Partnering for growth: How to ensure alliance and partnership success in 2025

In 2025 IT services companies and consultancies will refine their alliances, winnowing lists of 100-plus technology partners to the handful that drive more than 90% of their business, articulate a clear joint value proposition, and align at both the leadership and sales force levels.

A technology- and partner-agnostic approach was always a bit of a fiction and in the coming years will become a relic of the past. To make all that happen, ISV SaaS leaders to AI model providers, global systems integrators to hyperscalers, and semiconductor to platforms vendors will invest in ecosystem intelligence and elevate alliance management within their organizations.

In this TBR Insights Live session, Principal Analysts Angela Lambert, Allan Krans and Patrick Heffernan share insights from TBR’s 2025 Predictions special report Ecosystem Intelligence: Key Strategic Changes for 2025.

In this above session on ecosystem intelligence strategies you’ll learn:

How to place strategic ecosystem bets on alliance partners that are well-positioned for the next growth wave

How competitors are gaining ground with common alliance partners through sales programs, go-to-market motions and training

How to create unique value with alliance partners that resonates with end customers

Excerpt from Ecosystem Intelligence for IT Services, Cloud and Consultancies: Strategic Insights for 2025 Success

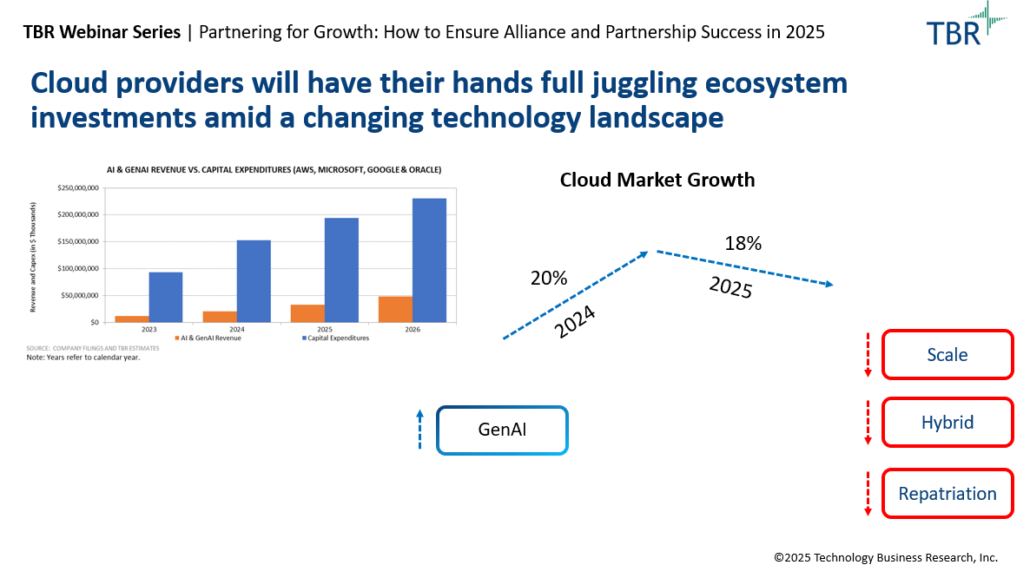

Cloud providers will have their hands full juggling ecosystem investments amid a changing technology landscape

Visit this link to download this session’s presentation deck here.

TBR Insights Live sessions are held typically on Thursdays at 1 p.m. ET and include a 15-minute Q&A session following the main presentation. Previous sessions can be viewed anytime on TBR’s Webinar Portal.

https://tbri.com/wp-content/uploads/2025/02/Eco-Intelligence-Web_1Q25_WatchNow.png10801080TBRhttps://tbri.com/wp-content/uploads/2021/09/TBR-Insight-Center-Logo.pngTBR2025-02-26 13:38:182025-03-20 09:35:20Ecosystem Intelligence for IT Services, Cloud and Consultancies: Strategic Insights for 2025 Success

Attendance at Mobile World Congress (MWC) 2025 is expected to near the annual event’s all-time high set in 2019, underscoring not only the importance of this event to the global mobile ecosystem but also the opportunities and potential inherent in the ecosystem.

Though TBR expects MWC25 to focus on the usual topics that have been popular in recent years, we anticipate there will be more substance at this year’s event, especially as it pertains to private networks, network evolution, business model transformation and the role of AI in the ecosystem, pointing to bright days ahead for companies that are aligned with market and technology trends. And with mobile network operators struggling more than ever to monetize their network investments, the stakes are high for finding the next big thing and understanding where new market disruptions may originate.

In this TBR Insights Live session, Principal Analyst Chris Antlitz and Senior Analyst Michael Soper share top takeaways from Mobile World Congress 2025. The pair also discuss how emerging opportunities are likely to drive technology and business model disruption and impact markets.

In the above session of Mobile World Congress 2025 you’ll learn:

How the telecom industry intends to derive business outcomes from AI

How enterprises are progressing in their digital transformations and incorporating private networks

Where in the mobile ecosystem new value is being created and what telcos need to do to generate ROI from new opportunities

FWA is driving significant top-line revenue for some mobile network operators

Technological innovations makes 5G FWA act like wireless fiber

New technologies mitigate spectrum issues

Visit this link to download this session’s presentation deck here.

TBR Insights Live sessions are held typically on Thursdays at 1 p.m. ET and include a 15-minute Q&A session following the main presentation. Previous sessions can be viewed anytime on TBR’s Webinar Portal.

https://tbri.com/wp-content/uploads/2025/02/MWC25-Webinar_1Q25_Register-Now.png10801080TBRhttps://tbri.com/wp-content/uploads/2021/09/TBR-Insight-Center-Logo.pngTBR2025-02-25 12:28:072025-03-25 09:33:47MWC25: Disruptive Technologies and Business Models Create New Opportunities for the Mobile Ecosystem

Recap: PwC Middle East’s ‘Transforming the Region’ presentation

PwC Middle East’s Feb. 18, 2025, webcast, “Transforming the Region: Future Insights – Economy and IPO Watch,” included a detailed presentation from Richard Boxshall, PwC Middle East’s chief economist, who highlighted the dichotomy between the region’s oil and non-oil economies, at least in Saudi Arabia and the United Arab Emirates (UAE). How does that all relate to TBR’s coverage of technology companies, including the IT services companies and consultancies I keep a close eye on?

In short, energy is stagnant, in terms of both oil price and overall sector growth. In contrast, the non-oil economy is booming, particularly in financial services and transportation. According to Boxshall, around 5,000 projects valued at over $5 trillion are in play in Saudi Arabia alone, reflecting a transformative investment in the country’s economy.

But before you set sail for Riyadh, remember that around half of the Saudi and UAE economies are, as Boxshall put it, “driven by oil,” and those governments depend on oil receipts to fund much of their spending. Uncertainty around oil price puts pressure on the countries’ fiscal positions and budgets, as Boxshall noted. If those prices went higher, for all the benefit that would bring to the government coffers, the economies would also face inflation, rising rents and potentially a drag on the non-oil economy. All that interdependency considered, Boxshall still described the split between the oil and non-oil economies as a “real decoupling.”

So, good news, right? The long-sought-after growth of strong non-oil economies, the eventual weaning of these pivotal Middle East countries from subservience to the price of oil is happening now and happening quickly. And should a trade war break out between the U.S. and the European Union (EU) or the U.S. and China, Saudi Arabia and the UAE — and the rest of the Middle East economies — will suffer. A production surge by the world’s largest oil producer — the U.S. — would further dampen oil prices, constraining Middle East governments’ budgets. Not everything is perfect, but certainly the big picture looks promising: Non-oil economies in oil-led countries have shown persistent, seemingly lasting growth.

Watch on Demand: $130+ Billion Emerging India Opportunity

Why TBR cares: A long history and a fast-changing present

Why does TBR care? Two reasons, one recent and one that goes back decades. First, the latest developments: Nearly every company we cover in the professional services, IT services, and digital transformation services spaces has increased its presence and investment in the Middle East in recent years. We’d like to take some credit for trumpeting the region’s IT possibilities back in 2020 (Egypt and IT and the center of the world), but no matter when or why the most recent surge into the Middle East started, it’s unquestionably become a hot spot (see Figure 1).

Sovereign wealth funds, newly arrived Western venture capital, and the payoffs from a couple decades of vastly improved schools and universities all converged in recent years with well-timed investments in technology and necessary changes to regulatory environments. The steady economic diversification efforts, coupled with new leadership in much of the region and all the factors above, have made the region exceptionally attractive to capital and talent. As one Big Four partner said to me recently, “If I was in my 20s right now, I’d move to Riyadh.”

Company

Coverage

Investment/Growth

Deloitte

Egypt

Innovation Hub and investment of $30 million over five years

KPMG

Saudi Arabia, Jordan, Iraq, UAE, Oman

Merged member firms into one entity to improve operations

Accenture

Kuwait

National Security Operations Center (cybersecurity services)

That leads to the decades-old reason why I’m interested in what’s happening in the Middle East and how those economies are changing. When I was in my 20s, I lived in the region, spending two years in Cairo followed by two in Dubai, UAE. Working for the U.S. government gave me access to regional economic conferences, multinational oil companies, local government ministries and even oil smugglers, all of which shaped my understandings of the energy industry and the region’s economies.

One would be foolish to doubt the Emiratis’ innovativeness, the Saudis’ limitless financial resources or the Egyptians’ belief in their centricity to the entire world. But 25 years ago, the obstacles to thriving non-oil economies, particularly in Saudi Arabia, seemed insurmountable. Looking at the region now through Boxshall’s eyes (and those of my friends still living and working there), it’s too easy to view the transformation as inevitable. Combine diligent reforms, steady investment, smart leadership and a growing population base, underpinned by all that relentless oil money, and, of course, these are thriving economies attracting top talent.

I can’t argue against that. Nor do I have a cautionary note to sound about previous financial crashes in Dubai or charming Saudi leaders or French emperors conquering Egypt. Very simply, when asked decades ago what success would look like, government and business leaders in the region described economic conditions very similar to what we’re seeing today.

https://tbri.com/wp-content/uploads/2025/02/economic-impact_vertigo3d_getty-images.png10801080Patrick Heffernan, Practice Manager and Principal Analysthttps://tbri.com/wp-content/uploads/2021/09/TBR-Insight-Center-Logo.pngPatrick Heffernan, Practice Manager and Principal Analyst2025-02-25 11:56:362025-02-25 11:56:36The Middle East’s Economic Transformation: A Real Decoupling or Persistent Uncertainty?

TBR has been tracking performance of IT services companies for decades. As go-to-market strategies increasingly focus on industry-centric solutions, TBR determined to build trailing 12-month revenue based on a standardized breakout of key industry verticals.

In 2018 we expanded our IT services coverage to include estimates for seven industry vertical splits (full list below), leading to the recent launch of the IT Services Industry Vertical Data Excel file. This extensive data file includes revenue estimates for 17 IT services companies, including Accenture, Capgemini, DXC Technology, IBM and Tech Mahindra (full list below). Quarterly estimates, year-to-year growth, and percentage of IT services totals date back to 1Q21.

This proprietary data stream, in conjunction with our qualitative analysis of these firms, including their partners and how they operate, offers unprecedented intelligence on which companies are growing or maintaining their revenue or experiencing declines within industry verticals and allows for partner adjustments and competitive maneuvering.

TBR’s vertical-specific IT services data reveals notable industry trends

In the most recently published data file, several key insights stand out, including highlights from TBR’s research on Tata Consultancy Services (TCS), Capgemini and Wipro.

Most notable: TCS’ public sector success in India

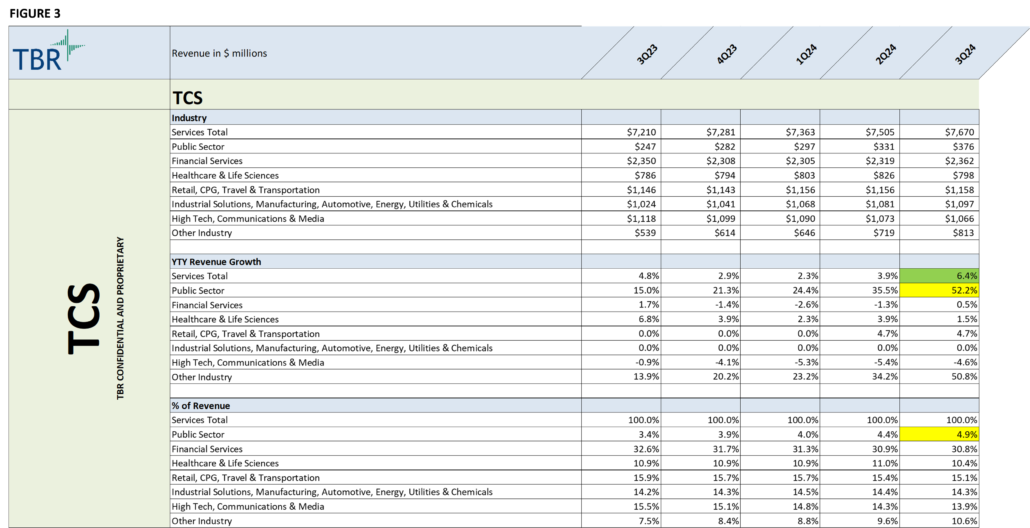

Tata Consultancy Services’ (TCS) public sector revenues jumped 52.2% year-to-year in 3Q24, extending — and accelerating — five straight quarters of double-digit growth. Curiously, however, TBR’s data shows a deviation from the norm in geo data. Reported India revenues by TCS (as a percentage of revenue) have been growing at a mid-double-digit range for over a year. In fact, reported revenue has grown so rapidly that India generated more revenue for TCS than the rest of the Asia Pacific region combined for the first time in 3Q24, and that gap expanded in 4Q24.

While it is unquestionably an impressive growth story, public sector revenue accounts for less than 5% of TCS’ overall IT services revenue, making it strong growth from a relatively small base. Still, 52.2% is impressive relative to the market, and analysis in TBR’s quarterly reports on TCS can help us understand this success. In short: It’s India.

“India was again a bright spot for TCS, nearly doubling its revenue composition from the previous year, now accounting for 8.9% of total TCS revenue. We attribute the growth in India to strong brand reputation and favorable government policies to incentivize companies to digitize their IT operations.” — TBR’s 3Q24 Tata Consultancy Services report

“Although India has historically only accounted for 5% to 6% of TCS’ total revenue, we anticipate this share will rise over the next few years, reaching double-digit figures before peaking and stabilizing. IT spending in India continues to increase, indicating there is plenty of opportunity, particularly for locally based IT services firms such as TCS. For example, during 2Q24 TCS and Indian state-owned telco Bharat Sanchar Nigam Limited announced plans to build four data centers across India to meet rising demand.” — TBR’s 2Q24 Tata Consultancy Services report

According to TBR’s lead analyst on TCS, Senior Analyst Kevin Collupy, “They are killing it with local Indian enterprises and government organizations. And last year we reported on an uptick in consultancies and IT services companies investing in their India-for-India capabilities, offerings and scale. So, 52.2% growth in public sector, even as TCS itself only grew 6.4%, tracks with the overall India growth story while illustrating just how well TCS has been doing.”

Additional insights from 3Q24 data

Capgemini’s revenue declined 1% year-to-year in U.S. dollars (USD) in 3Q24, but the company’s public sector revenue increased by more than 4% in the same period. At 15.1% of the company’s total IT services revenue, public sector revenue significantly buoyed what would have been an even rougher quarter. Retail, CPG, Travel & Transportation declined 4% year-to-year in USD in 3Q24 and accounted for 15.1% of Capgemini’s IT services.

Wipro’s 19.1% drop in public sector revenue in 3Q24 looks terrible, particularly in the context of an overall IT services decline of just over 2%. The vertical did not pull down Wipro as a whole though, as it represents just 0.5% of total revenue. The real culprits were Financial Services (down 1.3%, while accounting for 33.9% of revenue) and High Tech, Communications & Media (down 8.1%, at 15.4% of revenue).

Access all IT services vertical-specific data

While a single quarter is only a snapshot of the market narrative, the numbers in TBR’s vertical-specific IT services data starts to paint the picture while company reports fill out the story. An updated IT Services Industry Vertical Data Excel file will be released quarterly in TBR’s digital platform, Insight Center™.

If you are a current TBR user with access to the IT Services Vendor Benchmark, you can download the IT Services Industry Vertical Data Excel file today. If you’re interested in gaining access to the data, as well as TBR’s entire IT services research stream, start your free trial to Insight Center™.

Vendors covered in TBR’s IT Services Vendor Benchmark Data:

Accenture

Atos

Capgemini

CGI

Cisco Customer Experience

Cognizant

DXC Technology

Fujitsu

HCLTech

Hewlett Packard Enterprise Services

IBM

Infosys

Kyndryl

Tata Consultancy Services

Tech Mahindra

T-Systems

Wipro IT Services

Industry coverage in TBR’s IT Services Vendor Benchmark Data:

https://tbri.com/wp-content/uploads/2025/02/financial-data-analyzing_ispyfriend_getty-images-signature.png10801080Patrick Heffernan, Practice Manager and Principal Analysthttps://tbri.com/wp-content/uploads/2021/09/TBR-Insight-Center-Logo.pngPatrick Heffernan, Practice Manager and Principal Analyst2025-02-19 11:55:062025-02-19 11:55:06New IT Services Vertical Revenue Data Shows TCS’ Public Sector Surge and Market Shifts

NTT DATA turns to partners to unlock new revenue opportunities

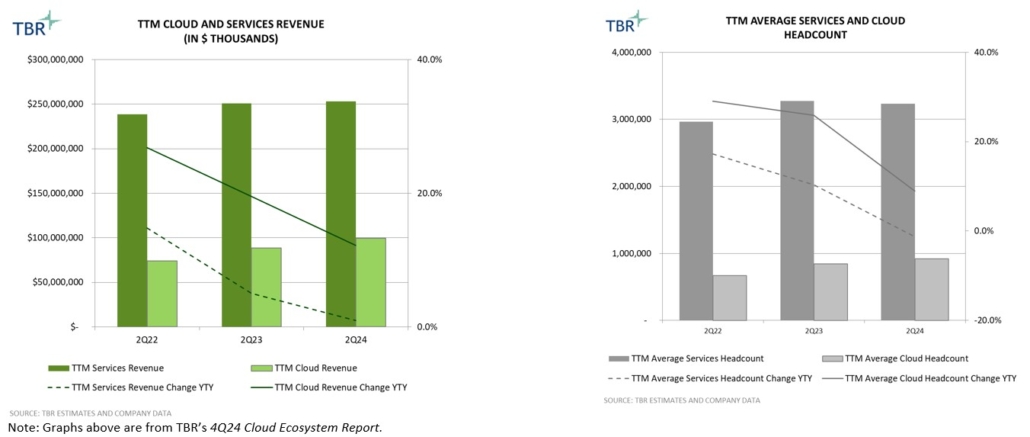

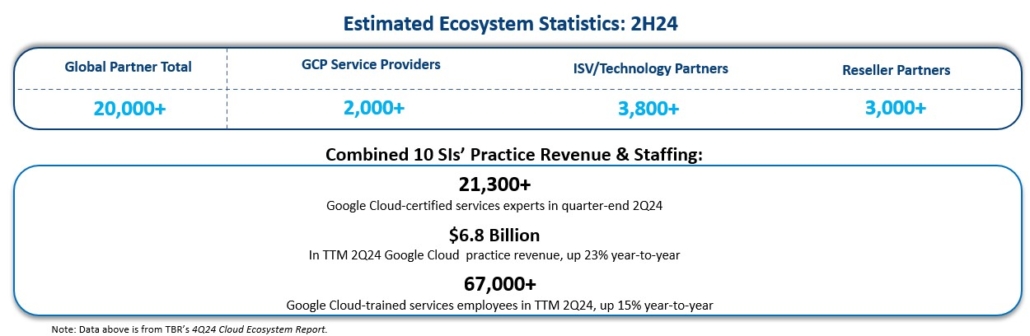

According to TBR’s 4Q24 Cloud Ecosystem Report, “Despite the recent slowdown in overall IT services revenue growth, global SIs (GSIs) remain committed to building out their hyperscaler practices as they try to maintain ecosystem stickiness and ensure they are ready when demand rebounds. GenAI [generative AI] continues to influence both services vendors’ and their hyperscaler partners’ go-to-market strategies with new implications centered on security and data privacy.

This is a natural market evolution as, following the hype and opportunities to experiment with large language model (LLM)-based tools in the past 24 months, enterprises are turning to proprietary data to scale GenAI deployments. This is resulting in the advent of small language models (SLMs), which are the new battleground for partners to prove value. Absent accounting for implications around data and AI security, these relationships will likely face challenges, especially as slower macroeconomic conditions have placed greater emphasis on vendors to ensure service quality. And delivering quality services begins with access to enterprise data.”

A year after completing the integration of various parts of NTT operations and the formation of NTT DATA Group Corp., NTT DATA continues to calibrate its portfolio and skills to protect its No. 2 position in terms of global revenue size among peers within TBR’s IT Services Benchmark. As TBR discussed in the 2Q24 NTT DATA report, the company’s alliance relationships have played an increasing role in these efforts. “Customer demand for cloud migrations remains strong, which presents opportunities for trusted service providers. NTT DATA is building up its alliance network and its internal capabilities around cloud platforms such as Amazon Web Services (AWS), Microsoft Azure and Google Cloud to address demand. By offering complementary services that seamlessly support client transitions to these hyperscaler platforms, NTT DATA is positioning itself to become a critical partner in cloud adoption journeys.”

NTT DATA understands the value of ecosystems

In November 2024 NTT DATA made two strategic announcements highlighting its efforts to strengthen trust and expand addressable market opportunities through its relationship with Google Cloud. First, the two deepened their relationship, forming the NTT DATA Google Cloud Business Unit centered on coinnovation and development of data and AI-ready industry solutions. Second, NTT DATA announced the acquisition — which has since closed — of India-headquartered Niveus Solutions.

The purchase adds over 1,000 cloud engineers with skills in Google Cloud Platform (GCP) including GCP-native modernization, data engineering and AI. Following the purchase of Niveus Solutions, NTT DATA’s GCP-certified headcount now sits at approximately 3,600 professionals. According to TBR’s estimates in the 4Q24 Cloud Ecosystem Report, this is higher than the GCP-skilled headcount at Atos, Capgemini, DXC Technology, IBM, Infosys and Wipro. We estimate NTT DATA’s GCP-related revenue to be north of $400 million, or about 12% of its total cloud revenue, with the bulk of the remaining revenue share generated by the company’s relationships with Microsoft and SAP.

Why Google?

As TBR wrote in the 4Q24 TBR Cloud Ecosystem Report, “In many ways Google Cloud is staying the course with its partner strategy, focusing on scaling existing programs and incentives to help partners close larger deals more quickly. As part of its vision to foster the most ‘open AI ecosystem,’ Google Cloud has recently put a lot of focus on partner breadth and onboarding new partners that can help Google Cloud appeal to new audiences.

One example is with developers, and while there are over 1 million developers using GenAI tools, such as Vertex AI on GCP, Google Cloud aims to follow in AWS’ footsteps, boosting developer mindshare and delivering more seamless experiences. As such, Google Cloud has been delivering integrations with platforms like GitHub, which in 4Q24 announced support for Google’s latest Gemini models.

The other big priority for Google Cloud is around Marketplace. Though we often put AWS in a category of its own when it comes to marketplaces, with essentially all AWS’ top 1,000 customers having at least one active subscription, it is clear these platforms are where customers are buying their cloud software. As such, Google Cloud has been scaling the Marketplace with Private Offers, allowing resellers to deliver ISV solutions on GCP, and Google Cloud continues to cite momentum from partners co-selling Marketplace solutions alongside GCP. That said, it is clear Google Cloud wants its partners to continue to move away from traditional resell, toward value-added services, and Google Cloud maintains its commitment to driving 100% partner attach on all services deals.”

Pivoting from a two-dimensional foundation to a multiparty ecosystem play will test NTT DATA’s ability to manage trust

NTT DATA understands the need to pivot toward outcome-based services sales. Although it is easier said than done, the company has an opportunity to deliver value to clients provided it relies more on its alliance partners and continues to stick to its core expertise. Additionally, it will be essential for NTT DATA to invest in a partner framework that helps it address the following questions, which TBR outlined in the special report, Top Predictions for Ecosystems & Alliances:

Can your alliance partners tell your clients what makes you special?

Do your alliance partners’ sales teams know what value you bring to the ecosystem?

Are you sure you placed your strategic ecosystem bets on alliance partners that are well positioned for the next growth wave?

Are your competitors gaining ground with your common alliance partners through sales programs, go-to-market motions and training that you are not doing?

Learn how the strategic shift to ecosystem intelligence will impact your business in 2025.

Download TBR’s 2025 Ecosystem & Alliances Predictions special report today!

According to our Ecosystem Intelligence research, no single vendor has mastered the answers to all of these questions. NTT DATA is not new to managing alliance partnerships, as evidenced by its long-standing relationships with Microsoft and SAP. For example, the company touts $2.5-plus billion worth of SAP services business backed by more than 22,000 SAP-trained professionals. As outlined in TBR’s October 2024 SAP, Oracle and Workday Ecosystem Report, the size of its SAP practice places NTT DATA in a close race with EY and Tata Consultancy Services and above Capgemini, Cognizant, DXC Technology, Infosys and PwC.

Moving forward, NTT DATA’s success will also depend on the company’s ability to use a multiparty ecosystem lens and bring parties together. We believe an element of NTT DATA’s success with SAP is its ability to take a three-way approach with Microsoft and SAP to drive more targeted conversations. NTT DATA’s opportunity around Google Cloud will require a similar blueprint. Given Google Cloud’s push in data, AI and security, NTT DATA needs to think strategically about how to bring the likes of ISVs to the table that can help fill in that gap.

https://tbri.com/wp-content/uploads/2025/02/concept-of-teamwork-and-partnership_alphaspirit_getty-images-pro.png10801080Bozhidar Hristov, Principal Analysthttps://tbri.com/wp-content/uploads/2021/09/TBR-Insight-Center-Logo.pngBozhidar Hristov, Principal Analyst2025-02-08 12:04:212025-02-10 12:24:05GenAI-related Workload Opportunities Compel NTT DATA to Deepen Ecosystem Relationships

TBR attended two virtual Snowflake events in January, AI + Data Predictions 2025: How Operationalizing AI Will Drive Technical Advances and Leadership Challenges on Jan. 16, and Snowflake GenAI Day on Jan. 22. During the events we heard from Snowflake leaders, including Chase Ginther, principal architect AI/ML, and Caleb Baechtold, principal AI architect, Applied Field Engineering. These discussions, coupled with keynote speakers, breakout sessions, and TBR’s ongoing analysis of Snowflake’s strategy, underscore the company’s ongoing transformation from a data warehouse innovator to a leader in integrated data and AI platforms.

Snowflake in transition: Scaling AI through a data-first approach

Snowflake’s AI strategy is centered on a data-first approach that leverages the company’s data management strengths to drive development of advanced AI capabilities. Three key aspects of Snowflake’s strategy help it stand out in a highly competitive data and AI platform market.

First, the company is leveraging its origins as a data warehouse provider to offer a fully integrated data and AI platform. By prioritizing the management of structured and unstructured data, Snowflake enables AI-driven analytics, machine learning (ML) workflows and advanced processing within a unified ecosystem. Second, Snowflake is using advanced technologies to scale its AI capabilities, including GPUs to accelerate ML workloads; Snowflake Container Services (SCS) for efficient model deployment; and Snowpark, which enables seamless AI development using SQL, Python and Java. Third, Snowflake is enhancing its ecosystem through open-source AI collaborations via Cortex, integrating models from Meta, Hugging Face and Mistral to power natural language processing, predictive analytics and automation — all within a secure, data-centric framework. By prioritizing data as a foundation for AI, Snowflake enables efficient scaling while ensuring security, performance and governance within its ecosystem.

During the Snowflake events, TBR observed that customer demand for scalable, governed and actionable data remains a key driver of Snowflake’s evolution. The company’s ability to manage and harmonize disparate data types was repeatedly emphasized. For example, Ginther highlighted Nissan’s success in using Snowflake to analyze millions of customer profiles across multiple markets. This initiative showcased Snowflake’s ability to address complex, large-scale data challenges while delivering actionable insights for decision making.

Find out how generative AI (GenAI) will impact IT services, cloud vendors, the federal IT services market, IT infrastructure vendors and more in 2025.

Download TBR’s 2025 GenAI Predictions special report today!

Snowflake’s scalability is not just about performance; it also plays a critical role in empowering AI adoption through a favorable cost-to-value alignment. The platform’s pay-as-you-go pricing model adjusts to the dynamic demands of AI applications, particularly for resource-heavy use cases such as generative AI (GenAI) and predictive modeling. This flexible model enables organizations to efficiently grow their AI workloads and lowers the barrier to implement advanced AI solutions.

During Snowflake GenAI Day, the company showcased GenAI’s vast potential beyond traditional applications like chatbots and content generation. For example, Snowflake partner Sigma Computing demonstrated how Snowflake transformed raw Salesforce data into actionable insights. The AI-driven analytics not only improved decision making for Sigma’s business leaders but also reduced the time spent on manual data preparation, unlocking faster, more informed outcomes.

However, as enterprises scale their GenAI applications, they face challenges related to data bias, IP risks and ethical AI. To build trust with customers, vendors must design their AI solutions with governance, fairness and transparency in mind to ensure responsible AI deployment. Customers need to implement strong data governance practices that carefully monitor data to avoid perpetuating inaccurate or discriminatory outcomes.

Golden datasets and the future of AI development

One emerging trend highlighted during Snowflake GenAI Day was golden datasets — curated collections of structured and unstructured data optimized for GenAI use cases. These datasets, when enriched by Snowflake’s platform, empower organizations to drive more accurate and impactful AI outcomes. Moreover, Snowflake’s focus on text-to-language prompts, which simplify data interactions by reducing reliance on complex SQL queries, demonstrate its commitment to improving user experiences. Using Snowflake’s Universal Search offering, customers can identify datasets in their accounts based on data quality and usage within their workflows to create optimized — or golden — datasets. Universal Search ensures that users — regardless of their level of technical expertise — can effectively leverage Snowflake’s capabilities for AI development, analytics and decision making. However, building and maintaining golden datasets pose significant challenges. For many organizations, curating and cleaning data at scale require advanced governance frameworks and skilled teams to ensure data quality, relevance and accuracy. Organizations that lack these capabilities may struggle to derive meaningful insights from their AI models. Additionally, errors or inconsistencies in golden datasets can lead to biased outcomes, undermining trust in AI-driven decision making.

Simplifying user interactions

Another topic highlighted during the GenAI Day event was Snowflake’s focus on improving user accessibility. By incorporating text-to-language prompts into its data and AI platform, Snowflake has reduced the technical barrier for users who may lack expertise in SQL or other programming languages. This feature ensures that nontechnical users can interact with the platform effectively, making data-driven insights accessible across diverse teams.

Predictions for 2025: From experimentation to enterprise-grade AI

During the AI + Data Predictions 2025 event, Snowflake forecast a significant shift in AI adoption as enterprises transition from experimental pilots to fully realized, enterprise-grade AI solutions throughout 2025. However, TBR’s 2H24 Cloud Infrastructure & Platforms Customer Research survey results suggest that the adoption of GenAI solutions may progress more slowly than expected in 2025, primarily due to cost constraints and a lack of technical expertise with the emerging technology. Despite these challenges, Snowflake anticipates AI adoption will be driven by AI observability, as businesses increasingly need to prioritize ROI measurement, deployment reliability and regulatory compliance.

During the presentation, speakers discussed how Snowflake’s key AI advancements such as embedding models to enhance the performance of large language models, including GPT models, are enabling task-specific customizations, improving multilingual capabilities and optimizing overall model performance. Snowflake’s platform supports these efforts with containerized runtimes like Snowflake Notebooks and Snowflake Container Services (SCS), which provide scalable and efficient tools for AI development. Baechtold emphasized the critical role of robust datasets in supporting both GenAI and traditional ML models. Snowflake’s platform addresses key challenges, such as data security, governance and accessibility, ensuring enterprises can confidently deploy AI solutions across industries ranging from healthcare to manufacturing.

Deep dive into generative AI’s impact on the cloud market in 2025 in the below TBR Insights Live session

Security, governance and containerization: Building trust in AI

Throughout both events, security and governance emerged as central themes in Snowflake’s AI strategy. As enterprises increasingly integrate multiple platforms and environments, the risk of data breaches and compliance violations grows. Snowflake’s approach to governance includes developing best practices around securing cloud configurations, authenticating model access, and monitoring runtime environments to ensure its AI solutions are scalable, secure and compliant with evolving regulations. For example, OM1’s use of Snowflake demonstrated how containerized systems streamline governance processes and enhance scalability and efficiency. By leveraging these systems, Snowflake ensures that clients can deploy AI solutions with confidence, knowing their data and models are protected.

Despite Snowflake’s efforts, managing security and governance at scale is an ongoing challenge. Customers operating in highly regulated sectors, such as finance or healthcare, may require additional customizations to ensure they comply with stringent regulatory requirements. Additionally, scaling governance frameworks to accommodate rapidly evolving AI use cases could stretch Snowflake’s platform and resources. Providing consistent, enterprise-grade support while maintaining innovation will be essential for Snowflake to navigate these challenges.

Snowflake’s road map: Scaling innovation while meeting enterprise needs

Looking ahead, Snowflake will continue to focus on expanding its integrated data and AI platform while maintaining its core pillars of scalability, flexibility and observability. The company’s ability to bridge the gap between structured and unstructured data — combined with its investments in user experience, embedding models and AI observability —will place it among the leaders in the next wave of AI innovation.

However, Snowflake’s success will depend on its ability to balance innovation with governance, ensuring enterprises can address their unique data challenges while meeting compliance requirements. By focusing on empowering users, streamlining AI deployments and scaling advanced technologies, Snowflake will be well positioned to meet the demands of a rapidly evolving market.

Conclusion

Snowflake’s evolution reflects its commitment to advancing AI through a data-first approach. By addressing the complexities of modern data ecosystems and aligning its platform with emerging AI trends, Snowflake has established itself as a key player in the AI landscape. This strategic focus not only drives digital transformation but also shapes the competitive dynamics of the market, impacting partners, competitors and technology providers. The company has expanded its GenAI capabilities by integrating open-source models such as those from Hugging Face and Meta, enabling customers to deploy and customize AI models more easily.

Snowflake also emphasizes AI observability, providing businesses with tools to track performance, optimize outcomes and ensure ROI, while mitigating model drift. Its governance framework ensures regulatory compliance, safeguarding AI data and models across industries. Snowflake’s efforts to simplify the user experience and make AI more accessible to nontechnical users align with new industry standards. By lowering technical barriers, Snowflake is enabling a broader range of businesses to leverage AI and encouraging the market to innovate toward more user-friendly solutions. However, Snowflake faces challenges in integrating diverse data environments and maintaining data quality at scale. The need for significant infrastructure investments, such as GPUs, may also become a hurdle as AI adoption expands.

As GenAI and AI observability evolve, Snowflake’s integrated platform is positioned to support partners and stakeholders in navigating the next phase of industry transformation. By offering scalable and secure AI workflows, Snowflake is helping them tackle the challenges of adopting AI at scale across industries. TBR will continue monitoring Snowflake’s progress and its influence on AI-driven business strategies across sectors.

https://tbri.com/wp-content/uploads/2025/02/data-analysis_tadamichi_getty-images-signature.png10801080Gunnar Tache, Research Analysthttps://tbri.com/wp-content/uploads/2021/09/TBR-Insight-Center-Logo.pngGunnar Tache, Research Analyst2025-02-07 10:48:002025-02-10 12:23:16Snowflake’s AI Evolution: Scaling Innovation with a Data-first Strategy

Fujitsu Kozuchi’s wider understanding of business operations provides Fujitsu with an advantage around AI

Fujitsu launched Fujitsu Kozuchi, its AI platform that provides cloud-based AI services including generative AI (GenAI), predictive analytics, text, AI trust, experience AI, vision and automated machine learning (ML). These seven areas enable Fujitsu to address a wide range of business process needs. Since the launch of Fujitsu Kozuchi in August 2023, Fujitsu has continued to invest in the platform to add new services. For example, during 3Q24 Fujitsu expanded Fujitsu Kozuchi AI to include an AI agent that supports high-level tasks. As a result, Fujitsu is better equipped to provide advice and support related to users’ profitability challenges. In December Fujitsu added multi-AI agent security technology to protect digital and AI environments.

According to TBR’s November 2024 Digital Transformation: Voice of the Customer Research, “Buyers have become more tech savvy in recent years due in part to cloud adoption, and there is widespread understanding that they need GenAI. It is up to the vendors to make sure the technology lives up to the hype. Vendors have some time to iron out how to best demonstrate ROI, as only one-quarter of respondents quantitatively measure the effectiveness of the technology and 60% still apply only soft KPIs.”

Fujitsu’s investments in Fujitsu Kozuchi have equipped the company well to appeal to clients’ needs around the technology, providing opportunities to supply analytics with associated text, vision and trust in support of business operations. While AI technology evolves rapidly to include new capabilities, Fujitsu’s approach to developing the platform and leveraging partners and internal capabilities gives it an advantage in offering a wider set of services. Fujitsu’s industry expertise drives additional value for clients, helping them address key pain points and extract insights from their business operations. Despite the company’s geographical challenges, the development of Fujitsu Kozuchi and use of partners for portfolio development will enable Fujitsu to compete with peers and capture new clients in Europe and APAC.

Find out what’s in store for IT services vendors and consultancies in 2025 in terms of strategy consulting, generative AI (GenAI) and ecosystem intelligence.

Download TBR’s 2025 Digital Transformation Predictions special report today!

Partnerships enhance Fujitsu’s positioning around operational transformation projects

Revenue in Fujitsu’s services business fell an estimated 0.2% in local currency (down 3.2% in USD) to ¥713 billion ($4.7 billion). Continued demand for digital transformation projects and IT modernization services, particularly in Japan, was offset by offloading underperforming businesses. Fujitsu’s investments around Fujitsu Uvance, which is underpinning transformation projects, will help improve the company’s trajectory. Grounding its transformation projects in sustainable solutions that aim to address societal challenges aligns with clients’ needs and advanced technologies. The company’s enhanced delivery network improves operations outside of Japan, enabling Fujitsu to engage with new regional clients. Moving through 2025, Fujitsu will continue to accelerate Fujitsu Uvance, bringing in new capabilities to strengthen its value for clients and regional connections.

According to TBR’s 3Q24 IT Services Vendor Benchmark, “IT services vendors are working with partners to provide smoother, less disruptive adoption of new technology, enabling clients to improve their cost structures and benefit from operational efficiencies during ongoing macroeconomic uncertainty. Vendors and their partners are combining professional services, technology and industry expertise with new capabilities to meet client needs and create new revenue streams.”

Fujitsu continued to leverage its partner ecosystem, extending its existing relationships with key partners such as Microsoft, SAP and Amazon Web Services (AWS). Through the partnerships, Fujitsu enhances its position to deliver on vendor needs around cost structure and operational efficiencies. For example, with AWS, Fujitsu incorporated Fujitsu Uvance offerings with AWS’ cloud services and architecture to help integrate sustainability and address societal issues within digital transformation projects.

Under the partnership expansion, Fujitsu will train an additional 5,000 engineers to further accelerate digital transformation with new offerings and provide tailored services within cloud migrations. Fujitsu also renewed its partnership with SAP Fioneer following similar initiatives with an insurance industry focus. For instance, the two will collaborate on a cloud platform that supports core insurance services and business practices.

TBR will continue to report on Fujitsu’s increasing roles in the AI and consulting space. For access to upcoming data and analysis on Fujitsu’s strategy and performance, start your Insight Center™ free trial today.

https://tbri.com/wp-content/uploads/2025/02/5g-and-ai-technology_tony-studio_getty-images-signature.png10801080Kelly Lesiczka, Senior Analysthttps://tbri.com/wp-content/uploads/2021/09/TBR-Insight-Center-Logo.pngKelly Lesiczka, Senior Analyst2025-02-06 12:07:202025-02-10 12:12:03Fujitsu Expands Kozuchi AI Platform and Strengthens Partnerships to Drive Digital Transformation

Atos showcases strength in manufacturing industry specialization

Although it is an understatement to say Atos has struggled with its financial performance in recent years, the new year gives TBR analysts a chance to look for signs of change or markers indicating that Atos’ strategic decisions, investments and leadership adjustments have put the company on the path to sustained and profitable revenue growth in the coming years. We are paying close attention to Atos’ enhanced and deepened partnerships with technology companies, its major multiyear deal signings, and the use cases Atos’ two business lines — Eviden and Tech Foundations — tout as indications of what is working well and where they are gaining additional traction (and traction equals growth).

Along with the usual digital security solutions, cloud migrations, platforms and advanced computing implementations, one recent use case stood out, surprisingly not only for what Eviden did but also for what the organization positioned its client to do in the future. As part of a five-year engagement, Eviden helped Spanish train manufacturer Talgo develop what Eviden called a “state-of-the-art fleet monitoring system” that can ingest and process massive volumes of data, bring information and insights to train maintenance engineers, and “achieve architectural flexibility and scalability to incorporate modern train series without additional development efforts.” While the first few elements should be considered core capabilities of any modern, AI-enabled, and purpose-built system, the last one addresses a customer sentiment we have been hearing relentlessly for the last 18 months: Make my current technology work better without additional investment in even more new technology.

But that is not what jumped out at TBR as something special and a marker of potentially good things to come.

Reselling the TSMART solution creates new revenue streams for Talgo

Eviden’s work with Talgo produced the fleet monitoring system Talgo SMART Maintenance (TSMART). In recent years TSMART has been improved with capabilities such as predictive maintenance and visualizations. So far, so good, and so much like most others.

There is a significant difference, though, as Eviden noted in the press release: “Long an aspiration of smart manufacturing, the ability to create value-adding services from products is now Talgo’s reality. TSMART can be enhanced with product packaging/branding to be offered as a service to third parties. Talgo can easily extend the TSMART system to new train series or offer it to customers as a service. Its customizable interfaces include options for company branding and user personalization as well as new train configurations.”

Eviden helped create more than just an asset for Talgo to use internally and benefit from increased productivity, operational safety and fleet reliability. Now Talgo can expand its offerings with its own clients, develop a new business model, create new revenue streams, and, likely, greatly enhance its stickiness and position across its ecosystem. Not every IT services engagement leads to a client creating a new business opportunity, but this one did.

Now, can Eviden recreate the success of TSMART with other clients? Can this become a calling card for Eviden, an example of what can separate the organization from peers?

Certainly not with every client and every engagement — routine designing and building of systems are just that, routine — but if Eviden brings the mindset behind TSMART into opportunities, particularly with long-standing clients in the manufacturing and energy industries, TBR anticipates a quicker return to revenue growth for Eviden, which will support Atos’ overall financial performance.

Atos has established expertise around delivering predictive maintenance solutions and is applying its skills across industries. The company is working with multiple clients in the theme park and attractions industry, utilizing data and AI as well as edge server technologies to reduce the downtime of rides and improve customer satisfaction. For example, in 2020 Atos won a deal with the Triple Five Group’s American Dream entertainment complex to provide predictive maintenance utilizing data analytics and AI solutions as well as BullSequana Edge servers to collect and store data from ride sensors and detect issues through real-time analytics at the edge.

In covering Atos and its two business lines, Eviden and Tech Foundations, TBR publishes a quarterly Atos report and a semiannual Atos Cloud report. TBR also includes the company in our quarterly IT Services Vendor Benchmark, AI and GenAI Market Landscape, and various ecosystem intelligence and digital transformation reports, as warranted by Atos’ investments and activities in those areas. Access all of this research and more with your Insight Center™ free trial. Sign up today!

https://tbri.com/wp-content/uploads/2025/02/products-moving-on-production-line_simonkr_getty-images-signature.png10801080Elitsa Bakalova, Senior Analysthttps://tbri.com/wp-content/uploads/2021/09/TBR-Insight-Center-Logo.pngElitsa Bakalova, Senior Analyst2025-02-05 12:13:082025-02-10 12:18:28New Solutions Drive New Revenue Streams for Atos’ Manufacturing Clients

When the Carlyle Group acquired ManTech for $4.2 billion in September 2022, TBR questioned how the federal IT vendor would be restructured. One month later, when Matt Tait succeeded Kevin Phillips as president and CEO of ManTech, he quickly signaled that the needs of the defense and intelligence markets would remain central to the company’s vision.

Since then, Tait has been steadily funneling resources into five technology focus areas: Analytics, Automation and AI (A3); Cognitive Cyber for Physical and Digital Platforms (Cognitive Cyber); Data at the Edge (D@tE); Intelligent Systems Engineering (ISE); and Mission & Enterprise IT (M/EIT). Rather than focusing on harnessing a single emerging technology, ManTech has explored how these technologies played off one another and how to leverage their synergies. In doing so, ManTech’s efforts aligned with the Biden administration’s spending priorities and the company captured lucrative awards like the U.S. Army’s $622 million Technology Insertion Transformation Unified Services (TITUS) task order.

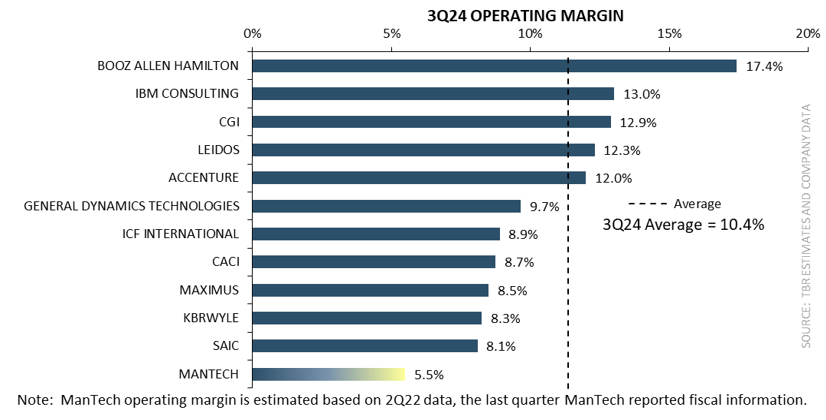

While ManTech’s ongoing strategy appears to align with the Trump administration’s interests, the company will need to increasingly leverage its partner network to close the capabilities gap between it and Tier 1 peers like Leidos and Booz Allen Hamilton (BAH).

ManTech is increasingly collaborating with partners …

ManTech had been largely inactive on the alliance front since strengthening its ties with Amazon Web Services (AWS), Google and Red Hat in 2021, but the Carlyle Group’s takeover in 2022 has prompted ManTech to recently take steps in that direction.

For example, ManTech partnered with Marque Ventures in 2Q24 to find companies in the national security space making inroads with emerging technologies and incorporate them into ManTech’s offering ecosystem. ManTech also announced that Trust Stamp’s AI-powered Irreversibly Transformed Identity Token would be integrated with ManTech’s offerings as part of a teaming agreement the two reached during the first half of 2024.

… but so are its Tier 1 peers

Although ManTech has been accelerating its alliance formation and expansion activity, the company continues to lag its biggest federal systems integrator peers. Accenture Federal Service, BAH, CACI, SAIC and Leidos maintain extensive and well-run alliance ecosystems in the federal IT market, and each has been very active in forging new alliances or expanding existing collaborations (particularly in cloud computing and AI). Several of these vendors, such as BAH through its venture capital arm Booz Allen Ventures, have also made substantial venture capital investments in smaller, AI- and cloud-focused peers or partners with key adjacent technologies.

Leidos, the largest federal systems integrator by revenue, with over $14.2 billion in technology and technology-related sales in 2024, has a broad network of solutions and strategic partners. Leidos pursues partnerships across a wide swath of players, from Microsoft to NetApp. In most engagements, Leidos acts as the principal systems integrator thanks to its market-leading scale and ability to design and deliver open-architecture-based data management, security and communications solutions across federal agencies’ IT infrastructures. Leidos and Microsoft expanded the scope of their partnership in cloud computing in 2023 and formed a strategic collaboration agreement with AWS in 1Q24, deepening the long-standing relationship between the partners. Historically, Leidos and AWS have been active in the defense and intelligence sectors, and the enhanced collaboration will focus on advancing multidomain operations for the Department of Defense (DOD) and Intelligence Community (IC).

Entering the consulting sphere

When Tait initially took charge of ManTech in fall 2022, he gave no indications as to whether he would seek financial backing from the Carlyle Group to bolster ManTech’s sputtering civilian business. Less than a year later, ManTech acquired Definitive Logic for an undisclosed amount.

While the acquisition has certainly expanded ManTech’s presence in the defense and intelligence markets, it has also created new opportunities for ManTech in the civilian market. By purchasing the 330-person firm, ManTech was able to significantly speed up its efforts to incorporate consulting into its go-to-market strategy.

Since 2023, ManTech has launched multiple consulting practices, such as the Google Workspace Practice, that are dedicated to helping agencies adopt emerging technologies. Through the Google Workspace Practice, ManTech and Google Public Sector have expanded their partnership and are hosting immersive workshops tailored to agencies and other prospects’ needs to demonstrate how generative AI and Google Workspace can enhance operational efficiency.

ManTech’s pivot into the consulting space may come as a surprise given the company’s history, but it aligns with the Carlyle Group’s priorities since purchasing ManTech. The private equity specialist has been fine-tuning ManTech to expand its addressable market size, build out a more diverse array of capabilities, and bring its margin performance more in line with that of its peers. Having ManTech expand beyond its traditional plug-and-play role and support all stages of a client’s journey addresses all of those goals and is why more vendors like General Dynamics Information Technology (GDIT) have also recently thrown their hats into the consulting ring.

ManTech has an advantage over GDIT in the consulting space because it is currently a private company and can take its time fine-tuning operations without facing the scrutiny of Wall Street. Consulting fundamentally comes down to people and permission, which can be difficult to build and/or acquire. Consulting also requires money and patience to be successful — things that are rarely rewarded when facing the never-ending 90-day clock of earnings.

What is next?

While private equity always has an exit strategy, it is unlikely that the Carlyle Group will take ManTech public or sell it to another company in the near future.

When the Carlyle Group first took over ManTech, the company was a margin laggard with organic revenue growth that paled in comparison to its peers in TBR’s Federal IT Services Benchmark. The Carlyle Group has had a positive impact on ManTech’s profitability by optimizing its headcount, making necessary divestitures and pivoting into the margin-friendly consulting business, but it will still take time to bring ManTech’s operating margin in line with vendors like CGI Federal.

Additionally, while ManTech is making inroads with its consulting business and earning seats on high-profile contract vehicles like the FBI’s Information Technology Supplies and Support Services 2nd Generation initiative (ITSSS-2) program, TBR believes that the company’s revenue growth continues to lag far behind that of Tier 1 peers like BAH and CACI. ManTech recently stood up civilian and defense-oriented advisory boards to better understand how it can gain traction across these markets, but it will be a while before these efforts yield results.

Similarly, bringing ManTech’s AI, analytics, automation, systems engineering and solutions to the scale that its competitors offer is also a longer-term goal. Given that the M&A market is becoming increasingly buyer-friendly, TBR anticipates that ManTech will leverage financial backing from the Carlyle Group to quickly strengthen these capabilities.

The Carlyle Group spent roughly two and a half years restructuring an already high-functioning BAH before cashing out. TBR believes the Carlyle Group will be patient with ManTech and ensure that the company is better positioned across the defense market as well as the civilian market by leveraging its technology focus areas and fostering margin growth to ensure long-term success. Once ManTech can generate predictable revenue and profit streams, TBR believes the Carlyle Group will cash out, but we do not expect this to occur until 2027 at the earliest.

https://tbri.com/wp-content/uploads/2025/02/green-ipo_oksanasazhnieva_canva-pro.png10801080James Wichert, Analysthttps://tbri.com/wp-content/uploads/2021/09/TBR-Insight-Center-Logo.pngJames Wichert, Analyst2025-02-04 10:06:402025-02-11 09:35:11As the Carlyle Group Continues to Fine-tune ManTech, Will We See It Go Public in 2025?

Federal IT spending remained robust throughout FFY24, and the market appears poised for another strong year in FFY25, even as CY25 begins with yet another continuing resolution

TBR projects weighted average year-to-year federal IT services revenue growth for the 11 companies featured in our Federal IT Services Benchmark will decelerate to between 8% and 8.5% in 4Q24, down from 9.3% in 3Q24. Additionally, we anticipate weighted average year-to-year revenue growth in the defense sector will fall to between 6.8% and 7.3% in 4Q24, while civilian revenue growth will remain between 10% and 10.5% in 4Q24.

Four leading federal systems integrators — Booz Allen Hamilton (BAH), CACI, Leidos and SAIC — as well as smaller federal IT peer KBRWyle elevated their respective revenue growth forecasts for their current fiscal year when tendering 3Q24 fiscal results; these results indicate the federal IT macro environment will remain mostly growth-friendly through FFY25.

The new federal fiscal year began with a continuing resolution (CR) that extended government funding until Dec. 20, when a subsequent CR was enacted to fund federal operations until March 14, 2025. Further CR extensions in federal fiscal year 2025 (FFY2025) would cause budget delays that could impede the ability of federal IT contractors to convert backlog into revenue, but most vendors expect revenue growth to remain on a solidly upward growth trajectory in FFY25.

The Fiscal Responsibility Act of 2023 (FRA) remains in effect, and the Biden administration’s FFY25 budget request aligns with the FRA’s spending caps. Federal IT spending priorities will remain largely unchanged in FFY25, with IT investment focused on enhancing national security (especially in the APAC region and to deter future Russian aggression in Ukraine), promoting the adoption of AI and generative AI (GenAI) technologies, modernizing and enhancing the security of federal technology infrastructures, and IT-enabling public health systems.

The Department of Defense (DOD) will be integrating six new naval vessels into its global IT networks while spending nearly $34 billion to enhance space-based capabilities and another $10 billion to enhance the security and interoperability of IT and weapons systems operating in the Indo-Pacific theater. The Pentagon will spend another $14.5 billion for overall cybersecurity activities in FFY25 while expanding outlays on analytics and AI and increasing investment in the ongoing Replicator initiative to deploy thousands of autonomous systems across multiple domains by FFY26 to counter the ever-growing threat from China.

Civilian agencies will continue increasing their cybersecurity spending in FFY25, with an additional $13 billion requested in FFY25 to fund new zero-trust and access management programs as well as initiatives to secure critical infrastructure and federal civilian supply chains. The budget of the Cybersecurity and Infrastructure Security Agency (CISA), the division of the Department of Homeland Security (DHS) charged with leading cybersecurity efforts across the federal market, will expand by over $100 million from FFY24 to FFY25 to reach $3 billion. Civilian agencies are also increasing AI-related investments to fund the development, testing, purchase and deployment of new AI and GenAI technologies, as well as to expand their AI workforces.

Federal agencies must master AI from both a technological and a responsible use standpoint, prior to the inevitable adoption of GenAI. The most basic, fundamental distinction between AI and GenAI is that AI is good at analyzing existing content while GenAI generates new content. Much foundational modernization work is still needed across the federal IT environment to accommodate digital technologies like cloud, AI and GenAI, ensuring continued (albeit slower) federal IT growth in FFY25 and beyond.

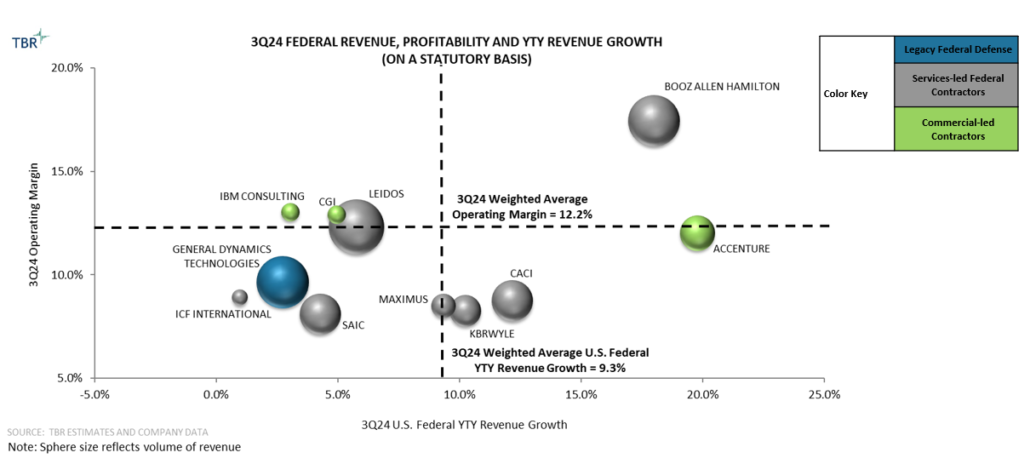

Expansion accelerated in the federal IT market in 3Q24 as renewed M&A activity by several federal IT vendors augmented strong, stable demand for digitally based IT modernization

Statutory year-to-year revenue growth for the 11 TBR-benchmarked vendors in the U.S. federal market on a weighted average basis rose 100 basis points sequentially, increasing from 8.3% in 2Q24 to 9.3% in 3Q24. Acquisitions by Accenture Federal Services (Cognosante), BAH (PAR Government Systems Corporation [PGSC]), CACI (Quadrint in 1Q24 and Azure Summit Technologies [AST] in 3Q24), CGI Federal (Aeyon), General Dynamics Technologies (Iron EagleX) and KBRWyle (LinQuest) generated an inorganic tailwind to overall market growth of roughly 180 basis points in 3Q24.

Federal IT executives (e.g., CACI CEO John Mengucci) have indicated that the M&A market became more buyer-friendly during 2024, prompting several benchmarked vendors to leverage acquisitions to address portfolio gaps in multiple areas, including digital transformation (DT) and emerging technologies for classified defense and intelligence operations.

Vendors have been acquiring, and will continue to hunt for, smaller peers with scalable cloud and digital modernization capabilities as well as deep existing (and likely cloud-related) relationships with federal agencies. Underpinning inorganic market growth is enduring robust demand for digitally transformative technologies in AI, cloud, analytics and data science, as well as the continued need to upgrade baseline IT infrastructures across the federal sector to accommodate digital modernization.

KBRWyle’s federal revenue rose 10.2% year-to-year in 3Q24 as LinQuest was acquired and demand mounted for all the offerings within Government Solutions business units. KBR’s leadership team increased its guidance for the company’s revenue, adjusted EBITDA and adjusted earnings per share (EPS) during the 3Q24 earnings call due in part to Government Solutions’ strong performance and the purchase of LinQuest creating more opportunities with DOD agencies.

Inorganic growth is again boosting CACI’s top-line growth after the company made three acquisitions between 2Q24 and early 4Q24. CACI’s acquisition of AST in 3Q24 contributed between 70 and 80 basis points of inorganic growth during the quarter and is expected to add between $440 million and $450 million to the company’s sales in its FY25.

BAH’s revenue rose 18% year-to-year in 3Q24, driving the firm’s total sales past $3 billion for the first time. BAH’s June acquisition of PGSC began to contribute inorganic revenue in 3Q24, and we estimate BAH’s organic year-to-year growth was 17.7% in 3Q24, with PGSC contributing between 20 and 30 basis points of inorganic growth.

Civil and defense agencies drive double-digit IT growth through cybersecurity, health IT and AI investments

Civil agencies continue to aggressively invest in cybersecurity, health IT and Agile-based software systems, leading to sustained double-digit civil sector IT spending growth

Weighted average growth in the civilian sector accelerated 80 basis points sequentially, rising from 9.6% in 2Q24 to 10.4% in 3Q24. Vendors including BAH and Leidos have posted multiple quarters of double-digit growth in their respective civil units as of 3Q24, with robust rates of growth expected to persist well into 2025. Sector growth was sustained at or near 10% throughout FFY24 as demand among civil agencies remains robust for comprehensive zero-trust and cyber incident support solutions, particularly by DHS, the Department of Health and Human Services (HHS), the IRS and NASA.

Attracting and retaining cybersecurity talent also remain top priorities for nearly all civilian agencies, which are tapping vendors like Accenture Federal Services (AFS), BAH and Deloitte Federal for human resource advisory services. NASA launched an eight-year, $2 billion program, NASA Consolidated Applications and Platform Services (NCAPS), during 3Q24 to develop and deploy Agile-based software for over 200 IT systems, with vendors including CACI among the primary awardees. Health IT is generating new revenue and profit streams for the benchmarked vendors, and agencies including the HHS (and its subagencies, the Centers for Medicare & Medicaid Services, the Center for Disease Control and Prevention, and the National Institutes of Health) are seeking agencywide AI and analytics adoption services. The top five benchmarked vendors in year-to-year civilian sector revenue growth in 3Q24 were AFS (25%), BAH (16.1%), SAIC (10.8%), Maximus (9.3%) and CACI (7.9%).

Defense and intelligence agencies expanded spending on IT modernization, global integration of defense networks, and AI-enabling intelligence collection and analysis solutions in 3Q24

Weighted average expansion in the defense sector rose 110 basis points sequentially, from 7.5% in 2Q24 to 8.6% in 3Q24. BAH and CACI maintained double-digit expansion in their respective defense sales in 3Q24, while Leidos and GDT posted midsingle-digit top-line defense growth in the quarter. The DOD awarded billions of dollars in net-new programs while several benchmarked competitors also secured key recompetes with defense agencies. The DOD’s European Command has aggressively expanded its activities (particularly with BAH) as the war in Ukraine grinds on, while globally, the Pentagon continues prioritizing the adoption of AI, analytics, big data and cloud technologies to facilitate and accelerate real-time decision making for military commands.

The DOD is also expanding activities in APAC, investing in advanced intelligence and combat-related technologies to deter Chinese aggression. The U.S. Air Force is accelerating spend on the Collaborative Combat Aircraft program while the DOD’s Combined Joint All Domain Command and Control (CJADC2) initiative to achieve IT infrastructure interoperability across all military branches and with defense agencies of U.S. allies continues to spool up. Project volumes also expanded on several marquee defense IT programs, including Sentinel (modernizing C5ISR [Command, Control, Communications, Computers, Cyber, Intelligence, Surveillance and Reconnaissance] systems across the DOD) and the $11 billion Defense Enclave Services program.

IT investment patterns in the intelligence community continue slowly stabilizing as intelligence agencies invest in intelligence analysis services and solutions and AI-based technologies to collate and ingest intelligence data. The top five benchmarked vendors in year-to-year defense sector revenue growth in 3Q24 were BAH (19.1%), CACI (13.5%), KBRWyle (12.4%), Leidos (4.4%) and AFS (3.9%).

Follow federal IT services performance throughout 2025 with data and analysis in TBR Insight Center. Start your free trial today.

https://tbri.com/wp-content/uploads/2024/12/government-debt-ceiling_douglas-rissing_getty-images_canva-pro.png10801080John Caucis, Senior Analysthttps://tbri.com/wp-content/uploads/2021/09/TBR-Insight-Center-Logo.pngJohn Caucis, Senior Analyst2025-02-04 08:44:482025-01-31 13:45:53Federal IT Spending Poised for Another Strong Year in Fiscal 2025

We may request cookies to be set on your device. We use cookies to let us know when you visit our websites, how you interact with us, to enrich your user experience, and to customize your relationship with our website.

Click on the different category headings to find out more. You can also change some of your preferences. Note that blocking some types of cookies may impact your experience on our websites and the services we are able to offer.

Essential Website Cookies

These cookies are strictly necessary to provide you with services available through our website and to use some of its features.

Because these cookies are strictly necessary to deliver the website, refusing them will have impact how our site functions. You always can block or delete cookies by changing your browser settings and force blocking all cookies on this website. But this will always prompt you to accept/refuse cookies when revisiting our site.

We fully respect if you want to refuse cookies but to avoid asking you again and again kindly allow us to store a cookie for that. You are free to opt out any time or opt in for other cookies to get a better experience. If you refuse cookies we will remove all set cookies in our domain.

We provide you with a list of stored cookies on your computer in our domain so you can check what we stored. Due to security reasons we are not able to show or modify cookies from other domains. You can check these in your browser security settings.

Other external services

We also use different external services like Google Webfonts, Google Maps, and external Video providers. Since these providers may collect personal data like your IP address we allow you to block them here. Please be aware that this might heavily reduce the functionality and appearance of our site. Changes will take effect once you reload the page.

Google Webfont Settings:

Google Map Settings:

Google reCaptcha Settings:

Vimeo and Youtube video embeds:

Privacy Policy

You can read about our cookies and privacy settings in detail on our Privacy Policy Page.