Technology Business Research, Inc.

Technology Business Research, Inc.3Q24 Federal IT Services Benchmark

TBR Spotlight Reports represent an excerpt of TBR’s full subscription research. Full reports and the complete data sets that underpin benchmarks, market forecasts and ecosystem reports are available as part of TBR’s subscription service. Click here to receive all new Spotlight Reports in your inbox.

Expansion accelerated in the federal IT market in 3Q24 as renewed M&A activity by several federal IT vendors augmented strong, stable demand for digitally based IT modernization

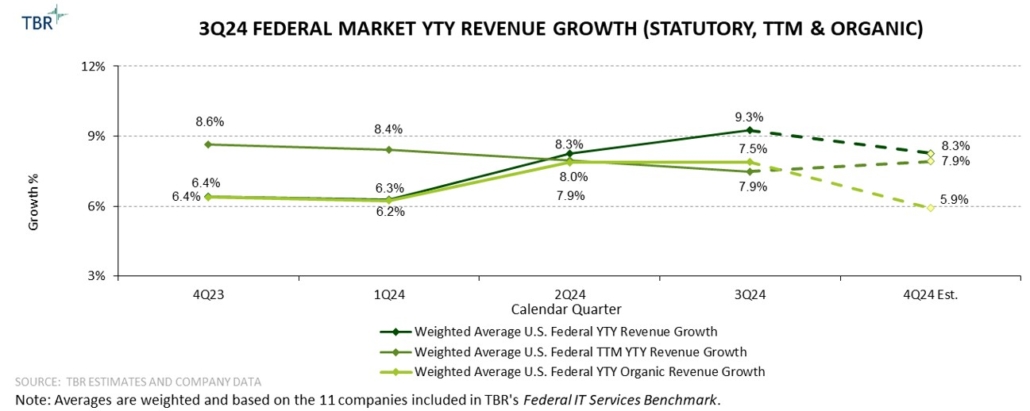

Statutory year-to-year revenue growth for the 11 benchmarked vendors in the U.S. federal market on a weighted average basis rose 100 basis points sequentially, increasing from 8.3% in 2Q24 to 9.3% in 3Q24. Acquisitions by AFS (Cognosante), BAH (PAR Government Systems Corporation [PGSC]), CACI (Quadrint in 1Q24 and Azure Summit Technologies [AST] in 3Q24), CGI Federal (Aeyon), General Dynamics Technologies (Iron EagleX) and KBRWyle (LinQuest) generated an inorganic tailwind to overall market growth of roughly 180 basis points in 3Q24.

Federal IT executives (e.g., CACI CEO John Mengucci) have indicated that the M&A market became more buyer-friendly during 2024, prompting several benchmarked vendors to leverage acquisitions to address portfolio gaps in multiple areas, including digital transformation (DT) and emerging technologies for classified defense and intelligence operations. Vendors have been acquiring, and will continue to hunt for, smaller peers with scalable cloud and digital modernization capabilities as well as deep existing (and likely cloud-related) relationships with federal agencies.

Underpinning inorganic market growth is enduring robust demand for digitally transformative technologies in AI, cloud, analytics and data science, as well as the continued need to upgrade baseline IT infrastructures across the federal sector to accommodate digital modernization.

3Q24 Federal Market Year-to-year Growth (Source: TBR)

Civil agencies continue to aggressively invest in cybersecurity, health IT and Agile-based software systems, leading to sustained double-digit civil sector IT spending growth

Weighted average growth in the civilian sector accelerated 80 basis points sequentially, rising from 9.6% in 2Q24 to 10.4% in 3Q24. Vendors including BAH and Leidos have posted multiple quarters of double-digit growth in their respective civil units as of 3Q24, with robust rates of growth expected to persist well into 2025. Sector growth was sustained at or near 10% throughout federal fiscal year 2024 (FFY24) as demand among civil agencies remains robust for comprehensive zero-trust and cyber incident support solutions, particularly by the U.S. Department of Homeland Security (DHS), the Department of Health and Human Services (HHS), the IRS and NASA.

Attracting and retaining cybersecurity talent also remain top priorities for nearly all civilian agencies, which are tapping vendors like AFS, BAH and Deloitte Federal for human resource advisory services. NASA launched an eight-year, $2 billion program, NASA Consolidated Applications and Platform Services (NCAPS), during 3Q24 to develop and deploy Agile-based software for over 200 IT systems, with vendors including CACI among the primary awardees.

Health IT is generating new revenue and profit streams for the benchmarked vendors, and agencies including the HHS (and its subagencies, CMS, the CDC and NIH) are seeking agencywide AI and analytics adoption services. The top five benchmarked vendors in year-to-year civilian sector revenue growth in 3Q24 were AFS (25%), BAH (16.1%), SAIC (10.8%), Maximus (9.3%) and CACI (7.9%).

Federal IT spending remained robust throughout FFY24, and the market appears poised for another strong year in FFY25, even as CY25 begins with yet another continuing resolution

TBR projects weighted average year-to-year federal IT services revenue growth for the 11 benchmarked companies will decelerate to between 8% and 8.5% in 4Q24, down from 9.3% in 3Q24. We anticipate weighted average year-to-year revenue growth in the defense sector will fall to between 6.8% and 7.3% in 4Q24, down from 8.6% in 3Q24, while civilian revenue growth remains between 10% and 10.5% in 4Q24, in line with the 10.4% increase in 3Q24.

Four leading federal systems integrators — BAH, CACI, Leidos and SAIC — as well as smaller federal IT peer KBRWyle elevated their respective revenue growth forecasts for their current fiscal year when tendering 3Q24 fiscal results, indicators that the federal IT macro environment will remain mostly growth-friendly through FFY25.

The new federal fiscal year began with a continuing resolution (CR) that extended government funding until Dec. 20, when a subsequent CR was enacted to fund federal operations until March 14, 2025. Further CR extensions in FFY25 would cause budget delays that could impede the ability of federal IT contractors to convert backlog into revenue, but most vendors expect revenue growth to remain on a solidly upward growth trajectory in FFY25.

Pressures on resource management teams at federal IT contractors continue easing as the federal technology labor market returns to pre-pandemic rates of employee attrition and retention

Federal IT vendors are expanding training of their workforces across a variety of emerging technologies, including AI, analytics, cloud, EW, SIGINT and communications. The competition for talent in federal IT continues to cool, according to executives at several vendors, who have indicated that current trends in the labor market in federal technology are reminiscent of those seen in 2020. Recruiting and upskilling initiatives at federal IT vendors emphasize skills in AI/GenAI, machine learning and security technologies.

Spotlight on IT and professional services vendors serving the public sector: Resource management

Leidos CFO Chris Cage noted in the company’s 3Q24 earnings discussion that employee retention levels remain at all-time highs, as the federal IT labor market continues to cool after the hyper-competitive, post-pandemic period. BAH CFO Matt Calderone indicated his firm received over 100,000 applications in one month during 3Q24.

Amanda Christian, CACI SVP of Contracts and Subcontracts, is leading an effort to consolidate the company’s finance, accounting, contracts and subcontracts activities to enhance cross-collaboration and improve the company’s already strong win rates on net-new awards and recompetes.

Peraton continued to support Dakota State University’s CybHER Security Institute this summer to encourage young girls to pursue careers in cybersecurity. The company has recently ramped up its efforts to develop a cybersecurity talent pipeline. Peraton has promised to double its related apprenticeships, hire over 200 interns, set up an initiative to help people pivot into cybersecurity, and expand its ties with community colleges over the course of 2024.

Technology Business Research, Inc.

Technology Business Research, Inc. Kentoh, Getty Images Signature

Kentoh, Getty Images Signature