Technology Business Research, Inc.

Technology Business Research, Inc.Are Hyperscalers Really Competing for Services Revenue?

TBR has consistently highlighted hyperscalers’ professional services units, despite their relatively small revenue streams, as potentially credible threats to IT services companies. Hyperscalers do not intend to displace global system integrators (GSIs) in consulting or managed services, but their growing services capabilities create more margin pressure for (and anxiety among) the GSIs each quarter. This report examines where hyperscalers’ professional services units overlap with GSIs’ and how their roles continue to evolve. We begin by comparing the companies’ services operating models.

How hyperscalers work alone

Among the hyperscalers, Amazon Web Services (AWS), Google and Microsoft have their own services units, with AWS having the highest cloud professional services revenue and being the most vocal about its offerings. AWS ProServe (Professional Services) and Amazon Managed Services take tailored approaches and have customer-forward strategies. AWS provides ProServe offerings on AWS Marketplace, making it easier for account teams and customers to procure consulting alongside cloud products.

At the end of 2025, AWS launched the Professional Services Delivery Agent, which changed the workflow for AWS and its clients, making agents the first step, not a consultant-led pilot. Now agents can perform architecture validation, migration planning, code generation and documentation while consultants focus on customer-specific decisions. In comparison, Google Cloud Consulting introduced packaged engagements around new technologies, such as AI Readiness and Agent Launchpad, to help customers reach production quickly before partners scale the deployments.

Microsoft’s professional services practice, which once focused on paid implementation, is moving toward adoption and customer success through services like FastTrack, Unified, and Cloud Solution architects. The introduction of Microsoft Frontier Company could change the dynamic by giving the company a more direct role in helping clients design, deploy and scale agentic AI solutions. The model creates a more comprehensive delivery motion that may resemble AWS’ and Google Cloud’s by taking a more formalized approach to technology, engineering support and consulting around emerging AI workloads.

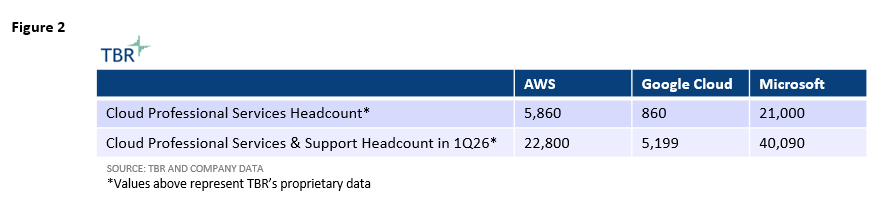

Figure 1 contains TBR’s proprietary data and includes estimates of professional services revenue developed over years of experience covering these companies and the broader IT services market. Microsoft receives the smallest share of revenue from cloud professional services, and this may be part of why the company rebranded its former Microsoft Consulting Services to be included as part of Microsoft Industry Solutions and the broader Microsoft Professional Services unit, which is more closely aligned with the client-facing brands AWS ProServe and Google Cloud Consulting. Microsoft intends to gain higher margins in consulting-related work as part of its broader strategy to become AI-first.

TBR believes Microsoft may be trying to emulate margin leader AWS’ approach in its professional service business. Compared to five years ago, Microsoft’s and Google Cloud’s professional services revenue has been declining as a percentage of total cloud sales. Yet, many vendors are increasingly giving away managed services as a value-add.

As AI matures and repeatable solutions become more attainable, AWS may borrow Microsoft’s and Google Cloud’s more platform-based approach. In addition, repeatable outcomes will make services partners even more important, and they can focus on ecosystem orchestration. Services orchestration of go-to-market motions incorporating emerging solutions indicates that interconnected revenue is rising. Google Cloud saw a 9x combined increase in seats sold with partners and in the number of partners using the application internally in 1Q26. On the GSI side, TBR believes hyperscaler partnerships will become more important and account for a larger share of revenue, as described in TBR’s 1Q26 Accenture report, for example.

Where is the threat to services partners?

Hyperscalers’ services revenue is increasing much more year-to-year than GSIs’. Each of the three hyperscalers’ professional services revenue grew by more than 10% from 2024 to 2025. TBR believes this is due in part to adding services to existing and emerging product lines. Hyperscalers want to ensure customer satisfaction, since it is their AI platform and software on the line, while GSIs remain technology agnostic as their measure of client satisfaction comes from their own services and not the technology products or platforms delivered by the hyperscalers. In addition, hyperscalers also want to obtain more consumption usage around AI.

TBR believes GSIs may be losing ground around adoption and solution-specific implementation engagements. TBR’s Cloud Professional Services Market Forecast 2025-2030, which focuses on a GSI perspective, predicts that hyperscalers “can influence not only how services are delivered but also how outcomes are achieved, strengthening their role in driving client success and increasing their share of the value chain.”

Typically, GSIs are more instrumental in broader transformation and change management engagements that require greater scale and complexity. TBR does not expect these areas of influence to change anytime soon. As discussed in TBR’s 1Q26 Cloud Go-to-market Benchmark, “As [cloud] portfolios shift toward consumption-based and modular pricing, [services] partners play a critical role in driving adoption, expansion and usage discipline, which directly influences lifetime value even when the initial transaction is small.”

In turn, hyperscalers are increasingly relying on GSIs’ large benches. As we also noted in the benchmark, “many AI and platform revenues are usage-based or deferred, while partner services revenue is front-loaded. [Cloud] vendors use incentives to bridge this timing mismatch and keep partners economically engaged even when vendor revenue recognition lags. Essentially, incentives are replacing guaranteed margins, enabling [cloud] vendors to steer partners’ behavior without permanently increasing the ecosystem’s costs, which would happen if they continually added headcount.”

Hyperscalers’ growing influence is affecting which services GSIs offer. Each new frontier model and agent release promises new, exciting potential outcomes across business workflows, security measures and applications. Yet it is up to GSIs to ensure all technology layers are prepared for AI, beyond what hyperscalers’ professional services teams offer. Hyperscalers are more interested in developing advanced solutions and earning more consumption-based revenue.

How are cloud professional services evolving on their own?

Do hyperscalers and GSIs differ in their delivery approaches? Hyperscalers may have more depth in platform-enabled delivery, given their closer proximity to innovation and heavier IP assets. Hyperscalers are not headcount-heavy and thus are motivated to keep headcount in check. AWS’ Professional Services organization is adding AI agents internally, including a Professional Services Delivery Agent, to speed consulting work and reduce delivery costs. More broadly, GSIs are an entry point for multiparty orchestration when clients need packaged repeatable offerings across cloud, services, AI-native and hardware ecosystems. We expect cloud-partner-backed revenue to increase as a share of overall revenue over the second half of the decade. However, multiparty orchestration creates competition for margins. A strong partnership means all parties need to be upfront about pricing expectations and about which engagements are best for each point of contact, the latter of which TBR believes hyperscalers and services vendors are already addressing.

Hyperscalers want to be the first choice of technology providers for basic migration. As such, the three companies are focusing on providing consulting with designated solutions and more defined frameworks. Alongside strong alliance partners, repeatable solutions help hyperscalers keep consistent professional services despite some recent increases in cloud professional services revenue. For example, AWS’ cloud professional services revenue rose an estimated 26.7% from 2024 to 2025, but the company’s professional services headcount grew an estimated 6% year-to-year from 4Q24 to 4Q25. The conservative headcount growth is indicative of hyperscalers staying true to their nature and not becoming a services business. Meanwhile, Google Cloud, which has significantly lower headcount numbers in its professional services unit, may increase hiring or, at the very least, redirect resources to make services headcount more accommodating for effective AI deployment.

Forward-deployed engineers (FDEs) are changing the conversation around services headcount. As the IT market scrambles to accommodate growing client demand for ROI, hyperscalers are introducing FDEs. These professionals are being deployed alongside GSIs’ teams and are gaining headlines, but a deeper look suggests these roles previously existed in some capacity. The FDE model is less a clean break from prior services roles and more of a product- and adoption-oriented version of technical architecture support. FDEs share similarities with systems architects in that both sit close to the client and translate platform capabilities into workable solutions, but FDEs are more tightly linked to implementation and iteration as AI use cases move into production. One example of this is Avanade, the joint venture between Microsoft and Accenture.

The two companies are deploying FDEs together, with a focus on Microsoft’s Frontier Suite. As described in TBR’s 1Q26 Microsoft Cloud report, “The announcement is important because the FDE model, while made prominent by Palantir, has historically been less common among software vendors that prefer more scalable and margin-accretive delivery models. FDEs are expensive because they place technical resources close to the customer, but that proximity becomes more valuable as AI moves from experimentation into mission-critical workflows that require customization, governance and fault tolerance.” Hyperscalers are rebranding existing solutions to highlight their capabilities.

In the newest example, Microsoft has launched the Microsoft Frontier Company and announced a $2.5 billion investment. The company will “embed” 6,000 professionals to design and implement AI solutions, suggesting a more services-forward approach to clients, perhaps similar to AWS’. Although FDEs and related professionals are important and are likely to expand in some capacity, especially in the short term, as technical expertise is necessary for enterprises navigating AI transformation, we believe the build-out will be confined to when AI solutions begin to reach maturity. For now, hyperscalers’ professional services units will stay in their lane, focusing on how their solutions are best built and deployed, leaving the other noise, such as change management and ecosystem orchestration, to the GSIs.