There is no GenAI strategy without a data strategy

Realizing the long-promised ROI of generative AI (GenAI) will require customers look for ways to better access, integrate, manage and govern large amounts of unstructured data. Data-native ISVs, hyperscalers and global systems integrators (GSIs) are evolving their critical ecosystems of solutions to deliver on the commitments of GenAI for enterprise. As such, roles within the cloud ecosystem are shifting, and the increase in open APIs and architectures will have lasting impacts on many data cloud ISVs and GSIs, including how they partner with one another as they race to gain AI workloads.

In this TBR Insights Live session, TBR Principal Analyst Boz Hristov and Senior Analyst Catie Merrill share their insights into data cloud ISVs’ and hyperscalers’ strategies and their professional services partners, as well as how forming a triparty alliance structure at the data layer will help partners pursue higher-value GenAI opportunities.

Additionally, the pair share an exclusive look at TBR’s revamped Cloud Data & Analytics Market Landscape, which provides insight into enterprises’ data strategies, vendor analysis by workload, and where the market is headed through 2025 and beyond. TBR’s Cloud Data & Analytics research stream tracks all hyperscalers; SaaS vendors such as SAP and Salesforce; and data cloud ISVs including Boomi, Confluent, Cloudera, Databricks, Informatica, MongoDB and Snowflake. The research also looks at the overarching layers of the data cloud stack, from storage and querying to business intelligence.

Watch the below session on the emerging data ecosystem to learn:

The data cloud ISVs that have demonstrated success in alliance strategies

Ecosystem best practices of data cloud ISVs

C-Suite priorities regarding data management and GenAI

How hyperscalers are adjusting their partnering strategies to improve the flow of data and win new GenAI workloads

Why vendors are positioning around data intelligence, and the components necessary to succeed in this space

Excerpt from The Emerging Data Ecosystem: ISVs, Hyperscalers and Global Systems Integrators

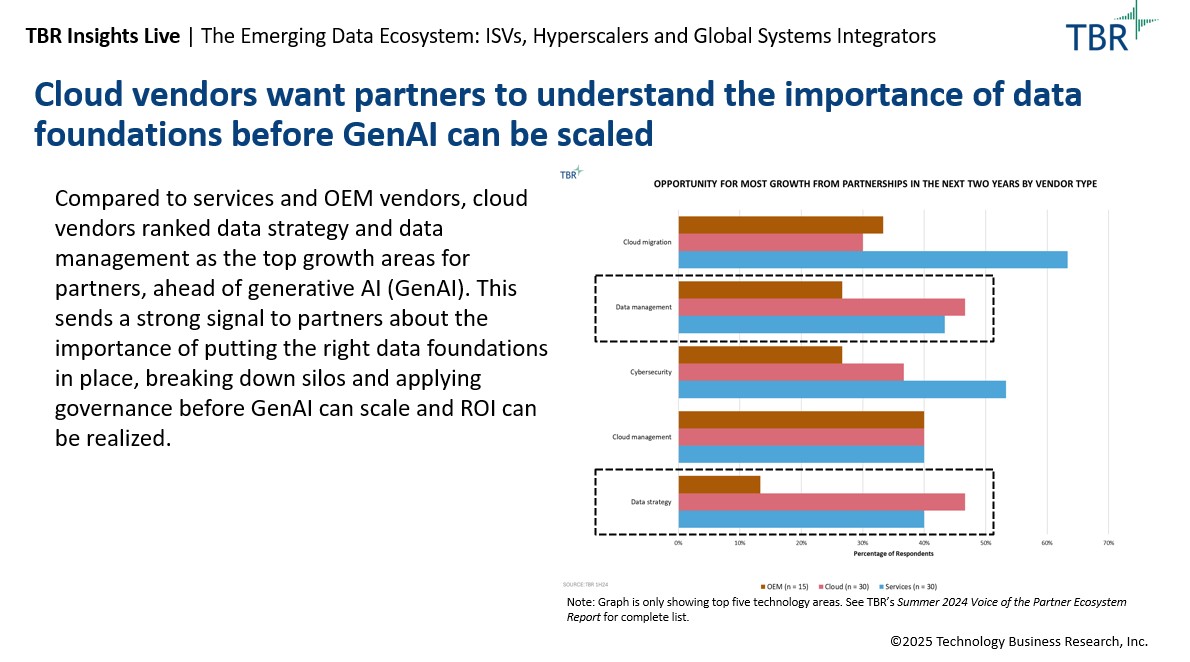

Cloud vendors want partners to understand the importance of data foundations before GenAI can be scaled

Compared to services and OEM vendors, cloud vendors ranked data strategy and data management as the top growth areas for partners, ahead of generative AI (GenAI). This sends a strong signal to partners about the importance of putting the right data foundations in place, breaking down silos and applying governance before GenAI can scale and ROI can be realized.

Visit this link to download this session’s presentation deck here.

TBR Insights Live sessions are held typically on Thursdays at 1 p.m. ET and include a 15-minute Q&A session following the main presentation. Previous sessions can be viewed anytime on TBR’s Webinar Portal.

https://tbri.com/wp-content/uploads/2025/04/WI_CloudDataAnalytics_2Q25_RegisterNow.png10801080TBRhttps://tbri.com/wp-content/uploads/2021/09/TBR-Insight-Center-Logo.pngTBR2025-04-04 17:04:382025-05-05 17:12:23The Emerging Data Ecosystem: ISVs, Hyperscalers and Global Systems Integrators

The U.S. federal government will need modern cloud services to be most efficient, regardless of DOGE-driven changes

Rolling pockets of chaos and an overall cloud of uncertainty may be the best way to describe the first two months of the new Trump administration. One upside to federal contracts is that they tend to be long-term in nature, which provides some stability for all types of vendors with existing contracts. However, the current transition has been rocky, to say the least, as contracts are getting canceled, agency staffing is reduced, and the existence of entire agencies is called into question.

Beyond the distinct financial impacts that are occurring to many federal systems integrators (FSIs) and IT vendors, the overall uncertainty about future changes has complicated government contractors’ ability to conduct business as usual. Short-term uncertainty will likely persist, but eventually we will see a silver lining for the ecosystem of IT providers catering to the needs of the U.S. federal government. The government may become a more streamlined entity, in all respects, but IT will need to remain at the forefront of U.S. government operations.

Differences of opinion on optimal levels of funding will persist, but most people concur that the IT infrastructure supporting many core government agencies is antiquated and long overdue for upgrade. After the Department of Government Efficiency (DOGE) completes its cost-cutting and agency reorganizations, the overall approach to modernizing those systems will come into greater clarity, but third parties including FSIs and IT vendors like Amazon Web Services (AWS), Microsoft, Google and Oracle will all likely be a part of the solution enabling the reformed federal government to modernize and play an ongoing role eliminating waste, fraud and abuse using a refreshed IT infrastructure environment.

Explore the expected impact of DOGE on federal systems integrators and how it could shape the technology landscape

Vendors hope federal spending materializes after the fog of dismantling and reducing headcount dissipates

Reducing the size of the federal workforce was an immediate focus for DOGE. With the “Fork in the Road” email sent by the Office of Personnel Management to encourage staff resignations and the nonvoluntary firing of workers across civilian agencies, the total number of employees shed from the federal workforce is estimated to have surpassed 100,000 in the first two months of the Trump presidency.

The entire federal workforce still totals more than 3 million, excluding 1.3 million active military personnel, and additional cuts are a certainty. Early in the formation of DOGE, the idea of cutting up to 75% of federal workers was floated, which could be far-fetched in reality. Regardless, it is clear the workforce-reduction efforts will continue to be a focus as DOGE expands its reach to additional government agencies and pushes further than just the probationary employees that made up the bulk of early reductions.

As headcount reductions continue, cloud and software vendors could assist the administration with those cuts while, at the same time, be impacted by the fallout of those cuts. On Workday’s FY4Q25 earnings call, CEO Carl Eisenbach painted the impact of DOGE in an opportunistic light, stating: “In fact, the majority of them [federal IT systems] are still on-premise, which means they’re inefficient. And as we think about DOGE and what that could potentially do going forward, if you want to drive efficiency in the government, you have to upgrade your systems. And we find that as a really rich opportunity.”

If, in the era of DOGE, government agencies undertake new, or continue existing, efforts to modernize IT systems and adopt cloud-enabled solutions, it would certainly be a big opportunity not just for Workday, but for the entire federal IT contractor market. The certainty of that opportunity is still questionable, however, given the rapidity with which major changes to how government operates are occurring. Any technology opportunities with USAID (United States Agency for International Development), for instance, are now dubious given the speed with which the agency has been dissolved, even as legal challenges abound.

Additional rapid changes will occur with the Department of Education given President Trump’s clear directive to new Secretary of Education Linda McMahon to dismantle the agency. On ServiceNow’s 4Q24 earnings call, CFO Gina Mastantuono noted some of this uncertainty while also remaining optimistic about the federal opportunity, stating the company’s guidance reflects a stronger U.S. federal performance in the back half of 2025, given changes brought on by the administration.

A build-it-yourself approach could challenge packaged IT solutions

DOGE head Elon Musk has clearly employed many of the same techniques and strategies he has used in the past, such as sending a “Fork in the Road” email to Twitter employees and requiring them to send a weekly email of their accomplishments after he purchased Twitter (now called X). With that in mind, it is relevant to think about the approaches to IT that Musk has used as CEO of Tesla and SpaceX for clues about what might occur in the U.S. federal space.

For some of the most important mission-critical IT and software decisions at Tesla and SpaceX, Musk deployed a proprietary software package that is shared by the companies to manage core manufacturing and sales, CRM and financial processes. Instead of utilizing a prebuilt solution from the likes of SAP or Oracle, internal teams at SpaceX and Tesla built, customized and manage their own ERP solution named WARPDRIVE. Musk could very well encourage a similar approach in federal agencies, either by licensing WARPDRIVE to those agencies or by directing more proprietary programs to be custom-built to reduce expenditures and theoretically achieve a superior technological solution. Either option would be challenging to implement but remains within the realm of possibility and would effectively reduce the addressable market for third-party IT solutions.

Watch Now: Deep Dive into Generative AI’s Impact on the Cloud Market in 2025

Scaling back new and existing awards will stifle revenue for cloud vendors in the short term

In the U.S. federal sector, SIs are a key conduit for how cloud and software companies capture opportunities. The opportunity pipeline and associated timeline for deals is notoriously long for federal spending, but the total opportunity has already decreased in size based on the cuts made by DOGE. Some of the strategies and actions recently used by leading SIs in the federal space are discussed in TBR’s special report, Leading Federal Systems Integrators React to U.S. Department of Government Efficiency. As outlined in the special report, all 12 of the leading federal SIs are looking to reduce expenses and prepare for a slowing of revenue streams in the near term. After a period of federal investment and expansion, this certainly is a change in trajectory for their businesses. In addition to making similar cost reductions, all 12 vendors are also doubling down on their competitive differentiation to secure growth moving forward. All of the recent market shifts, including security, AI and digital transformation, have led FSIs to reinvest in capabilities that provide the best opportunities for long-term expansion.

In the short term, even existing contracts with the federal government are subject to reductions or termination, which impacts not only the SI but also the IT vendors that have secured subawards to provide their technology as part of the overall engagement. One example TBR cited in the special report was the $1.5 billion award Leidos has with the Social Security Administration (SSA), which includes subawards for Pegasystems, AWS and multiple other IT vendors. The Leidos deal was scaled back by DOGE, marking the beginning of the disruption to awards with SIs and subawards with IT vendors. SSA represents a small portion of the federal budget, so when DOGE looks to larger agencies such as the Department of Health and Human Services for cost reductions and efficiencies, the impact on the federal SIs and supporting IT vendors will be even greater.

In terms of the scale of revenue at stake, AWS alone has won close to $500 million in subaward contracts in the last three fiscal years. That does not directly translate into revenue, however, as the money still needs to be outlaid, a process that is even more tenuous given the current spending environment and actions taken by the DOGE team. In addition to deals tied to FSIs, cloud vendors and software vendors also have direct deals/prime awards with federal agencies that are at greater risk. AWS, for instance, has won a total of $445 million in prime award contracts over the past three fiscal years.

Most of those awards are multiyear contracts that are not guaranteed, and the revenue could be reduced or not disbursed. In fact, only $104 million of those awards to AWS have been outlaid, meaning the balance, more than $340 million, could be impacted. It is also important to note these figures only reflect past deals; we anticipate the new federal deal pipeline for vendors like AWS to shrink due to uncertainty and the administration’s focus on cost reductions.

Big cloud deals such as JWCC and Stargate are expected to proceed without significant funding impacts

The impacts of DOGE should be widespread throughout the government, but we expect the top federal IT opportunities, the Stargate Project and the Joint Warfighting Cloud Capability (JWCC) contract vehicle, to avoid major funding challenges. Though both projects are in the early stages and still subject to competitive jockeying between technology providers to secure task orders, we expect the funding to remain available even amid broader spending reductions.

The JWCC was announced in 2022 with a total of $9 billion in funding available to Oracle, Microsoft, AWS and Google Cloud. Oracle has been a leading provider under the contract to date. Roughly $2.5 billion has been awarded to the five vendors thus far in the contract, leaving more than $6 billion in additional task orders in the entire project. The spending bill passed in mid-March to avoid a federal shutdown illustrates the appetite to sustain, if not increase, defense spending. All the participants in JWCC have donated to and publicly supported the administration, which could solidify the longevity of the engagement.

Stargate was introduced by President Trump in the early days of his presidency, indicating that the project is likely to proceed in some fashion regardless of any budgetary pressure. The project will be a joint venture with OpenAI, SoftBank and Oracle to initially build a $100 billion data center in Texas. Over the next four years, the project aims to build additional large-scale data centers, with a total of $500 billion in funding, making it the largest centralized data center investment in history. The funding includes significant financial backing from the U.S. government, with contributions from SoftBank, a firm known for its long-term investment strategies. OpenAI, SoftBank, Oracle and MGX are the initial equity investors, while Arm, Microsoft, NVIDIA and OpenAI have been named as technology partners and will have some involvement in the project.

Modern cloud IT solutions should have an elevated role in the restructured federal government

The headcount reductions, eliminations of agencies, and overall uncertainty will disrupt business as usual in the U.S. federal sector at least through the end of 2Q25. Once the new, smaller and streamlined structure emerges, we expect the value of modern IT solutions to be recognized and spending to resume and even increase compared with the prior trajectory. Having fewer human resources, likely fewer skilled IT professionals, and an altered view of budgeting and ROI for all initiatives, IT included, all amplify the value that can be added by modernizing the infrastructure and solutions that support the mission of government agencies.

Across fragmented environments, many of which are still traditional on premises and based on aging technology, consolidation and use of government-grade cloud delivery can improve performance and reduce the total cost to deliver even over a relatively short three-to-five-year time frame. On the commercial side, many of the organizations we speak with note that the simplification of their IT environments is one of the strongest drivers of cloud adoption. AI and generative AI capabilities add to the benefits that can now be enabled. And for government agencies, preexisting data protocols and procedures increase their readiness to apply next-generation data analysis and AI. We see the business use cases for AI becoming more compelling on the commercial side, which bodes well for adding real value in the U.S. federal sector as it adapts to a more streamlined way of operations.

https://tbri.com/wp-content/uploads/2025/04/level-of-impact_itjo_getty.png10801080Allan Krans, Practice Manager and Principal Analysthttps://tbri.com/wp-content/uploads/2021/09/TBR-Insight-Center-Logo.pngAllan Krans, Practice Manager and Principal Analyst2025-04-04 09:29:542025-04-04 09:29:54Cloud Opportunity Expected to Increase Once DOGE Disruption Subsides

TBR Spotlight Reports represent an excerpt of TBR’s full subscription research. Full reports and the complete data sets that underpin benchmarks, market forecasts and ecosystem reports are available as part of TBR’s subscription service. Click here to receive all new Spotlight Reports in your inbox.

Post Updated: Aug. 6, 2025

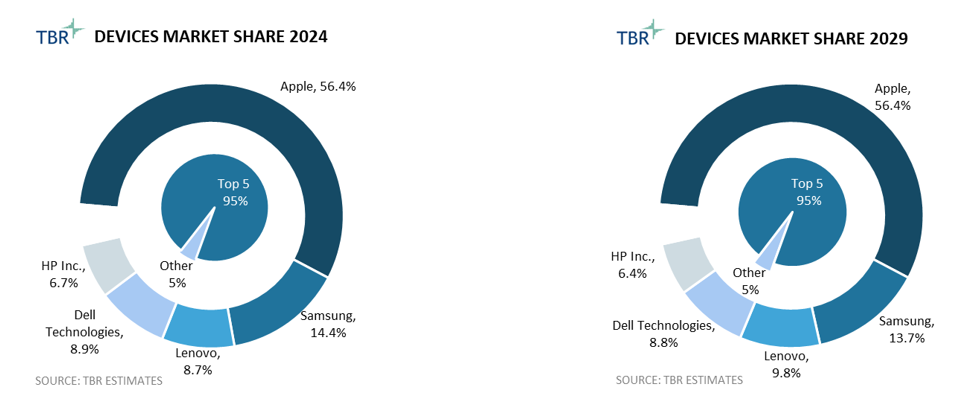

TBR predicts that Apple and Samsung will continue to lead in devices market share through 2029, and Lenovo will overtake Dell for the No. 3 spot

After declining for several quarters due to market saturation and tightened corporate IT budgets, PC demand is gradually recovering, particularly on the commercial side of the market as organizations begin to refresh their fleets of devices. TBR expects the devices market to grow at roughly a 2.7% CAGR from 2024 to 2029 as this recovery in PC demand is supplemented by growing smartphone and tablet revenue. TBR also expects demand for AI advisory and consultancy services will increase as organizations invest in implementing AI across IT infrastructure and client devices.

The proliferation of AI across the IT space presents devices vendors with a range of growth opportunities. PC OEMs will remain focused on driving AI PC adoption and gradually increasing these devices as a mix of total PC shipments to drive long-term revenue growth and average revenue per unit (ARPU) expansion. To help speed this adoption and increase services revenue, vendors will also continue to build out suites of services designed to help organizations take advantage of the productivity gains offered by AI PCs. TBR expects vendors to continue to increase their non-PC revenue mix, capitalizing on growth opportunities presented by AI and sheltering their top lines and margins from potential fluctuations in the PC market.

Apple continues to lead the devices market in revenue share by a significant margin due to its large, loyal and constantly expanding customer base, and TBR expects this position to remain unchanged through 2029. Among the major Windows PC OEMs, Dell Technologies (Dell) held the largest market share during 2024, followed by Lenovo and HP Inc. However, TBR expects Lenovo to overtake Dell for the top spot by 2029 as Lenovo takes advantage of PC revenue growth opportunities in China, bolstered by the expansion of its smartphone and tablet businesses.

Devices Market Share, 2024 and 2029 (Source: TBR)

If you believe you have access to the full research via your employer’s enterprise license or would like to learn how to access the full research, click the Access Research button.

TBR expects Apple will maintain its significant lead in the smartphone market through 2029, leveraging its Apple Intelligence platform to encourage customers to upgrade their devices

Apple remains the dominant player in the global smartphone market with its iPhone lineup, followed by Samsung, while Lenovo and Asus each maintain relatively small smartphone businesses that account for a combined total market share of less than 3%.

AI is becoming increasingly central to the smartphone space. Throughout the next several quarters, Apple will continue to expand the global availability and feature set of its Apple Intelligence AI platform. As Apple Intelligence is only compatible with the company’s newest lineup of smartphones, the iPhone 16 series, Apple intends to leverage the platform to encourage users to upgrade their devices sooner. So far, this strategy appears to be paying off, with Apple reporting on its 4Q24 earnings call that iPhone 16 sales were strongest in regions where Apple Intelligence is available.

Apple and Samsung will remain focused on driving sales of their high-end iPhone and Galaxy lineups, respectively, while Asus will continue to target the gaming market with devices under its Republic of Gamers (ROG) brand.

Premiumization is also central to Lenovo’s smartphone strategy, with the company focused on driving sales of phones under its Motorola brand, particularly the Moto Edge and the foldable Moto Razr. Additionally, Lenovo will leverage its purchase of former Fujitsu spinoff FCNT Ltd. to expand its smartphone market share in Japan.

Although China is a weak market for some vendors, TBR expects Lenovo to take advantage of AI PC opportunities in the country to expand APAC revenue

TBR expects the APAC devices market to grow at a 2.7% CAGR from 2024 to 2029 — a rate on par with the global devices market.

Over the last several quarters, vendors such as Apple and HP Inc. have reported China as being a particularly weak market for their devices businesses due to persistent softness in demand.

TBR expects that among the vendors included in this forecast, Lenovo will reap the greatest benefit from recovering PC demand in China due to its already large market share and its AI PC strategy in the country. In May 2024 Lenovo rolled out a lineup of devices in the country it dubbed its “five-feature” AI PCs, including a personal agent and local large language model (LLM). The company reported strong initial uptake of these devices during its 2Q24 and 3Q24 earnings calls, and TBR expects ongoing momentum in China will help drive Lenovo’s PC segment and top-line growth throughout the forecast period.

TBR Spotlight Reports represent an excerpt of TBR’s full subscription research. Full reports and the complete data sets that underpin benchmarks, market forecasts and ecosystem reports are available as part of TBR’s subscription service. Click here to receive all new Spotlight Reports in your inbox.

Post updated: Nov. 15, 2025

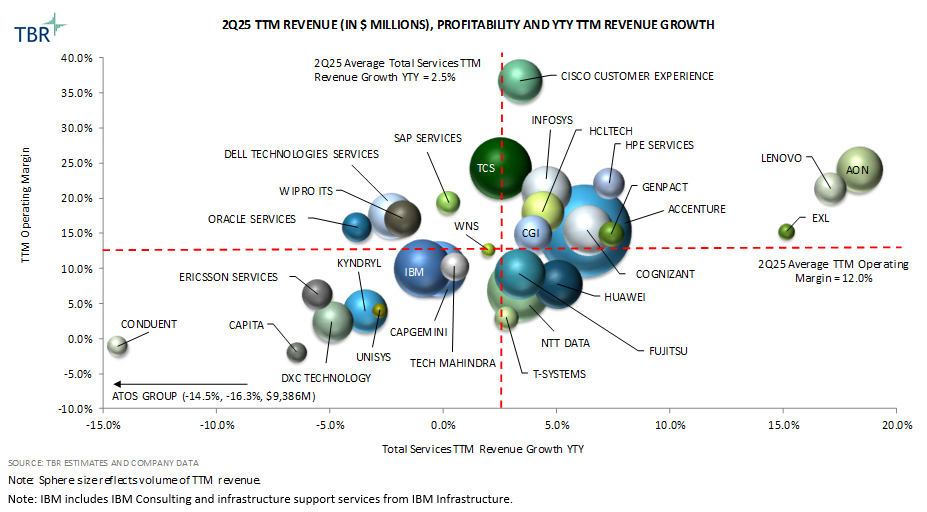

A rebound in financial services and activities around improving productivity and optimizing costs drove revenue performance for IT services vendors during 2Q25

Outlook: TBR estimates trailing 12-month (TTM) revenue growth for the benchmarked IT services vendors will be 2.6% year-to-year in 2025, higher than 2024 revenue growth of 0.9% year-to-year. The market dynamics have not changed since 3Q23, when the uncertain macroeconomic environment began to pressure discretionary spending and consulting activities while fueling a wave of outsourcing demand around infrastructure and application modernization, productivity improvement and cost optimization. Clients are showing increased interest in large transformational offerings to increase productivity and reduce costs, and this trend is increasing the share of managed services deals in IT services providers’ signings mix. Manufacturing faces ongoing downward pressure in Europe, particularly in the automotive sector, but demand for supply chain optimization and digital transformation continues to fuel growth in the sector globally. Vendors are experiencing a rebound in demand from clients in the financial services sector such as banks seeking to improve customer experience (CX) through the use of agentic AI solutions. Although agency spending and headcount cuts by the Department of Government Efficiency (DOGE) negatively impacted the performance of some IT services providers in the U.S. public sector in 1H25, we expect new consulting opportunities to emerge in the long term around efficiency improvement, including systems enhancement, technology modernization and AI adoption. However, some vendors are warning that solicitations, award activity and adjudications have been slowing and that there will be some challenges in 2H25, and expect that consulting engagements will face increased scrutiny.

Key Vendors: Accenture remained the largest vendor in TBR’s IT Services Vendor Benchmark in terms of revenue and headcount and was No. 7 in TTM revenue growth in 2Q25. Accenture’s relentless execution will help the company maintain stakeholder trust as it enters the next phase of its business model rotation and pursues opportunities with upper-midmarket clients. NTT DATA was No. 2 in TTM revenue and No. 14 in TTM revenue growth in 2Q25. NTT’s recent purchase of the remaining shares of NTT DATA creates uncertainty around NTT DATA’s decentralized structure, which currently includes both domestic and overseas operations and enables NTT DATA to tailor service offerings to specific regional markets. Tata Consultancy Services (TCS), which was No. 3 in TTM revenue and No. 16 in TTM revenue growth in 2Q25, demonstrates a strong commitment to innovation through significant investment in research and development, which has incrementally created valuable intellectual property that supports the company’s cutting-edge platforms and solutions.

Market Overview: TTM IT services revenue grew 2.5% year-to-year in 2Q25, compared to year-to-year increases of 1.6% in 1Q25 and 0.9% in 2Q24. Accelerated momentum in financial services and activities around IT modernization and efficiency improvement enabled vendors to alleviate pressures from tight discretionary spending and extended buyer decision cycles. Vendors were able to stabilize profitability in 2Q25, with 20 of the 31 benchmarked vendors improving TTM operating margins year-to-year due to tight expense management, productivity initiatives and stable utilization, and increased use of automation, generative AI (GenAI) and agentic AI solutions.

If you believe you have access to the full research via your employer’s enterprise license or would like to learn how to access the full research, click the Access Research button.

Solutions enabled by technology partner capabilities increase IT services providers’ value proposition around addressing specific infrastructure, operational and business challenges

Quarterly focus: Alliances

TBR Assessment: According to TBR’s 2Q25 Cloud Ecosystem Report, “Enterprise buyers are becoming increasingly conflicted in their expectations of how vendors can best support their technology needs. … In a nutshell, vendors cannot rely on a one-size-fits-all AI ecosystem strategy across regions. Success will require region-specific approaches: IP-led initiatives in APAC, orchestration frameworks in Europe, and startup-centric marketplaces in the Americas. All must be underpinned by interoperable APIs and strong governance to help IT services providers capture and monetize local demand. Executing against such expectations while continuing to rely on a traditional labor-arbitrage model will test professional services firms’ readiness to transform their own operations while maintaining trust with hyperscalers, which continue to explore the opportunity to drive professional services revenue by simplifying the sales process and marketplace through the use of agentic AI.”

Examples of recent vendor activities

IBM is expanding activities with technology providers to augment its cloud and AI capabilities and support clients through all stages of transformation and optimization. Since April IBM has expanded its relationships with Microsoft, Amazon Web Services (AWS), Oracle, Salesforce and SAP. IBM Consulting established a Microsoft practice with 33,000 certified experts dedicated to technologies such as Azure OpenAI, Azure Cloud, Copilot, Fabric and Sentinel. IBM, which has approximately 12,000 AWS-trained professionals, introduced tools and frameworks for building and managing AI agents and integrating them with technologies available on the AWS Marketplace. IBM Consulting is providing AI Integration Services to help clients establish agentic AI capabilities and is offering the IBM Consulting Advantage solution to transform processes through agentic AI on AWS. IBM and Oracle provide agentic AI and hybrid cloud solutions by bringing IBM watsonx to Oracle Cloud Infrastructure. IBM, which has more than 10,000 dedicated Oracle consultants, is expanding its consulting services to enable the use of AI agents across platforms and transform business processes. IBM has more than 7,000 Salesforce-certified professionals and is developing its Salesforce capabilities by introducing AI agents based on IBM watsonx Orchestrate that work with Salesforce technologies and IBM Granite models. IBM has more than 18,000 SAP-certified consultants and, together with SAP, launched a hyperscaler option for moving SAP S/4HANA workloads from on-premises IBM Power servers to the cloud.

Although client trust wavered in the past several quarters due to uncertainty around Atos Group’s transformation, the company received stable support from its technology partners, which will drive portfolio expansion and position the company for growth. In July Atos Group was awarded the Golden Certificate from SAP and was certified for the 10th consecutive time as a SAP Global Operations Partner. The award reflects Atos Group’s dedication to its partnership with SAP, which has spanned more than 20 years, and established managed services capabilities with over 10,000 professionals with SAP expertise. Also in July, Atos Group renewed its status as a Google Cloud Managed Service Provider, driven by capabilities around providing cloud-native services, infrastructure solutions and digital modernization. In April Atos Group received Microsoft’s Private Cloud Solution Partner Designation due to its track record of providing Azure Cloud in data centers globally. Expanding capabilities around Google Cloud and Microsoft diversifies Atos Group’s infrastructure services capabilities and creates opportunities for growth outside of commoditized and low-growth traditional infrastructure services segments. Over the past several years the company has been decreasing its dependency on legacy infrastructure services and reviewing and exiting low-growth and low-margin contracts in the segment.ications strengthens Cognizant’s Neuro AI platform.

Although managed services activities contributed to an acceleration in 2Q25 overall TTM revenue growth year-to-year, 15 of the 31 benchmarked vendors ranked below the average

Trailing 12-month Revenue , Profitability and Year-to-year Trailing 12-month Revenue Growth for Benchmarked IT Services Vendors (Source: TBR)

Vendor spotlight excerpt

Accenture pursues new revenue growth opportunities with upper-midmarket clients, while TCS leverages its cloud and AI expertise and solutions to pull long-term managed services deals

Key Findings and TBR Assessment

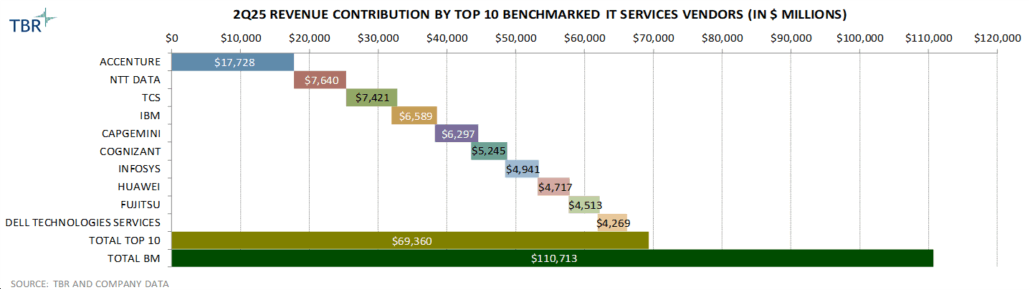

Accenture, NTT DATA and TCS retained their No. 1, No. 2 and No. 3 revenue contribution positions, respectively, compared to 1Q25. Vendors will be challenged to maintain sales growth momentum in 2026 as Accenture navigates macroeconomic headwinds and internal operating model adjustments. Building a pipeline in the midmarket will gradually augment Accenture’s performance. TCS leverages its scale and cost-efficient global talent to offer flexible, competitive pricing, which will be a key advantage as clients scrutinize budgets during uncertain economic times.

IBM moved up from No. 5 to No. 4, Capgemini rose from No. 6 to No. 5, and Fujitsu dropped from No. 4 to No. 9. Although IBM Consulting’s revenue growth has been negatively impacted by clients’ extended decision making, the business continues to benefit from clients’ emphasis on cost-efficient, high-impact technology investments. Pursuing opportunities in the public sector in Europe, specifically in the defense subsegment and around sovereignty solutions, will positively affect Capgemini’s revenue expansion in 2H25.

Cognizant and Infosys each moved up by one position, to No. 6 and No. 7, respectively, compared to 1Q25. Cognizant is capturing opportunities in vendor consolidation, cost reduction and efficiency improvements, and is leveraging its AI expertise and Neuro AI platform to effectively win new projects with existing clients. Infosys is deploying industry-centric, cloud-ready, GenAI-enabled services and solutions within established IT buyer relationships while also relying on customer-zero use cases.

Revenue Contribution by Top 10 Benchmarked IT Services Vendors (Source: TBR)

Revenue segment views excerpt

C&SI revenue growth year-to-year accelerated from 2Q24 to 2Q25, indicating clients are becoming more open to signing discretionary funded engagements

C&SI: Although discretionary spending remained tight, some of the IT services providers saw pockets of growth in C&SI in 2Q25, leading to an increase in C&SI revenue share and revenue growth year-to-year acceleration compared to 2Q24. Portfolio development, client relationship building and skills development to drive transformational engagements aided revenue performance in 2Q25. For example, Accenture is partnering with Deloitte and Korn Ferry to support Saudi Aramco’s employee experience transformation program using LearnVantage capabilities. Capgemini is working with GN Hearing to improve the company’s customer experience and order processing by implementing a Salesforce global order management system.

BPO: Vendors’ BPO businesses continue to benefit from the ongoing shift in buyer priorities from innovation and growth to business resiliency and optimization. Automation, GenAI and agentic AI capabilities within BPO will shift vendors’ service delivery models and generate productivity improvements; however, GenAI and agentic AI threaten the core value proposition centered on human-backed service delivery. IBM Consulting will combine AI Integration Services with capabilities from its partner ecosystem to enable clients to reengineer business processes, improve the user experience, and orchestrate systems comprising AI assistants, agents and data.

Application outsourcing (AO): Application outsourcing revenue growth accelerated year-to-year to 2Q24. Enterprise applications are core to broader digital transformation engagements and create expansion opportunities for vendors. Preparing clients’ applications and data streams for cloud and AI integration continues to fuel managed application services opportunities.

IT outsourcing (ITO): Integration of new infrastructure, enabled by vendors’ cloud and consulting practices, provides a natural starting point for companies to build their managed services pipeline. Demand for IT optimization and IT operations efficiency through AI and automation, and security services continues to fuel ITO revenue opportunities. For example, in July Atos Group renewed its status as a Google Cloud Managed Service Provider due to its capabilities around delivering cloud-native services, scalable infrastructure solutions and digital modernization to enterprises globally through advanced support, optimization and AI-driven management of Google Cloud environments.

TBR Spotlight Reports represent an excerpt of TBR’s full subscription research. Full reports and the complete data sets that underpin benchmarks, market forecasts and ecosystem reports are available as part of TBR’s subscription service. Click here to receive all new Spotlight Reports in your inbox.

Vendors lead with the data lake architecture and emerging frameworks to sell a message of data intelligence amid rampant GenAI adoption

The race for Apache Iceberg mindshare is on

Data lakes remain a valuable way for enterprises to simultaneously store structured and unstructured data, particularly as the latter increases due to generative AI (GenAI) and large language models (LLMs). Data lakes are also directly attributable to the rising popularity of Apache Iceberg, an open-source format regarded by developers for its ability to store data in tables and freely move that data across any data lake architecture.

Whether a customer is creating their own data lake (e.g., on Amazon Web Services [AWS]) or deploying a data lake platform as a product (e.g., Databricks), Iceberg is playing an increasingly larger role in helping customers navigate their big data estates with the most limited vendor lock-in.

How the two data lake giants — Snowflake and Databricks — are investing best speaks to the budding role of Apache Iceberg and its growing community. Earlier this year Snowflake adopted Apache Iceberg as the native format for its platform and subsequently launched Polaris, a tool that allows customers to catalog that data stored in Iceberg tables.

In only a matter of days, Databricks, which was born out of Delta Lake, an Apache Iceberg alternative, moved into the space with its acquisition of Tabular. Tabular was created by the founders of Apache Iceberg, marginalizing Snowflake’s recent investments and intent to attract more Iceberg-heavy users, which generally include digital and cloud-native companies. The hyperscalers, primarily AWS and Microsoft, work closely with Snowflake and Databricks and benefit from their respective integrations to boost interoperability for joint customers through Iceberg.

For example, Microsoft announced its data platform Fabric, which is based on a data lake architecture (OneLake), will support Iceberg via Snowflake. This is a major win for Snowflake that elevates the company’s role as an ISV partner in the Microsoft Fabric ecosystem and further challenges Databricks, which due to its native first-party integration with Azure, has always had a rich and unique relationship with Microsoft.

A select number of vendors are leading the shift to data intelligence

Though somewhat influenced by a degree of marketing hype vendors use to differentiate themselves, data intelligence has become an emerging topic in the market, led by GenAI. At its core data intelligence refers to the use of AI on data to deliver insights tailored to the business, but the other core component of data intelligence is the underlying data architecture foundation.

Databricks is largely associated with formalizing the concept of data intelligence and even markets its platform as the Data Intelligence Platform to convey the value of having both the data lakehouse architecture and the AI components (in Databrick’s case, Mosaic AI) that allow customers to build, train and fine-tune models. Other vendors have similarly adapted their messaging around data intelligence.

For example, as part of what it now calls its Data Intelligence vision, Oracle Analytics announced Intelligent Data Lake, a reworking of existing OCI (Oracle Cloud Infrastructure) services like cataloging and integration, to create a single abstraction layer that will support both Apache Iceberg and Delta Lake formats.

If you believe you have access to the full research via your employer’s enterprise license or would like to learn how to access the full research, click the Access Research button.

Hyperscalers are taking different approaches to address the symbiotic relationship between data architecture and AI

Microsoft and Google Cloud are integrating and productizing their data services as complete solutions, exposing a lack of maturity in AWS’ fragmented approach

Microsoft made a big move when it launched Fabric, which essentially integrates seven disparate Azure data services — from data warehousing up to analytics — as part of a single platform underpinned by a unified data lake. Today, Fabric has amassed over 14,000 paid customers and a growing ecosystem of global systems integrators (GSIs) and ISVs building and selling applications on top of the platform.

Google Cloud, which has always had a strong play in data analytics, is trying to better unify key data and analytics capabilities in BigQuery to deliver a more complete, single-product experience. This includes BigLake, Google Cloud’s storage abstraction layer and services like Dataplex, so customers can apply governance tasks like lineage and profiling in Dataplex without having to leave the BigQuery interface.

Though Google Cloud’s approach may lack the level of integration compared to Microsoft Fabric, it is clear to see the direction the company is heading to help customers simplify their data estates, and ultimately capture more analytics and AI workloads.

AWS’ approach is different. Though offering the broadest set of data tools and services, from storage and ingestion up to governance, AWS is still lacking the platform mindset and strategy of its peers.

To be fair, the company has been working to better integrate services within its own ecosystem by improving data sharing between the operational database and the data warehouse (e.g., “zero-ETL” integration between Aurora and Redshift), but customers continue to stress that they have to take on more burden in the back end when crafting a data architecture on AWS.

This dynamic only reinforces the importance of AWS’ partnerships with complete data cloud platforms like Snowflake and Databricks, but of course Microsoft is also making sure it keeps these companies elevated within the Fabric ecosystem.

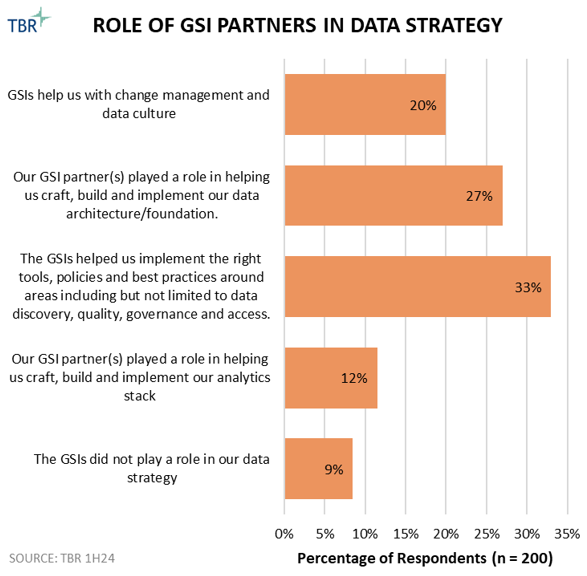

The GSIs are playing a prominent role in multiple facets of data, which could speak to maturing ecosystems and hyperscalers’ efforts to productize the entire data life cycle

Customers indicated that the GSIs play a prominent role in all aspects of the data strategy from change management to data architecture to governance. Just 12% of respondents say the GSIs were involved in their analytics stack, but this seemingly low percentage could be for many different reasons.

First, establishing the data architecture, or re-architecting disparate IT assets, such as data warehouses, is top of mind for many customers right now as they recognize it is a necessary step in GenAI deployment.

Secondly, the hyperscalers and pure play data platform companies are becoming more adept at delivering integrated solutions that deliver upper-stack capabilities, such as analytics based on a holistic data lake architecture. Microsoft Fabric, which has a growing ecosystem of both GSI and ISV partners, is a top example.

TBR’s newly launched Voice of the Partner Ecosystem Report found that cloud providers expect data strategy and management to be the biggest growth area coming from partners over the next two years. In fact, data strategy and management ranked higher than GenAI on its own, which is telling of what the cloud providers expect from their partners.

Role of GSI Partners in Data Strategy (Source: TBR 1H24)

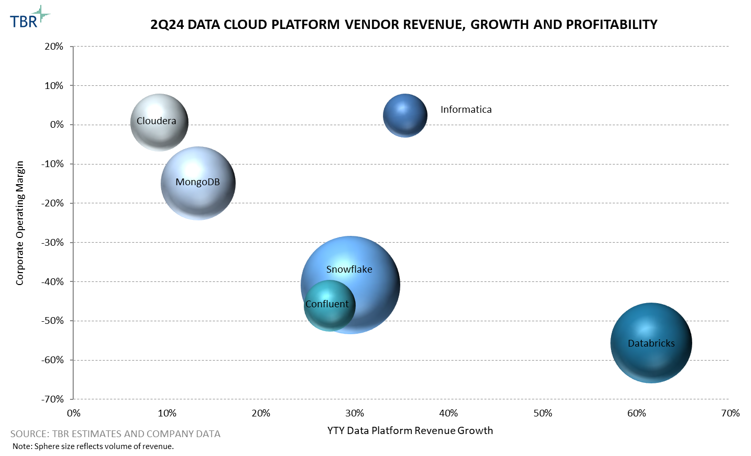

Though Informatica’s cloud-first vision will erode lucrative license and support revenue streams, the company is showing early signs in its ability to expand margins

Despite no longer selling perpetual licenses and actively migrating its support base to Information Data Management Cloud (IDMC) in the cloud, Informatica’s gross margins continue to expand.

Meanwhile, GAAP operating margin increased over 300 basis points year-to-year in 2Q24 as Informatica continues to benefit from economies of scale, and sign larger, more strategic contracts with customers.

Recognizing that it is navigating a highly competitive landscape, Snowflake’s investments in R&D are increasing. For context, Snowflake’s R&D accounts for a notable 50% of total revenue.

2Q24 Data Cloud Platform Revenue, Growth and Profitability (Source: TBR)

https://tbri.com/wp-content/uploads/2025/04/TBR-Spotlight-Report.png10801080TBRhttps://tbri.com/wp-content/uploads/2021/09/TBR-Insight-Center-Logo.pngTBR2025-04-03 09:52:172025-04-03 09:52:171H24 Cloud Data Services Market Landscape

The Trump administration and its Department of Government Efficiency (DOGE) have generated massive upheaval across the board in federal operations, including in the federal IT segment. As of March 2025, thousands of contracts described by DOGE as “non-mission critical” have been canceled, including some across the federal IT and professional services landscape. TBR’s DOGE Federal IT Vendor Impact Series explores vendor-specific DOGE-related developments and impacts on earnings performance. Click here to receive upcoming series blogs in your inbox as soon as they’ve published.

AFS navigates DOGE disruptions: Strong 1Q25 growth amid federal IT spending cuts

Accenture Federal Services’ parent company, Accenture, released its 1Q25 (FY2Q25) earnings March 20, which included some details, albeit limited, about the impact DOGE’s cuts have had on the company’s $5-plus billion federal subsidiary. Although TBR estimates AFS’ quarterly sales in 1Q25 were $1.44 billion, up 18.3% year-to-year on a statutory basis and 7.6% on an organic basis (excluding the impact of the 2Q24 Cognosante acquisition), Accenture CEO Julie Sweet was careful to note during the company’s 1Q25 earnings call that AFS experienced delayed procurement cycles, particularly on net-new programs, during the quarter. That said, AFS’ estimated 1Q25 sales remained in line with TBR expectations.

TBR had projected AFS’ 1Q25 quarterly revenue would fall between $1.40 billion and $1.55 billion, implying statutory year-to-year growth of between 14.7% and 27.0% and organic year-to-year growth of between 4.0% and 16.3%. By TBR estimates, AFS achieved double-digit top-line organic growth in four of the six quarters between 4Q23 and 1Q25, and organic growth of at least 9% in the other two quarters. We anticipated the slowdown in AFS’ organic growth in 1Q25 but did not factor any DOGE-related impacts into our calculations.

All indications from the cohort of federal systems integrators (FSIs) tracked by TBR, as well as anecdotes from our secondary research, suggested that federal IT spending would begin to naturally cool down in federal fiscal year 2025 (FFY25) after a four-year bull market featuring unprecedented expansion of federal IT budgets and growth on behalf of the FSIs. After all, what goes up must eventually come down, but we could not have fully predicted or quantified the early impact of DOGE on AFS or the broader federal market.

TBR believes DOGE canceled nearly $93 million in potential AFS revenue across 10 DOE task orders

Sweet did not mention any specific programs culled from AFS’ book of business by DOGE’s cost-cutting actions. However, TBR is aware that in 1Q25, DOGE canceled 10 task orders on the U.S. Department of Energy’s (DOE) Chief Information Officer Business Operations Support Services 2.0 (CBOSS 2.0) blanket purchase agreement (BPA) for IT modernization and business process services. AFS was the incumbent on the first iteration of the program, CBOSS 1.0, winning the contract with the DOE in 2018.

AFS also secured the $3.5 billion, seven-plus-year recompete on CBOSS 2.0 in January 2025 to continue providing IT support solutions and technology and advisory services around security strategy, operations and environmental management. After AFS won this recompete, Booz Allen Hamilton (BAH) and Leidos protested, prompting the DOE to reconsider the award and review AFS’ winning bid and subsequently leaving a major deal win on AFS’ books in protest limbo. However, we do not believe the challenge by BAH and Leidos was related in any way to the 10 canceled task orders or to DOGE.

The full impact of the 10 canceled task orders on AFS remains unclear, but TBR’s secondary research indicates the terminated work has a total contract value (TCV) of nearly $93 million, including a $35 million order from DOE’s CIO office and a $2 million order for geospatial services. If we assume all $93 million worth of orders was booked by AFS as the prime awardee, that sum would represent just under 2% of AFS’ estimated FY24 revenue of $5.4 billion.

According to TBR’s 1H25 Accenture Federal Services Vendor Profile, “We estimate Cognosante will add up to $400 million in annualized, acquired revenue to AFS’ top line after the acquisition is fully integrated in 1Q25.” Cognosante vastly enhanced AFS’ cloud migration, program management and platforms for federal IT health agencies. Acquiring Cognosante also expanded AFS’ footprint within the Centers for Medicare and Medicaid Services (CMS) and the Department of Veterans Affairs (VA). With Cognosante fully integrated as of 2Q25, and with no additional acquisitions assumed or expected in the company’s FY25 (though we believe M&A is under consideration by AFS and the other leading FSIs to offset near-term DOGE-related growth headwinds), TBR had projected AFS’ FY25 revenue would be between $5.76 billion and $5.87 billion, up between 6% and 8% on both a statutory and organic basis, at least prior to any DOGE-related impact.

If all $93 million in TCV for the 10 canceled CBOSS 2.0 task orders were erased from AFS’ order book, it would reduce AFS’ projected growth to between 4% and 5.5% in FY25 (assuming no other exogenous DOGE-related impacts or unexpected internal impediments to FY25 top-line growth). For context, we estimate that AFS realized double-digit year-to-year organic growth in nine of the 17 quarters between 1Q21 and 1Q25, with estimated organic growth of at least 5% in the other eight quarters.

AFS faces $75 million in additional cuts outside CBOSS 2.0

The General Service Administration (GSA) will continue to review the contracts held by AFS and nine other companies* the Trump administration instructed DOGE to initially target in an effort to cut $65 billion in consulting fees the federal government is set to pay in FFY25 and future years. According to the “DOGE-Terminated Contracts Tracker” on the GX2 website, which tracks developments in federal contracting, AFS has had a total of $75 million in contracts terminated by DOGE as of the publishing of this blog (the CBOSS 2.0 program was not among the listed cancellations).

Cancelled awards were with the Department of Agriculture, Department of the Interior, Social Security Administration (SSA), Department of the Treasury, Department of Homeland Security (DHS), Department of Education, and Department of Health & Human Services (HHS, which houses CMS).

Of the more than $16.2 billion in TCV (8,373 contracts) listed as canceled on GX2’s DOGE-Terminated Contracts Tracker, over $2.8 billion (624 individual contracts) was awarded by HHS and $1.75 billion (420 individual contracts) was awarded by the VA. If DOGE’s contract terminations continue to fall disproportionately on federal healthcare agencies, AFS may not realize the full expected value of the Cognosante acquisition and top-line growth at one of the perennial growth leaders in TBR’s Federal IT Services Benchmark since the COVID-19 pandemic will be stunted in FY25.

Sweet reemphasized in the company’s 1Q25 earnings call that Accenture believes its “work for federal clients is mission-critical,” but TBR is unsure if this will be sufficient to protect AFS’ revenue base from a major disruption in FY25 and FY26. Conversely, Sweet also mentioned, “We see major opportunities over time for us to help consolidate, modernize and reinvent the federal government to drive a whole new level of efficiency.”

AFS pivots to emphasize mission-critical offerings and efficiencies

We believe AFS will pursue new, longer-term opportunities in this shifting federal IT environment by emphasizing its ability to scale cloud, data and generative AI (GenAI)-based solutions agencywide to generate efficiencies, as demanded by DOGE and the Trump administration. AFS will focus on maximizing speed to solution and clearly demonstrating program ROI to prove its offerings are, in fact, mission-critical.

We also expect AFS to double down on advisory services related to resource management, cultural and operational change management, and risk management — critical precursors to federal digital transformations. AFS’ previous investments in AI-enhanced service delivery will be a significant advantage compared to its peers with less mature internal AI capabilities, enabling AFS to showcase how its internal application of AI technologies has optimized operations. AFS’ AI-enhanced service delivery will also enable the company to generate more cost-competitive bids and meet increasingly aggressive IT project timelines for federal digital IT modernization programs.

*BAH, CGI Federal, Deloitte Consulting, General Dynamics IT (GDIT), Guidehouse, HII Mission Technologies, IBM, Leidos and SAIC

We may request cookies to be set on your device. We use cookies to let us know when you visit our websites, how you interact with us, to enrich your user experience, and to customize your relationship with our website.

Click on the different category headings to find out more. You can also change some of your preferences. Note that blocking some types of cookies may impact your experience on our websites and the services we are able to offer.

Essential Website Cookies

These cookies are strictly necessary to provide you with services available through our website and to use some of its features.

Because these cookies are strictly necessary to deliver the website, refusing them will have impact how our site functions. You always can block or delete cookies by changing your browser settings and force blocking all cookies on this website. But this will always prompt you to accept/refuse cookies when revisiting our site.

We fully respect if you want to refuse cookies but to avoid asking you again and again kindly allow us to store a cookie for that. You are free to opt out any time or opt in for other cookies to get a better experience. If you refuse cookies we will remove all set cookies in our domain.

We provide you with a list of stored cookies on your computer in our domain so you can check what we stored. Due to security reasons we are not able to show or modify cookies from other domains. You can check these in your browser security settings.

Other external services

We also use different external services like Google Webfonts, Google Maps, and external Video providers. Since these providers may collect personal data like your IP address we allow you to block them here. Please be aware that this might heavily reduce the functionality and appearance of our site. Changes will take effect once you reload the page.

Google Webfont Settings:

Google Map Settings:

Google reCaptcha Settings:

Vimeo and Youtube video embeds:

Privacy Policy

You can read about our cookies and privacy settings in detail on our Privacy Policy Page.