Cloud Opportunity Expected to Increase Once DOGE Disruption Subsides

The U.S. federal government will need modern cloud services to be most efficient, regardless of DOGE-driven changes

Rolling pockets of chaos and an overall cloud of uncertainty may be the best way to describe the first two months of the new Trump administration. One upside to federal contracts is that they tend to be long-term in nature, which provides some stability for all types of vendors with existing contracts. However, the current transition has been rocky, to say the least, as contracts are getting canceled, agency staffing is reduced, and the existence of entire agencies is called into question.

Beyond the distinct financial impacts that are occurring to many federal systems integrators (FSIs) and IT vendors, the overall uncertainty about future changes has complicated government contractors’ ability to conduct business as usual. Short-term uncertainty will likely persist, but eventually we will see a silver lining for the ecosystem of IT providers catering to the needs of the U.S. federal government. The government may become a more streamlined entity, in all respects, but IT will need to remain at the forefront of U.S. government operations.

Differences of opinion on optimal levels of funding will persist, but most people concur that the IT infrastructure supporting many core government agencies is antiquated and long overdue for upgrade. After the Department of Government Efficiency (DOGE) completes its cost-cutting and agency reorganizations, the overall approach to modernizing those systems will come into greater clarity, but third parties including FSIs and IT vendors like Amazon Web Services (AWS), Microsoft, Google and Oracle will all likely be a part of the solution enabling the reformed federal government to modernize and play an ongoing role eliminating waste, fraud and abuse using a refreshed IT infrastructure environment.

Vendors hope federal spending materializes after the fog of dismantling and reducing headcount dissipates

Reducing the size of the federal workforce was an immediate focus for DOGE. With the “Fork in the Road” email sent by the Office of Personnel Management to encourage staff resignations and the nonvoluntary firing of workers across civilian agencies, the total number of employees shed from the federal workforce is estimated to have surpassed 100,000 in the first two months of the Trump presidency.

The entire federal workforce still totals more than 3 million, excluding 1.3 million active military personnel, and additional cuts are a certainty. Early in the formation of DOGE, the idea of cutting up to 75% of federal workers was floated, which could be far-fetched in reality. Regardless, it is clear the workforce-reduction efforts will continue to be a focus as DOGE expands its reach to additional government agencies and pushes further than just the probationary employees that made up the bulk of early reductions.

As headcount reductions continue, cloud and software vendors could assist the administration with those cuts while, at the same time, be impacted by the fallout of those cuts. On Workday’s FY4Q25 earnings call, CEO Carl Eisenbach painted the impact of DOGE in an opportunistic light, stating: “In fact, the majority of them [federal IT systems] are still on-premise, which means they’re inefficient. And as we think about DOGE and what that could potentially do going forward, if you want to drive efficiency in the government, you have to upgrade your systems. And we find that as a really rich opportunity.”

If, in the era of DOGE, government agencies undertake new, or continue existing, efforts to modernize IT systems and adopt cloud-enabled solutions, it would certainly be a big opportunity not just for Workday, but for the entire federal IT contractor market. The certainty of that opportunity is still questionable, however, given the rapidity with which major changes to how government operates are occurring. Any technology opportunities with USAID (United States Agency for International Development), for instance, are now dubious given the speed with which the agency has been dissolved, even as legal challenges abound.

Additional rapid changes will occur with the Department of Education given President Trump’s clear directive to new Secretary of Education Linda McMahon to dismantle the agency. On ServiceNow’s 4Q24 earnings call, CFO Gina Mastantuono noted some of this uncertainty while also remaining optimistic about the federal opportunity, stating the company’s guidance reflects a stronger U.S. federal performance in the back half of 2025, given changes brought on by the administration.

A build-it-yourself approach could challenge packaged IT solutions

DOGE head Elon Musk has clearly employed many of the same techniques and strategies he has used in the past, such as sending a “Fork in the Road” email to Twitter employees and requiring them to send a weekly email of their accomplishments after he purchased Twitter (now called X). With that in mind, it is relevant to think about the approaches to IT that Musk has used as CEO of Tesla and SpaceX for clues about what might occur in the U.S. federal space.

For some of the most important mission-critical IT and software decisions at Tesla and SpaceX, Musk deployed a proprietary software package that is shared by the companies to manage core manufacturing and sales, CRM and financial processes. Instead of utilizing a prebuilt solution from the likes of SAP or Oracle, internal teams at SpaceX and Tesla built, customized and manage their own ERP solution named WARPDRIVE. Musk could very well encourage a similar approach in federal agencies, either by licensing WARPDRIVE to those agencies or by directing more proprietary programs to be custom-built to reduce expenditures and theoretically achieve a superior technological solution. Either option would be challenging to implement but remains within the realm of possibility and would effectively reduce the addressable market for third-party IT solutions.

Watch Now: Deep Dive into Generative AI’s Impact on the Cloud Market in 2025

Scaling back new and existing awards will stifle revenue for cloud vendors in the short term

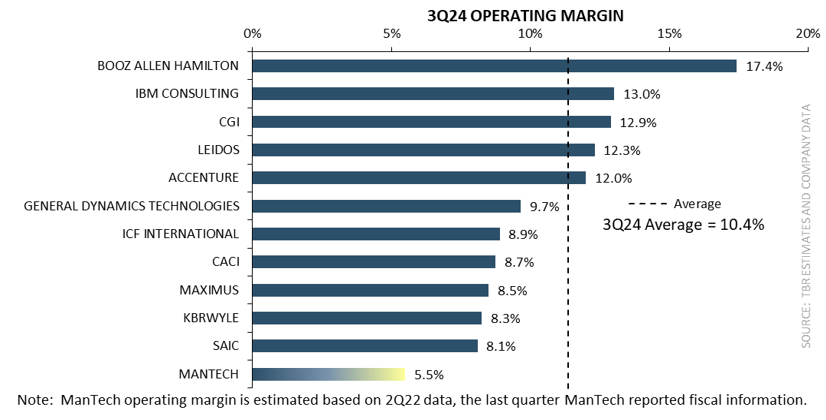

In the U.S. federal sector, SIs are a key conduit for how cloud and software companies capture opportunities. The opportunity pipeline and associated timeline for deals is notoriously long for federal spending, but the total opportunity has already decreased in size based on the cuts made by DOGE. Some of the strategies and actions recently used by leading SIs in the federal space are discussed in TBR’s special report, Leading Federal Systems Integrators React to U.S. Department of Government Efficiency. As outlined in the special report, all 12 of the leading federal SIs are looking to reduce expenses and prepare for a slowing of revenue streams in the near term. After a period of federal investment and expansion, this certainly is a change in trajectory for their businesses. In addition to making similar cost reductions, all 12 vendors are also doubling down on their competitive differentiation to secure growth moving forward. All of the recent market shifts, including security, AI and digital transformation, have led FSIs to reinvest in capabilities that provide the best opportunities for long-term expansion.

In the short term, even existing contracts with the federal government are subject to reductions or termination, which impacts not only the SI but also the IT vendors that have secured subawards to provide their technology as part of the overall engagement. One example TBR cited in the special report was the $1.5 billion award Leidos has with the Social Security Administration (SSA), which includes subawards for Pegasystems, AWS and multiple other IT vendors. The Leidos deal was scaled back by DOGE, marking the beginning of the disruption to awards with SIs and subawards with IT vendors. SSA represents a small portion of the federal budget, so when DOGE looks to larger agencies such as the Department of Health and Human Services for cost reductions and efficiencies, the impact on the federal SIs and supporting IT vendors will be even greater.

In terms of the scale of revenue at stake, AWS alone has won close to $500 million in subaward contracts in the last three fiscal years. That does not directly translate into revenue, however, as the money still needs to be outlaid, a process that is even more tenuous given the current spending environment and actions taken by the DOGE team. In addition to deals tied to FSIs, cloud vendors and software vendors also have direct deals/prime awards with federal agencies that are at greater risk. AWS, for instance, has won a total of $445 million in prime award contracts over the past three fiscal years.

Most of those awards are multiyear contracts that are not guaranteed, and the revenue could be reduced or not disbursed. In fact, only $104 million of those awards to AWS have been outlaid, meaning the balance, more than $340 million, could be impacted. It is also important to note these figures only reflect past deals; we anticipate the new federal deal pipeline for vendors like AWS to shrink due to uncertainty and the administration’s focus on cost reductions.

Big cloud deals such as JWCC and Stargate are expected to proceed without significant funding impacts

The impacts of DOGE should be widespread throughout the government, but we expect the top federal IT opportunities, the Stargate Project and the Joint Warfighting Cloud Capability (JWCC) contract vehicle, to avoid major funding challenges. Though both projects are in the early stages and still subject to competitive jockeying between technology providers to secure task orders, we expect the funding to remain available even amid broader spending reductions.

The JWCC was announced in 2022 with a total of $9 billion in funding available to Oracle, Microsoft, AWS and Google Cloud. Oracle has been a leading provider under the contract to date. Roughly $2.5 billion has been awarded to the five vendors thus far in the contract, leaving more than $6 billion in additional task orders in the entire project. The spending bill passed in mid-March to avoid a federal shutdown illustrates the appetite to sustain, if not increase, defense spending. All the participants in JWCC have donated to and publicly supported the administration, which could solidify the longevity of the engagement.

Stargate was introduced by President Trump in the early days of his presidency, indicating that the project is likely to proceed in some fashion regardless of any budgetary pressure. The project will be a joint venture with OpenAI, SoftBank and Oracle to initially build a $100 billion data center in Texas. Over the next four years, the project aims to build additional large-scale data centers, with a total of $500 billion in funding, making it the largest centralized data center investment in history. The funding includes significant financial backing from the U.S. government, with contributions from SoftBank, a firm known for its long-term investment strategies. OpenAI, SoftBank, Oracle and MGX are the initial equity investors, while Arm, Microsoft, NVIDIA and OpenAI have been named as technology partners and will have some involvement in the project.

Modern cloud IT solutions should have an elevated role in the restructured federal government

The headcount reductions, eliminations of agencies, and overall uncertainty will disrupt business as usual in the U.S. federal sector at least through the end of 2Q25. Once the new, smaller and streamlined structure emerges, we expect the value of modern IT solutions to be recognized and spending to resume and even increase compared with the prior trajectory. Having fewer human resources, likely fewer skilled IT professionals, and an altered view of budgeting and ROI for all initiatives, IT included, all amplify the value that can be added by modernizing the infrastructure and solutions that support the mission of government agencies.

Across fragmented environments, many of which are still traditional on premises and based on aging technology, consolidation and use of government-grade cloud delivery can improve performance and reduce the total cost to deliver even over a relatively short three-to-five-year time frame. On the commercial side, many of the organizations we speak with note that the simplification of their IT environments is one of the strongest drivers of cloud adoption. AI and generative AI capabilities add to the benefits that can now be enabled. And for government agencies, preexisting data protocols and procedures increase their readiness to apply next-generation data analysis and AI. We see the business use cases for AI becoming more compelling on the commercial side, which bodes well for adding real value in the U.S. federal sector as it adapts to a more streamlined way of operations.