Moving from Use Cases to AI Value: Infosys Focuses on Portfolio, Partner and Talent Readiness

U.S. Analyst and Advisor Meet 2026, New York City, March 5, 2026 — Infosys hosted industry analysts and advisers for an afternoon in the newly branded Infosys Theater within Madison Square Garden. Using client stories amplified through technology partner support to reinforce Infosys’ role in the IT services, cloud and enterprise AI market, company executives consistently noted that enterprise AI success depends on combining strong data foundations, responsible governance, talent transformation, domain-specific use cases and partner-led execution, which can help turn AI from isolated experimentation into measurable business value.

Americas’ scale and market maturity present an opportunity for Infosys to treat AI as a horizontal capability rather than an ad hoc solution

Similar to previous meetings, the event began with an update on the company’s strategy and performance in the Americas region. Anant Adya, EVP and head of Americas Delivery, led the presentation, highlighting key elements of the company’s success in the region, such as its hub-first strategy, including the addition of a hub in Costa Rica. Adya described the hubs as serving four roles: innovation, client cocreation, centers of excellence, and training and enablement. He specifically mentioned the hub in Hartford, Conn., which focuses on insurance and healthcare domain solutions and client prototyping, as well as a ServiceNow Center of Excellence, which focuses on onboarding and training local university students and other talent.

A key nuance in Adya’s presentation at last year’s event was Infosys’ positioning of AI and moving from the earlier pentagon-shaped strategy to a new hexagon-shaped strategy centered on AI. The message was that AI is no longer a horizontal add-on but is now meant to reshape the full services value chain. He emphasized that enterprise data readiness is the critical prerequisite, with cloud already assumed and data becoming the true launchpad for AI at scale. He used several client examples to illustrate the strategy in action: AI-infused managed services for a packaging company, AI-first manufacturing operations for a semiconductor client, AI-led SAP transformation for a utility, and AI-enabled wealth operations for a financial services firm. Across those examples, the focus was on measurable business outcomes like productivity, manufacturing uptime, revenue impact, and value creation, not just IT efficiency.

TBR appreciated these examples as we see them as a bridge into opportunities for Infosys to drive awareness of its broader capabilities and strengthen relationships among enterprises. We believe that pivoting from driving AI conversations centered on efficiency improvement to discussing business growth at scale will pressure-test Infosys’ commercial model readiness, especially as the former leads buyers to expect perpetual cost savings, thus pressuring Infosys’ margins, while the latter provides a pathway for increasing volume, delivered by fewer employees.

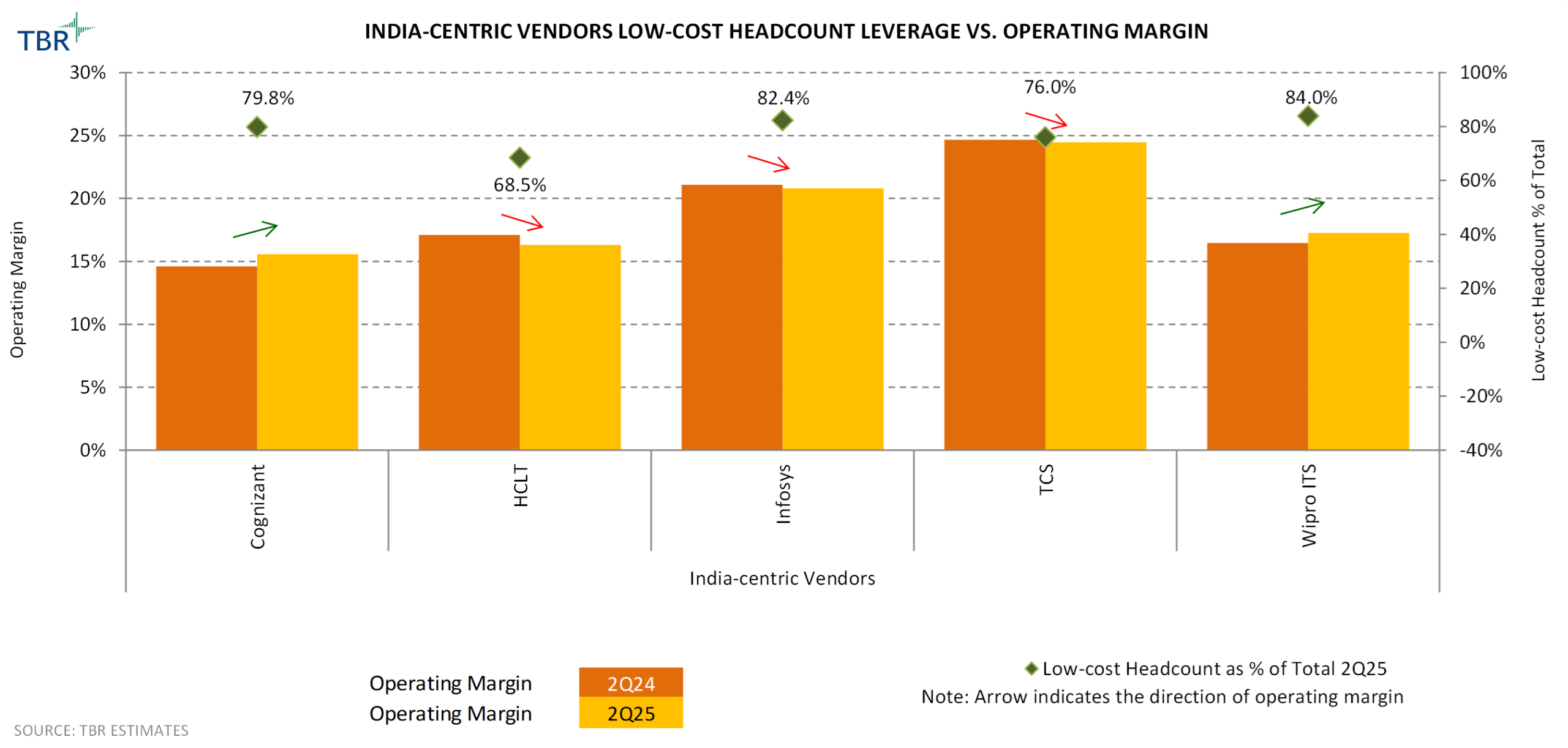

India-centric Vendors Low-cost Headcount vs. Operating Margin (Source: TBR)

Infosys has maintained an operating margin within its guided range of 20% to 22% for a few years, yet headcount growth began to rebound in 4Q25, at 4.2% year-to-year, following several quarters of decline. Additionally, grouping partners into strategic foundation partners, conventional core partners, and innovation-edge AI partners highlighted Infosys’ recognition of the value of the ecosystem and the importance of where each party plays. Aligning to core strengths from both a capability and a messaging perspective can help Infosys and partners demonstrate depth and strengthen trust with buyers who seek mutual accountability and understanding of go-to-market priorities.

Crystalizing AI talent strategy will provide Infosys with the necessary support to drive business value at scale

Following Adya’s strategy update, Ranjana Joshi, AVP and HR leader, Americas, discussed how Infosys is redesigning its workforce model for an AI-first services business. Although TBR has previously heard some of the details Joshi outlined, it was apparent that Infosys has crystallized what comes next in developing an AI-ready workforce. Infosys is building the talent strategy around three pillars: a new talent operating model, which she described as an “ambidextrous” model; a new career model; and a new talent development model.

According to Joshi, these pillars are set to help Infosys do two things at once: “augment the whole organization with AI while also building deeper engineering and domain expertise to deliver AI-first services.” Under its new “ambidextrous” approach, Infosys is changing how it hires. The company is shifting toward recruiting more specialized talent, including specialist programmers from U.S. campuses, alongside continued hiring of full-stack engineers and domain experts.

Additionally, Infosys continues to invest in internal bridge programs and hands-on sandbox-based development paths to ensure it develops the right-skilled bench. Meanwhile, career paths are being redesigned away from the traditional linear ladder. Instead of the old one-dimensional path from engineer to executive, Infosys has set up a Y-shaped career structure. One track is for the broad workforce that is AI-augmented, and the other is a specialist stream for people with deep engineering, domain and functional expertise. Further, the company is adding distinguished specialists in roles such as AI strategist and responsible AI engineer. These professionals are meant to act as catalysts who accelerate innovation and create specialist ecosystems around them.

Although these are important investments, especially as Infosys looks to build messaging centered on AI-readiness at scale, peers often cite numbers that suggest the majority of their workforce is AI-ready, challenging it to differentiate. Infosys’ opportunity lies in its ability to develop an AI-ready sales bench, especially as the technology forces it to act more like a software company than a traditional services company. We view Infosys’ investments in forward-deployed engineers (FDEs) as a bridge into an AI-ready sales force. Striking the right balance between pushing AI-first sales and managing relationships with ecosystem partners will be key, as going too far into selling tech could sour relationships with partners that try to do the same.

Helping clients scale, orchestrate and operationalize AI for business value will test Infosys’ commercial and operating model readiness

Throughout the rest of the afternoon, Infosys’ executives, clients and partners continued their efforts to separate hype from reality regarding scaling enterprise AI adoption. Compared to previous events, Infosys’ emphasis on domain-specific use cases amplified through panel discussions across financial services, energy, insurance, consumer packaged goods and life sciences strengthened the company’s message and AI strategy.

Joydeep Mukherjee, EVP and global head, Data & Analytics, Digital & Creative Services; and Srinivas Gopal, VP and Global Business Head – Data, Analytics & AI, noted that the market has moved beyond AI experimentation and is now demanding measurable enterprise value. Mukherjee’s core point was that most companies still struggle to scale AI because they are held back by weak strategy, fragmented data, governance gaps, integration challenges, and immaturity in their operating models. Scaling AI requires a coordinated blueprint spanning value discovery, operating model design, technology readiness, performance management, responsible AI and talent transformation.

Gopal built upon that point by showing what the next stage looks like in practice: agentic AI applied to real business processes, where enterprises use data products, intelligence layers and orchestrated agents to improve decision making, accelerate workflows and create business outcomes faster. Across both sessions, the message was that enterprise value does not come from isolated pilots or stand-alone agents but rather from combining strong data foundations, contextual business knowledge, governance and production-scale execution. This message also highlighted the breadth of Infosys’ capabilities in helping customers make that shift with Infosys Topaz as the orchestration layer.

In TBR’s 4Q25 Infosys report, we wrote: “Infosys’ recent cluster of GenAI [generative AI] announcements signals a deliberate pivot from AI-enabled services toward an agent-first delivery platform strategy, with Topaz Fabric positioned as the control plane. By pairing Fabric with hyperscaler-native capabilities like Amazon Q Developer for IT modernization and productivity, while embracing emerging AI software engineer tooling through Cognition’s Devin and scaling vertical agents such as its energy-operations solution on the Microsoft stack, Infosys is effectively building a multipartner operating model that can meet customers where they are without ceding the orchestration layer.

For competitors, differentiation is shifting from headcount, pricing and even domain expertise toward agent operational maturity, where productizing services compresses delivery timelines and forces a margin reset. For alliance partners, the upside (and risk) is that fabric-owning SIs become high-leverage distribution for platforms and models, while increasingly establishing the integration patterns, governance standards and customer experience — shifting partnerships from joint marketing to control of the runtime and commercial attach adds value.”

According to TBR’s December 2025 Digital Transformation: Voice of the Customer Research report, the market is signaling that vendors are getting better at packaging and surfacing IP, but monetization is still anchored to services constructs, not product economics, especially as automation and AI start to do a greater share of the work.

Against that backdrop, Infosys’ recent AI investments look like an attempt to bridge this gap rather than leap over it. The inflection point to watch is whether Infosys can translate its agent-first strategy into commercial pioneers that buyers can procure — clear SKUs, governance guarantees, and outcome and/or consumption mechanisms that do not simply relabel labor. If Infosys can prove repeatable productivity and quality gains and then price around outcomes with credible controls, it can move from AI-enabled services to a platform-led model that aligns with where buyers say they want vendors to go but have not consistently shifted toward yet in terms of their procurement behavior.

Alternatively, Infosys’ AI announcements can be interpreted as commercial positioning ahead of change. Topaz Fabric, agents and FDEs absolutely help industrialize delivery, but they also create a convenient story in which Infosys can claim platform-led differentiation while still monetizing primarily through large, multiyear services contracts. The recent launch of AI-enabled global capability center (GCC) framing, in particular, can be read in one of two ways: Either it is a structured route to platformizing captive operations, or it is a mechanism to lock in demand and defend wallet share by embedding Infosys’ tooling, processes and governance so deeply that switching becomes hard without changing the pricing model as much as the marketing implies. The near-term expectation is that Infosys will capture value the way the industry typically does during transitions: sell transformation rhetoric, deliver productivity gains, and then negotiate hard to keep most of the savings — or recycle those savings into scope expansion rather than price reductions.

Domain-aligned services backed by relentless and quality service execution will help Infosys sustain trust with key buyers

Across the panel discussions, speakers noted that most organizations have already experimented with pilots and proofs of concept. The real challenge now is turning those isolated efforts into repeatable, enterprisewide capabilities. Panelists described this as an execution problem as much as a technology challenge, requiring alignment across strategy, operating model, governance, data and talent.

Within a financial services discussion, banking was presented as one of the sectors most ready to use AI because it can improve both growth and efficiency while also supporting resilience and compliance. The insurance panel showed how AI is being applied in a regulated industry through underwriting, pricing, unstructured data extraction, faster service and operational efficiency. The insurance leaders repeatedly stressed that in the human-plus-AI equation, especially in specialty insurance, AI can speed intake and improve accuracy, but the knowledge and judgment of experts still matter for decision making and evaluating risk.

The energy discussion centered on the growing complexity of energy and commodity markets and the role Infosys wants to play in that transformation. Speakers described energy trading and risk management as a stabilizing force in volatile markets, especially as geopolitical disruption, AI-driven power demand and shifting wholesale-retail dynamics make forecasting and execution more difficult. Infosys’ acquisition of MRE Consulting, which featured prominently during the panel, will play a key role in strengthening trust with existing buyers and expanding the company’s addressable market opportunity across EMEA and APAC. Infosys’ Energy, Utilities, Resources and Services (EURS) vertical share of revenue has hovered around 13% to 14% of Infosys’ total sales. We believe MRE Consulting, along with future similar investments in the vertical, will help boost that share to between 16% and 17%, similar to how manufacturing grew from around 10% of Infosys’ total sales in 2020 when it signed its megadeal with Daimler to now hovering close to 17%.

Balancing steady services-enabled revenue growth with new product sales channels will test Infosys’ otherwise strong culture

Over the next 12 to 18 months, we will keep a close eye on whether Infosys can convert AI breadth into depth, which will be evidenced by higher attach rates of Topaz Fabric in large programs, clearer packaging and commercial models for GCC platformization, and consistent outcome metrics (not just activity metrics) tied to modernization, data readiness and workflow redesign.

Infosys has an opportunity to stand out from its peer group if it can make Fabric the default operating layer for agent delivery and use FDEs to accelerate time to value, creating durable differentiation versus peers, as many of them are still largely focused on tooling plus services. Key risks include execution complexity, partner dependence blurring differentiation, and value-capture pressure if Infosys is forced to compete on price, relinquishing the value of the productivity gains it gives clients. Additionally, the use of FDEs, even on a smaller scale than Infosys’ traditional labor arbitrage pyramid, can raise questions about the company’s use of a time-and-materials model versus agent-based wrapped pricing.

Further, accelerating revenue from value-based selling would bolster profitability but compel the company to recalibrate its staffing pyramid across legacy and new areas, pressure-testing attrition levels. Lastly, quick-hit wins within the agentic AI space could entice Infosys’ leadership to pursue a more aggressive product sales strategy, disrupting its ongoing success with traditional services deals. In an intense and rapidly changing competitive market for AI-enabled IT services solutions, Infosys has a fighting chance to stand out. And we think the company’s leadership and recent success will help Infosys separate from peers over the next few years

TBR will continue to cover Infosys across the IT services, ecosystems, cloud, and digital transformation spaces, including publishing quarterly reports that assess Infosys’ financial model, go-to-market strategy, and alliances and acquisitions strategies. For a comparison with Infosys’ peers and other IT services vendors, TBR includes Infosys in our quarterly IT Services Vendor Benchmark, our semiannual Global Delivery Benchmark and Cloud Ecosystem Report, and our annual Adobe and Salesforce Ecosystem Report, SAP, Oracle and Workday Ecosystem Report, and ServiceNow Ecosystem Report. Click here to learn more about accessing the data and analysis within these reports.