Closing the Gap: The Power of Agentic AI in the Persistent Value Pyramid

Three years into the AI era, the market has advanced quickly, but the value pyramid remains bottom-heavy

Although the generative AI (GenAI) cycle began three years ago, the market is still translating that progress into broad-based economic value. Model performance has improved, infrastructure investment has accelerated, enterprise experimentation has broadened, and buyers are recognizing value from early deployments. This progress reinforces TBR’s early view that AI would reshape enterprise work over time through workforce augmentation, task automation and role redesign. Although the long-term promise of AI has not dimmed, realizing the technology’s potential will take longer than was initially expected. The issue is whether enough value can move into the software, services and workflow layers where enterprise productivity is realized. That is the central question about the next phase of the AI market: When — and how meaningfully — will the AI value pyramid begin to invert?

AI infrastructure dominates the broader opportunity, with AI services representing only a small portion of the market today

The AI story remains trapped in a phase dominated by infrastructure investment, but early success in coding platforms offers a glimpse of how AI services revenue will scale over time. GPU and memory chip makers are capturing the largest revenue pools at the base of the pyramid, hyperscalers and neoclouds are monetizing compute delivery in the middle, and AI services providers are capturing a comparatively smaller share at the top. This imbalance is a sign that the cycle remains in its early stage. The first wave of monetization has accrued to the vendors supplying the capacity required to train, host and scale AI. The next wave will need to come from production usage, recurring inference consumption and AI services that deliver clear enterprise outcomes.

Over the long term, the AI value pyramid will need to invert. The market cannot remain structurally dependent on infrastructure build-out if AI is to become a durable enterprise productivity platform. Value will need to move closer to where work is executed, governed and measured. That is the future hyperscalers are investing in as large cloud commitments continue to flow from model developers such as Anthropic and OpenAI. The current distribution is rational for an early technology supercycle, but it cannot be the steady-state structure of the market indefinitely.

The AI value pyramid will need to invert over the long term

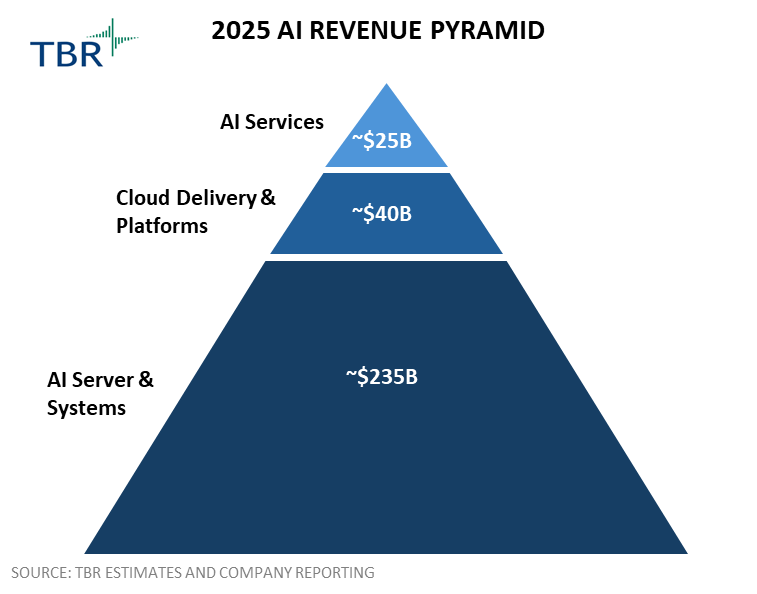

To put rough numbers to the AI value pyramid, across the three buckets of semiconductors, hyperscale delivery and AI services, semiconductor vendors are still capturing the lion’s share of the market. As noted in TBR’s 4Q25 AI Infrastructure Market Landscape, AI server and systems revenue reached an estimated $235 billion in 2025, inclusive of NVIDIA, AMD and hyperscalers. By comparison, TBR estimates 2025 AI cloud delivery and platforms revenue was under $50 billion, inclusive of Amazon Web Services (AWS), Microsoft, Google Cloud and ServiceNow, while AI services revenue was around $25 billion, inclusive of OpenAI, Anthropic, Microsoft, AWS, Google Cloud and ServiceNow.

Put another way, the foundational layer of the AI market saw nearly 10x the revenue opportunity of AI services providers in 2025. This gap is the clearest evidence that the AI market remains early in its value shift. Infrastructure monetized first because the market needed capacity before broad production usage could scale. Over the long term, however, this structure will need to change. If AI is to realize its full enterprise potential, the revenue generated via inference consumption on AI services, workflow management and agentic execution needs to increase.

2026 AI Revenue Pyramid (Source: TBR)

AI end-user perception remains positive, supporting future adoption

Upfront investment ahead of long-term opportunity is normal in a technology supercycle, but the AI services market needs to expand for the broader AI opportunity to be sustainable. Hyperscalers are investing for this future, and TBR’s customer research continues to point to an AI world where customer appetite is growing as early adopters recognize more value than expected from AI-related projects.

In TBR’s upcoming 2H25 AI Applications Customer Research, 55% of respondents are increasing their IT budgets to support AI adoption, up from 48% in 2H24, while 58% of respondents stated AI tools exceeded their expectations for value creation. With buyers seeing value and adjusting budgets accordingly, TBR continues to view end-user demand as robust. The demand side of the pyramid is not the main constraint, but it remains to be seen how quickly vendors can convert that appetite into production usage, recurring consumption and AI services revenue.

Agentic systems and usage-based revenue will accelerate revenue growth, helping close the value gap

The AI services market will not scale simply because the models improve. Instead, the market will scale when AI systems become embedded deeply enough in enterprise workflows to generate sustained inference demand. Agentic systems are the clearest path to that outcome. Unlike first-generation copilots, which primarily assist with discrete tasks, agents are designed to execute multistep work across applications, data sources and governance layers. That matters economically because every step in an agentic workflow creates additional model calls, tool calls and consumption events.

This shift gives AI services vendors a more credible path to monetization. Fixed-seat copilots can demonstrate productivity, but they disconnect usage from revenue and can pressure margins when consumption rises. Agentic systems practically require usage-based pricing because the work performed is more measurable and the consumption profile is more directly tied to business activity. In this model, AI revenue growth comes not from selling more experimental seats but from running more enterprise work through AI-enabled execution layers.

Infrastructure capacity is being built ahead of demand, but that investment will only be justified if inference workloads expand across real production environments. The vendors best positioned to capture that opportunity will be those that control where AI work is governed and managed. Model quality remains important, but workflow control is becoming the more durable source of value.

Code-generation tooling is becoming the first scaled, enterprise agentic AI market

This thesis is already playing out in software development, which is the first scaled example because it combines high labor cost, measurable productivity gains, structured workflows and clear willingness to pay. The adoption of AI tools has significantly increased software developers’ productivity, accelerating code generation and reshaping expectations around the cost of producing software. Executives from several notable software incumbents, including SAP and Salesforce, have boasted about their ability to limit hiring for new developers, with Salesforce leaders stating the company did not hire any in 2025. Software developer job postings on Indeed remain nearly 70% below their highs in 2022, reinforcing the view that the market for developer talent has shrunk significantly over the past three years, while revenues from leading AI code-generation tools, including Claude Code and OpenAI Codex, grow in the triple digits year-to-year.

The market for AI-powered development platforms is also moving toward agentic systems very quickly, trusting tools to leverage codebases, generate changes, test outputs, open pull requests and operate across parts of the development life cycle. As such, code generation is the first scaled enterprise proof point for agentic AI. It is a market where the productivity impact is measurable, user adoption is already material and monetization is scaling very rapidly. It also shows why execution control matters. GitHub has an advantage because it owns the repository, pull request, CI/CD (continuous integration and continuous delivery) and governance workflow. Cursor is gaining traction as an agent workspace. Anthropic and OpenAI are competing through model-native coding agents in Claude Code and Codex. The market is a contest not only between models but also across the workflow control layer, the agent workspace and the model-native execution layer.

Conclusion

The AI market is not failing to meet its promise, but it is still early in translating that promise into broad-based economic value. Three years into the GenAI cycle, the largest pools of revenue remain concentrated in the infrastructure layers required to train, deploy and scale frontier models. That concentration is rational given the scale of compute demand, but it is not a sustainable end state if AI is to become a true enterprise productivity platform.

The next phase of market development will depend on whether the AI value pyramid can begin to invert. Infrastructure investment has created the capacity, but inference demand will need to scale through production usage, workflow integration and consumption-based pricing. Agentic systems are the most credible path to that outcome because they increase AI usage, extend AI into multistep workflows and create a stronger foundation for usage-based monetization. Improvements in code generation show that the market is beginning to change, but broader enterprise adoption will require the same combination of measurable productivity, workflow integration, governance and pricing alignment.

The AI value pyramid should begin to shift over time, but not simply toward model developers. Durable value will accrue to the vendors that control execution. That includes model providers building agent platforms, hyperscalers hosting and metering workloads, SaaS vendors embedding agents into business processes, developer platforms controlling software workflows, and services firms operationalizing AI across complex enterprise environments. For model providers specifically, this means competitive positioning can no longer be measured by benchmark performance alone. Revenue mix, infrastructure access, enterprise adoption, partner alignment, agentic capabilities and workflow integration are becoming more important indicators of vendors’ positioning long-term.