Investing Big in GenAI Today: The Key to Unlocking Massive Long-term Returns

GenAI requires massive investment now for a chance at massive long-term returns

For most new technologies and trends in the IT space, actual business momentum and revenue generation typically take years to develop. In fact, in many cases, particularly with new technologies available to consumers, monetization may never develop, as the expectation of free trials or advertising-led revenue streams never leads to sustainable business models.

The history around monetizing new technologies is what makes the rise of generative AI (GenAI) over the past 18 months so notable. In such a short period of time, we have tangible evidence from some of the largest IT vendors that billions of dollars in revenue have already been generated in the space, with the expectation that even more opportunity will develop in the coming years.

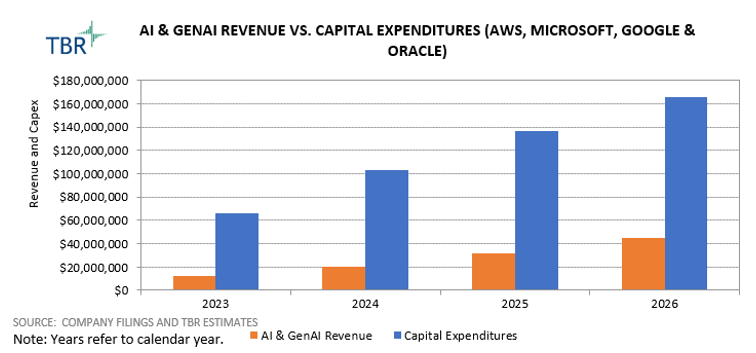

AI and GenAI revenue streams have not come without investment, however, as the infrastructure required to enable the new technology has been significant. The three major hyperscale cloud providers have borne the brunt of this required investment, outlaying billions of dollars to build out data centers, upgrade networking and install high-performance GPU-based servers. Amazon Web Services (AWS), Microsoft, Google and other cloud platform providers were already spending tens of billions annually to maintain and expand their cloud service offerings, and GenAI adds significantly to that investment burden.

The early revenue growth resulting from GenAI offerings has been promising, but put in the context of the increased investment required, it becomes clear that the business impacts of the technology will play out over an extended time period. Most public companies execute quarterly, plan annually and, as a stretch, project their expectations out over three to five years.

The impact of GenAI extends even further, as Microsoft CFO Amy Hood stated on the company’s fiscal 4Q24 earnings call: “Cloud and AI-related spend represents nearly all of our total capital expenditures. Within that, roughly half is for infrastructure needs where we continue to build and lease data centers that will support monetization over the next 15 years and beyond.” That means not only that Microsoft spent $19 billion on capital expenditures during a single quarter to support cloud and AI but also that the time horizon for the returns on that investment stretches beyond a decade.

Microsoft is, in this way, representative of all cloud platform peers, investing huge sums of capital expenditures now to realize modest new streams of revenue in the short term and anticipating significant revenue opportunity over the next 20 years.

AI-related revenue is already considerable, with growth expected to persist

TBR estimates the four leading cloud platform vendors generated more than $12 billion in revenue from AI and GenAI services in 2023, which is in and of itself a sizable market. On top of that, we expect revenue from those four vendors to increase by 71% during 2024.

Below are examples from some of the largest monetizers of GenAI so far, with estimates on the current size of their respective businesses and the strategies they use. A market of that scale and growth trajectory is notable in an IT environment where much more modest growth is the norm. While we expect growth to gradually slow and normalize over the coming years, the AI and GenAI markets remain attractive nonetheless. Insights follow about how some of the current leaders in this space are monetizing.

Microsoft (estimated $1 0 billion in GenAI revenue annually): While Microsoft did not quite meet Wall Street’s lofty expectations for AI-related revenue growth, the company posted a solid quarter in 2Q24. In TBR’s opinion, Microsoft’s GenAI strategy is on the right track, and its financial results align closely with our expectations. In 2Q24 Azure AI services contributed 8% of Azure’s 29% year-to-year growth, while Copilot was cited as a growth driver for Office 365.

Nevertheless, with Office 365 revenue growth decelerating compared to past quarters, it is clear the monetization of GenAI will take time to materialize. Still, given Microsoft’s current capex spend and capex forecast, the company is committed to its AI strategy. Management stated nearly all $19 billion of capital expenditures this quarter was focused on the cloud business, with roughly half going toward data center construction and the other half used to procure infrastructure components like GPUs.

This hefty commitment indicates that GenAI will remain at the forefront of Microsoft’s product development, go-to-market and partner strategies for years to come as the company looks to turn an early lead into an established position atop the AI and GenAI market.

AWS (estimated $2.5 billion in GenAI revenue annually): During AWS’ New York City Summit event in July, Matt Wood, the company’s VP of AI Products, noted that GenAI had already become a multibillion-dollar business for the company. Amazon CEO Andy Jassy has also spoken confidently about the future of AI, publicly proclaiming the company’s belief that GenAI would grow to generate tens of billions in revenue in the coming years.

The fact that AWS has been playing in AI infrastructure, with custom chip lines for both training and inference, well before the GenAI hype cycle is notable. Customers are not likely to go through the daunting task of moving off industry standard hardware, so these custom offerings can still be a more cost-effective source for net-new workloads, which is one of the reasons they signify a lot of potential for GenAI.

AWS’ custom offerings, coupled with tools that customers use to build and fine-tune models, such as Bedrock and SageMaker, will continue to spin the EC2 meter. AWS does have other GenAI monetization plans with a two-tiered pricing model for Amazon Q Business and Q Developer. However, it is still early days for these offerings, and Microsoft Copilot entering the mix, at least from the line-of-business (LOB) perspective, clearly indicates AWS faces an uphill battle.

Google Cloud (estimated $2 billion in GenAI revenue annually): Unlike some of its peers in the industry, Alphabet has not clearly quantified the impact that GenAI is having on Google Cloud’s top line. However, on Alphabet’s recent earnings call, executives said that GenAI solutions have generated billions of dollars year to date and are used by “the majority” of Google Cloud’s top 100 customers.

These results, coupled with a 40-basis-point acceleration in Google Cloud’s 2Q24 revenue growth rate, to 28.8%, signal that while GenAI is having an impact on Google Cloud Platform (GCP) revenue growth, it is very early days. Steps Google Cloud is taking to boost developer mindshare — with over 2 million developers using its GenAI solutions — and align with global systems integrator (GSI) partners to unlock new use cases, leave us confident Google Cloud can more aggressively vie for GenAI spend through 2025.

ServiceNow (less than $100 million in GenAI revenue annually): With Now Assist net-new annual contract value (NNACV) doubling from last quarter, ServiceNow’s steady momentum selling GenAI to the enterprise continues. Now Assist was included in 11 deals over $1 million in annual contract value (ACV) in 2Q24, showing positive early signs that the strategy of packaging premium digital workflow products based on domain-specific large language models (LLMs) is resonating.

At 45%, ServiceNow’s Pro SKU penetration rate, which represents the percentage of customer accounts on Pro or Enterprise editions of IT Service Management (ITSM), HR Service Delivery (HRSD) and CSM products, is already very strong. Upgrading these already premium customers to Pro Plus SKUs with GenAI, for which ServiceNow has already realized a 30% price uplift, could signify an opportunity for ServiceNow valued at well over $1 billion. Naturally, a big focus is expanding the availability of Pro Plus outside the core workflow products.

IBM (less than $2 billion in GenAI revenue annually): Approximately 75% of IBM’s reported $2 billion in GenAI book of business to date stems from services signings, and IBM lands nearly all watsonx deals thorough Consulting. Companies need help getting started with GenAI in the cloud, and IBM’s ability to lead with Consulting and go to market as both a technology and consulting organization will continue to prove unique in the GenAI wave.

On the software side, overcoming challenges with the Watson brand and deciding how much it wants to compete with peers have been obstacles, but IBM is now strategically pivoting around the middleware layer, hoping to act as a GenAI orchestrator that helps customers build and run AI models in a hybrid fashion. This pivot has resulted in a series of close-to-the-box investments, including Red Hat’s InstructLab project, which allows customers to fine-tune and customize Granite models, and IBM Concert for application management.

According to IBM, these types of GenAI assets have contributed roughly $0.5 billion to IBM’s AI book of business. By adopting a strategy to embed its AI infrastructure software into the cloud ecosystem of GenAI tools and copilots already widely accepted by customers, IBM ensures it stays relevant with these cutting-edge workloads.

Oracle (less than $100 million in GenAI revenue annually): With the Oracle Cloud Infrastructure (OCI) GenAI Service hitting general availability in January and a code assist tool only recently launched into preview, Oracle has been late to the GenAI game. But the company has highlighted several multibillion-dollar contracts for AI training on OCI, which speaks to its tight relationship with NVIDIA and ample supply of GPUs.

As an API-based service providing out-of-the-box access to LLMs for generic use cases, the OCI GenAI Service on its own does not necessarily differ from what other hyperscalers are doing. What does stand out is that Oracle offers the entire SaaS suite. Given that all Fusion SaaS instances are hosted on OCI, where the GenAI service was built, Oracle can deliver GenAI capabilities to SaaS customers at no added cost.

This means Oracle’s GenAI monetization will be purely from an infrastructure perspective. GPU supply and the cost efficacy of OCI will help Oracle bring new workloads into the pipeline, and we will see a bigger impact to growth in 2025. For context, Oracle’s remaining performance obligations balance (though some includes Cerner) is $98 billion.

Dive Into the Future of GenAI with TBR Analysts Patrick Heffernan, Bozhidar Hristov and Kelly Lesiczka

Beyond revenue generation, cost savings is part of the value proposition for cloud vendors and customers alike

Many of the leading IT vendors’ GenAI strategies have centered on investing in solutions for customers. However, vendors have also been serving as customer zero for the technology by implementing it internally. The results from their early implementations seem very much like end-customer use cases, which focus on cost savings and efficiency as the easiest benefits to realize. While many IT vendors have seen operating expenses and headcount level off over the past couple of quarters, implying that AI has had some impact on company efficiency, IBM and SAP have both explicitly stated AI’s impact on their operating models.

IBM was one of the earliest vocal proponents for the labor-saving benefits AI could bring to its business. In mid-2023 CEO Arvind Krishna announced a hiring freeze and shared an expectation that AI would replace 8,000 jobs. IBM remains focused on driving productivity gains, which it is largely doing by lowering the internal cost of IT and rebalancing the global workforce. This includes using AI to automate back-office functions. Such efforts have IBM on track to deliver a minimum of $3 billion in annual run-rate savings by the end of 2024.

Meanwhile, SAP’s decision to increase its planned FTE reallocation from a previous target of 8,000 to a new range of between 9,000 and 10,000 FTEs shows the company is committed to improving operating efficiency. While the bulk of the restructuring will consist of reallocating FTEs into lower-cost geographies and strategically important business units, taking a customer-zero approach with GenAI is also a component. SAP is leveraging business AI tools focused on areas like finance & accounting and human resources to reduce the labor intensity within the respective business units.

Just like end customers, vendors are investing significantly now in hopes of generating long-term GenAI returns

As seen in TBR’s Cloud Customer Research streams, customers have been investing in GenAI solutions with some haste, forgoing clear ROI measurements or typical budgeting procedures. Customers, as well as the major vendors we cover, have a sense of urgency around GenAI and share the feeling that if they do not embrace these new solutions now, it could place them at a long-term competitive disadvantage. If customers are not making full use of GenAI capabilities, their competitors will be more efficient and productive and capture more growth opportunities. For vendors, the ability to not only deliver GenAI capabilities but also do so at scale will be a competitive necessity for decades to come.

In this regard, customers and vendors find themselves in a similar situation, investing in GenAI now just for the possibility of a future advantage, but the scale of investments required are quite different. Customers have the good fortune of leveraging scalable, subscription-based services for many of these GenAI technologies. Customers are still extending their IT budgets and paying more to incorporate GenAI, but they do not have large fixed costs and long-term commitments at this point.

Vendors, on the other hand, need to make significant investments, even beyond the already huge levels of investment to support cloud services, to capitalize on the GenAI opportunity. The scale of investment cannot be understated for the largest cloud platform providers like AWS, Microsoft, Google and Oracle. All of these vendors were already investing tens of billions of dollars annually to support data center and infrastructure build-outs.

The unique data center and infrastructure requirements to deliver GenAI solutions, including the GPU-based systems, are driving double-digit to triple-digit increases in capex spending for leading vendors. Not only is the level of spending noticeable, the time periods for the returns are also lengthy. In communicating those increased expenses to investors and Wall Street analysts, vendors like Microsoft messaged the returns from these investments playing out over the next 15 years, a time horizon seldom mentioned previously.

Just_Super, Getty Images via Canva Pro

Just_Super, Getty Images via Canva Pro Elitsa Bakalova

Elitsa Bakalova