Technology Business Research, Inc.

Technology Business Research, Inc.5G & 6G Telecom Market Landscape

TBR Spotlight Reports represent an excerpt of TBR’s full subscription research. Full reports and the complete data sets that underpin benchmarks, market forecasts and ecosystem reports are available as part of TBR’s subscription service. Click here to receive all new Spotlight Reports in your inbox.

FWA remains the dominant 5G use case

Communication service providers (CSPs) in many countries (developed and developing) globally will leverage 5G FWA to provide competitive high-speed broadband services. CSPs increasingly view 5G FWA as a viable and, in many cases, more cost-effective alternative to traditional fixed broadband services. In many cases, FWA also provides CSPs with a time-to-market advantage versus traditional, fixed-access operators in greenfield environments such as rural areas. According to the June 2025 Ericsson Mobility Report 141 CSPs globally are currently offering 5G FWA services, up from 128 CSPs offering 5G FWA services a year ago.

FWA connection growth will remain robust in the U.S. as T-Mobile and Verizon expect to reach a total of 12 million and up to 9 million customers, respectively, by the end of 2028. FWA development in the U.S. will be aided by factors including new rules for the Broadband Equity, Access and Deployment (BEAD) Program that are more favorable to FWA as well as the establishment of an 800MHz pipeline of midband spectrum under the One Big Beautiful Bill Act, which will create more capacity to support FWA.

Other regions are experiencing significant growth in FWA customers, including Europe and the Middle East and Africa. India is also a prime market for FWA due to its limited broadband infrastructure as Reliance Jio reached 5.6 million 5G FWA connections as of March 2025 and aims to add 1 million new 5G FWA connections monthly.

Investments in 6G are likely to be muted due to uncertain ROI

TBR expects CSPs will be reluctant to invest in large-scale 6G infrastructure deployments when the time comes because they are still struggling to generate a ROI on their 5G investments. CSPs will be focused on monetizing existing 5G investments into the 6G cycle as clear use cases and tangible ROI will need to be evident before 6G is deployed at scale.

The above sentiments were captured by a joint statement issued by the Next Generation Mobile Networks (NGMN) Alliance, a consortium comprised of about 20 global operators as of August. The document includes statements such as the following: “6G standards must be globally harmonised. It is expected to be built upon the features and capabilities introduced with 5G, alongside new capabilities to deliver new services and value. Such technological evolutions should be assessed with respect to their benefits versus their associated impact. 6G standards must learn from the mistakes of 5G, including multiple architecture options, features that are never used and use cases that have no market pull. … The industry needs to develop solutions that have tangible pull from potential customers, as there is increasing concern from operators about the affordability of investment in networks for the sake of technology development.”

TBR believes enterprises are likely to lead in 6G adoption over CSPs as they have more use cases to justify 6G investment, especially in regard to private networks in areas including manufacturing and heavy automation facilities. TBR expects the level of government involvement in the cellular networks domain (via stimulus, R&D support, purchases of 6G solutions and other market-influencing mechanisms) to significantly increase and broaden, as 6G has been short-listed as a technology of national strategic importance.

The commercial deployment of 6G-branded networks will likely begin around 2030 (following the ratification of 3GPP Release 21 standards, which is tentatively slated to be completed by the end of 2028). However, it remains to be seen whether 6G will be a brand only or a legitimate set of truly differentiated features and capabilities that bring broad and significant value to CSPs and the global economy. Either way, the scope of CSPs’ challenges is growing, and governments will need to get involved in a much bigger way to ensure their countries continue to innovate and adopt technologies deemed strategically important.

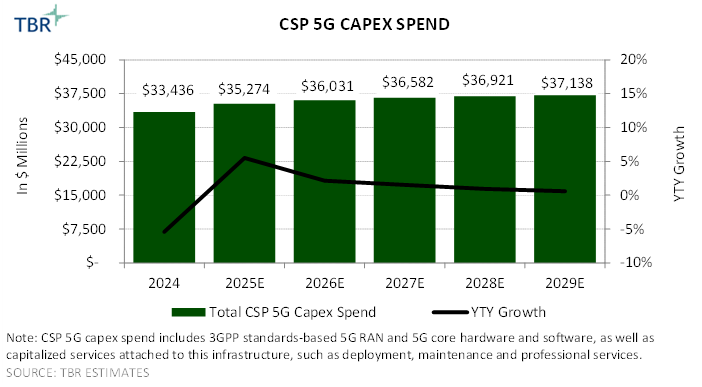

Global CSP spend on 5G infrastructure is growing slowly following a dip in 2024 as CSPs reassess their capital allocation and become more conservative

A pull forward of capex into 2023 in the U.S. and India resulted in a decline in CSP 5G capex in 2024, but slow growth will resume in 2025 as CSPs gradually deploy additional 5G base stations for coverage and capacity as well as roll out 5G SA and 5G-Advanced technologies.

Though some CSPs will continue to test and commercially deploy the newest technologies for 5G, most CSPs are in no rush to deploy 5G SA or 5G-Advanced due to the lack of ROI-positive B2B use cases.

FWA is one key area that will receive increased attention and investment through the forecast period as more CSPs legitimize the technology as an economically viable means of bridging the digital divide and bringing more competitive broadband services to existing markets that have fixed access.

Graph: CSP 5G Capex for 2024-2029Est. (Source: TBR)

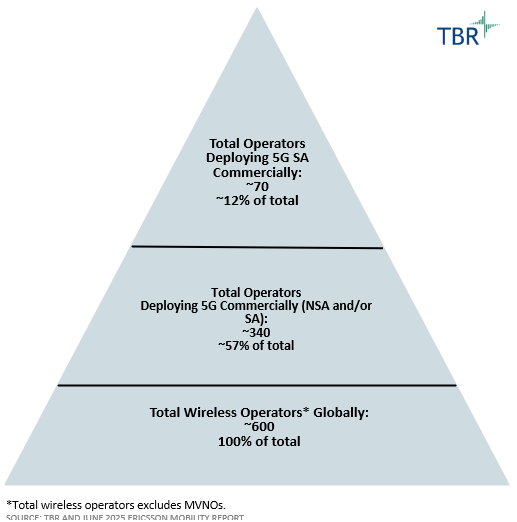

Operators remain slow in their transition to 5G SA, which is limiting revenue opportunities provided by areas including network slicing and 5G-Advanced

A continued lack of 5G SA deployments globally is a main barrier preventing the telecom industry from capturing new areas of value for their networks, such as B2B opportunities, network slicing and network APIs. However, many CSPs are hesitant to migrate to 5G SA due to uncertainty around ROI. According to the June 2025 Ericsson Mobility Report, out of the over 340 CSPs globally that have commercially launched 5G, only around 70, or about 21%, have commercially launched 5G SA so far.

Many CSPs are not in a rush to deploy 5G SA and are comfortable keeping their 5G Non-Standalone (NSA) networks for an extended period. Though 5G SA does provide some optimization benefits, such as throughput improvements to support data traffic increases, versus the NSA framework, many CSPs remain content with 5G NSA pending substantial, ROI-positive use cases that require the technology.

Limited 5G SA adoption will likewise hamper CSPs in implementing 5G-Advanced, which is dependent on 5G SA. Early deployments of 5G-Advanced began in 2024 and gradually expanded in 2025. 5G-Advanced will provide CSPs with benefits including faster data speeds, reduced latency and the ability to support use cases in areas such as AR/VR, edge computing and IoT.

5G Deployment (Source: TBR)

Technology Business Research, Inc.

Technology Business Research, Inc. Technology Business Research, Inc.

Technology Business Research, Inc.