperative in nature. Arguably, the highest profile agreement to date is between Amazon Web Services (AWS) (Nasdaq: AMZN) and Verizon (NYSE: VZ), and while Verizon has touted the monetization opportunities, it is providing little more than site access and network connectivity, while AWS’ intelligent edge capabilities provide the bulk of the customer value. In this relationship, AWS doles out a cut of the revenue to Verizon while holding on to the customer relationship and most of the value that emanates from the use of its platform.

The end state of this competitive dynamic will see telcos capturing even less value as they increasingly offload towers and other sites to towercos and data center real estate investment trusts (REITs), and as webscales own greater portions of the network.

Webscales and data center players invest in India to capitalize on the nascent digitalization opportunity

India has become the epicenter of webscales’ focus and investment among emerging markets due to the country’s large population and growth prospects. Alphabet (Nasdaq: GOOGL), Amazon, Microsoft (Nasdaq: MSFT) and Facebook (Nasdaq: FB) are all investing billions of dollars in equity stakes, infrastructure build-out, applications and platforms customized to meet the needs of the Indian market, and setting up business model structures. Reliance Jio, Bharti Airtel and Vodafone Idea are partnering with these webscales on various projects to realize this digitalization opportunity in India.

TBR’s Telecom Edge Compute Market Landscape, which is global in scope, deep dives into the edge compute-related initiatives of stakeholders in the telecom market, including telecom operators, cable operators, webscales and vendors that supply the telecom market. The research includes key findings, market size, regional summary, technology trends, use cases, operator and vendor positioning and strategies, and acquisition and alliance strategies and opportunities.

https://tbri.com/wp-content/uploads/2020/03/web-4776833_1920.jpg12801920Michael Soper, Senior Analysthttps://tbri.com/wp-content/uploads/2021/09/TBR-Insight-Center-Logo.pngMichael Soper, Senior Analyst2021-01-12 11:12:412021-01-12 11:12:41Webscales will capture the majority of economic value of telecom edge compute market

“Atos would also get DXC’s security services and solutions capabilities, as well as add 3,000 staff to its already existing team of 5,000 security professionals. It would also gain its digital security services, an area that TBR claims Atos is aiming to increase revenues in — from €0.7 billion in 2019 up to €2.1 billion in the midterm.” — ARN

https://tbri.com/wp-content/uploads/2021/11/TBR-In-the-News.png12001200adminhttps://tbri.com/wp-content/uploads/2021/09/TBR-Insight-Center-Logo.pngadmin2021-01-11 10:17:392022-11-03 20:13:37DXC acquisition expected to bring Atos gain — but not without pain

“‘Atos would directly benefit from the market consolidation of a direct competitor, while DXC Technology, which has historically prioritized its fiduciary responsibility, would seize the chance for its shareholders to capitalize on the opportunity and end its seemingly perennial turnaround efforts,’ according to Technology Business Research.” — CRN

https://tbri.com/wp-content/uploads/2021/11/TBR-In-the-News.png12001200adminhttps://tbri.com/wp-content/uploads/2021/09/TBR-Insight-Center-Logo.pngadmin2021-01-11 10:15:332022-11-03 20:14:005 Things To Know About A Possible Atos-DXC Technology Deal

“Access to quantum systems and vertical-specific use cases is beginning to emerge in more commercially available ways. While quantum computing has yet to achieve economic advantage, these developments are necessary next steps toward this goal.” — WRAL TechWire

https://tbri.com/wp-content/uploads/2021/09/TBR-Insight-Center-Logo.png00adminhttps://tbri.com/wp-content/uploads/2021/09/TBR-Insight-Center-Logo.pngadmin2021-01-11 10:04:242022-11-03 20:18:49Quantum computing momentum builds, especially at Duke, Honeywell

We may request cookies to be set on your device. We use cookies to let us know when you visit our websites, how you interact with us, to enrich your user experience, and to customize your relationship with our website.

Click on the different category headings to find out more. You can also change some of your preferences. Note that blocking some types of cookies may impact your experience on our websites and the services we are able to offer.

Essential Website Cookies

These cookies are strictly necessary to provide you with services available through our website and to use some of its features.

Because these cookies are strictly necessary to deliver the website, refusing them will have impact how our site functions. You always can block or delete cookies by changing your browser settings and force blocking all cookies on this website. But this will always prompt you to accept/refuse cookies when revisiting our site.

We fully respect if you want to refuse cookies but to avoid asking you again and again kindly allow us to store a cookie for that. You are free to opt out any time or opt in for other cookies to get a better experience. If you refuse cookies we will remove all set cookies in our domain.

We provide you with a list of stored cookies on your computer in our domain so you can check what we stored. Due to security reasons we are not able to show or modify cookies from other domains. You can check these in your browser security settings.

Other external services

We also use different external services like Google Webfonts, Google Maps, and external Video providers. Since these providers may collect personal data like your IP address we allow you to block them here. Please be aware that this might heavily reduce the functionality and appearance of our site. Changes will take effect once you reload the page.

Google Webfont Settings:

Google Map Settings:

Google reCaptcha Settings:

Vimeo and Youtube video embeds:

Privacy Policy

You can read about our cookies and privacy settings in detail on our Privacy Policy Page.