Technology Business Research, Inc.

Technology Business Research, Inc.Why are Deloitte’s, Accenture’s and TCS’ revenues per hyperscaler practice much higher than the benchmarked average?

Gimme 3 — Insight Interview with TBR’s Subject-matter Experts

In TBR’s new blog series, “Gimme 3 — Insight Interview with TBR’s Subject-matter Experts,” Principal Analyst Patrick M. Heffernan discusses our latest and most popular research with our analyst team.

This month Patrick chats with Principal Analyst Bozhidar Hristov about our latest cloud ecosystems research, including why Deloitte’s, Accenture’s and TCS’ revenues per hyperscaler practice are much higher than the benchmarked average.

Patrick: Why are Deloitte’s, Accenture’s and TCS’ revenues per hyperscaler practice much higher than the benchmarked average?

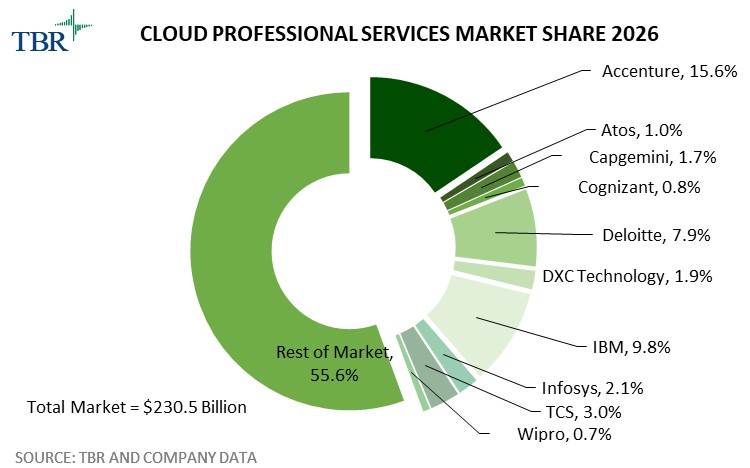

Boz: Deloitte’s, Accenture’s and Tata Consultancy Services’ (TCS) investments in cloud and overall IT services capabilities enabled each of them to drive conversations aligned to and/or enhanced by core value offerings. For example, Accenture has managed a close relationship with Microsoft since the launch of joint venture Avanade in 2000; Avanade evolved into Accenture Microsoft Business Group in 2019.

Acquisitions also bolstered Accenture’s scale, particularly around Amazon Web Services (AWS) and Google Cloud capabilities supporting the Accenture Cloud First agenda. Additionally, acquisitions help the company maintain a strong foothold in the market and trust with stakeholders as well as capitalize on its household name. In sum, Accenture has done everything it could, relentlessly.

In contrast, TCS has pursued a strictly organic strategy to build scale, relying on its low-cost execution offerings and investments in developing certified and skilled talent. Through distinct business units, TCS has also demonstrated commitment to all three hyperscalers — AWS, Microsoft Azure and Google Cloud Platform — enabling trust between TCS and hyperscaler partners.

Deloitte is a bit of an outlier, with the firm’s success largely rooted in its business compliance relationship and access to C-Suite decision makers, supported by ongoing investments in talent and portfolio offerings. Deloitte has built scale through both organic and inorganic means as the firm tries to balance investment priorities of individual member firms with globally run cloud initiatives.

Deloitte’s relationship with Microsoft is rather unorthodox as the firm audits the tech giant. However, Deloitte is able to circumvent these requirements while staying compliant by providing customer support rather than joint go-to-market efforts. We estimate Deloitte generated over $500 million in Microsoft Azure-related revenue in 2021. Deloitte also provides a use case for the remaining Big Four firms, which must also balance audit relationships with tech advisory and implementation positions.

Patrick: I keep hearing about industry clouds; do you have a breakdown of each vendor’s performance by industry?

Boz: With enterprise buyers viewing industry specialization as table stakes, the need to apply cross-industry use cases will elevate the role of SIs as orchestrators. Building out solutions for today’s problems with an eye toward future opportunities will help vendors capitalize on their investments, but only if they are able to maintain service delivery quality, trust and transparency.

The resurgence of industry clouds is testing services vendors’ mantra around vendor agnosticism as they try to balance commitments to their technology partners with addressing industry-specific client pain points. Industry cloud is far from a new phenomenon, with vendors employing industry-based cloud strategies since 2014, when SAP cited plans to target 25 industries.

Though industry-based clouds found early success, TBR believes uptake was limited as clients were largely focused on horizontal needs as they deployed productivity-based suites. Given the maturity of cloud today, the need for industry-based configurations has increased as adopters pursue custom solutions set against an industry backdrop.

Further, the nuanced nature of industry-based requirements and compliance standards faced by industries, such as financial services, healthcare and government, necessitate vertically tailored offerings. As a result, technology vendor investments around industry-based cloud have accelerated in the last couple of years.

TBR will continue to monitor and analyze vendor performance and ecosystem evolution around industry clouds. We hope to include industry revenue breakouts for IT services vendors by hyperscaler practice area in the next 18 months. But before we can publish our analysis, we need to have confidence in the data and complete all steps in the insights intelligence cycle, from collection through vetting, validating and publishing.

Patrick: I’m not seeing all of the IT services vendors TBR covers. Are there plans to add more vendors to this report?

Boz: Cloud Ecosystems Market Landscape started with 10 vendors across IT services and consulting spectrums, with the goal of providing a fair comparison across portfolio offerings, go-to-market strategies and performance and to set the stage of the market. We will continue to expand the vendor roster, provided there is enough activity and implications across the three hyperscaler practices.

In this month’s blog we’ve highlighted three different strategies well-suited to these IT services vendors’ strengths and positions in the market as well as trends pressuring everyone to change how they partner, particularly in a volatile, yet lucrative market.

Not everyone can or should try to emulate Accenture, TCS and/or Deloitte, but lessons learned around how and why they partner with hyperscalers could be valuable in any IT ecosystem.

Technology Business Research, Inc.

Technology Business Research, Inc.

Leave a Reply

Want to join the discussion?Feel free to contribute!