Telecom Edge Compute Market Forecast

TBR Spotlight Reports represent an excerpt of TBR’s full subscription research. Full reports and the complete data sets that underpin benchmarks, market forecasts and ecosystem reports are available as part of TBR’s subscription service. Click here to receive all new Spotlight Reports in your inbox.

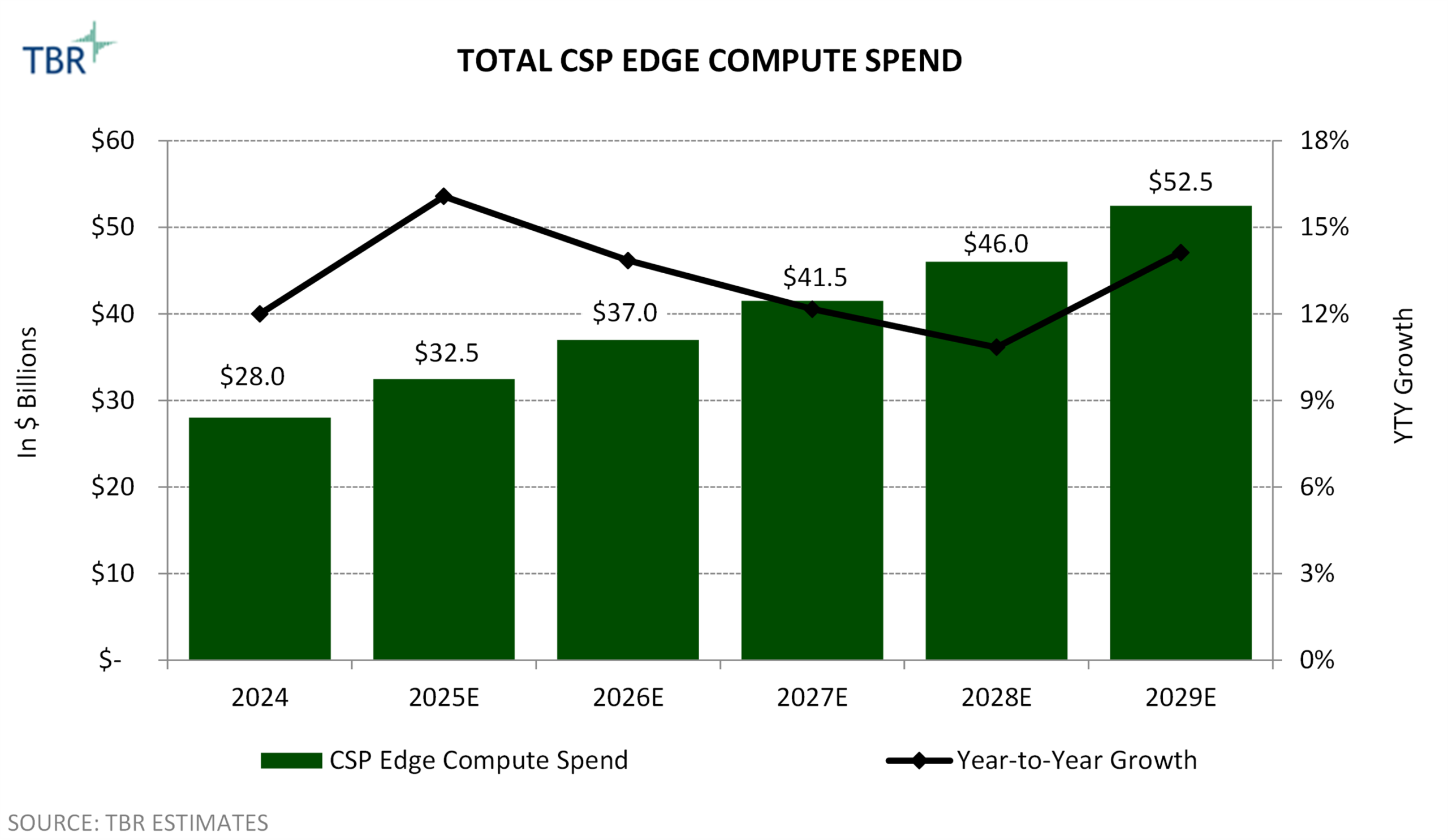

Telco, cableco and hyperscaler spend on edge compute infrastructure will grow at a TBR-projected CAGR of 13.4% from 2024 to 2029 to reach $52.5B

TBR estimates telecom edge compute infrastructure investment will reach $52.5 billion in 2029, driven primarily by network transformation ― especially vRAN deployments ― by telcos and deployments by telcos and hyperscalers eager to extract economic value from AI and other distributed computing use cases.

The edge computing market is developing more slowly than originally expected due to several factors, particularly the lack of proven revenue-generating use cases. Future ROI on edge compute investments is uncertain as opportunities such as monetizing AI inferencing at the edge remain unproven. vRAN, the primary telco use case for edge compute, provides some cost efficiencies but offers limited net-new revenue-generation opportunities.

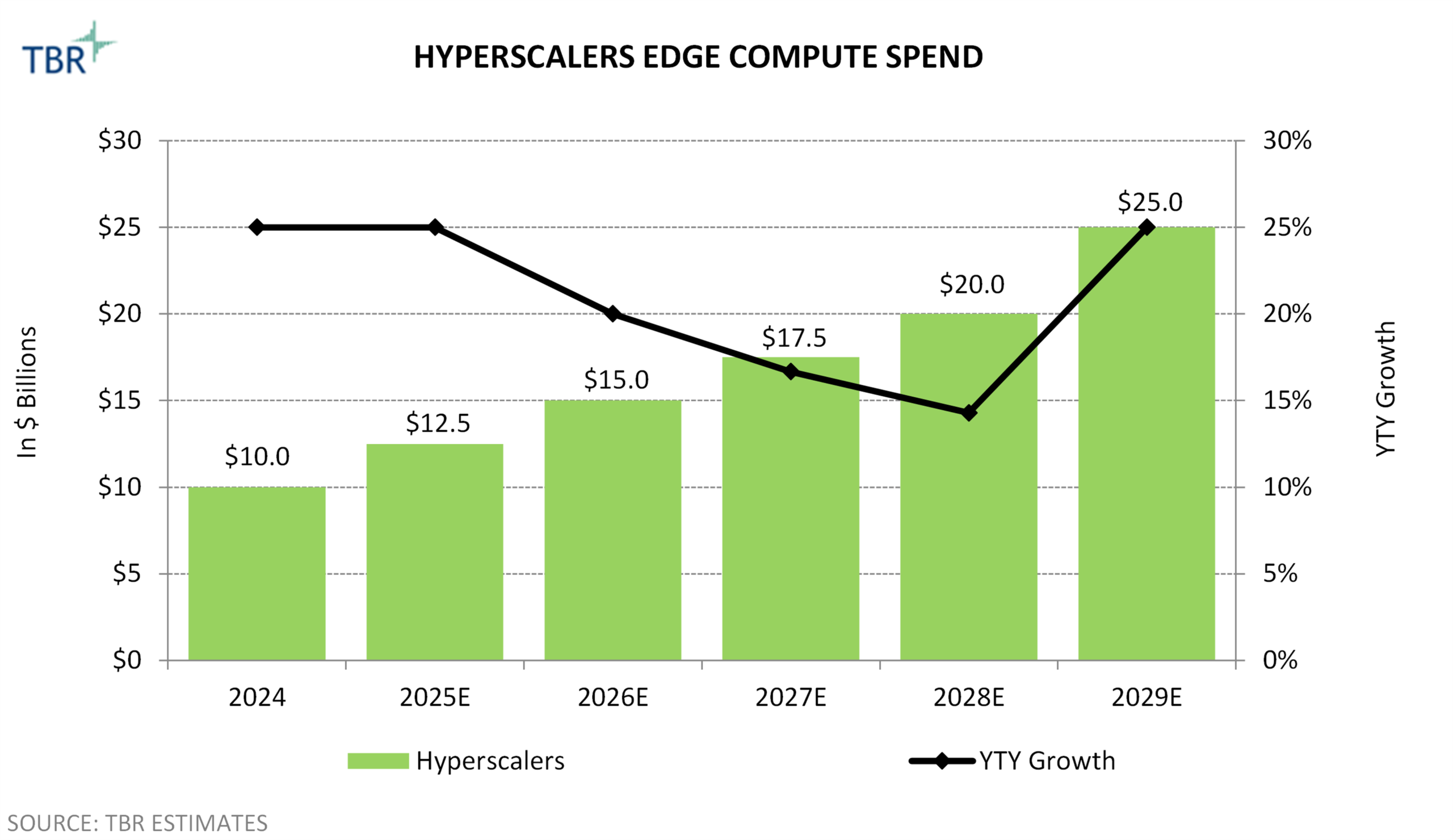

Hyperscaler spend growth will more than double the combined telco and cableco growth during the forecast period, as this cohort will pivot spend from central to edge build-outs to achieve the latency and quality of service that new network use cases will require, as well as to handle AI inferencing workloads.

Hyperscalers deprioritized edge cloud build-outs as they double down on AI training, which drives central data center investment; AI inferencing will leverage edge computing

Though hyperscalers are still increasing investment in edge data centers, their top priority is building out central data centers to train and support their AI models, as central data centers are best suited to support the large amount of power and space GPU servers require to do AI model training; data storage also requires space. Further, hyperscalers require more data center capacity to support their cloud services businesses and new use cases enabled by technologies such as AI.

To mitigate some of the economic and technical challenges associated with building out edge computing infrastructure at scale, hyperscalers intend to leverage key technological innovations in central cloud. For example, hyperscalers are conducting R&D and investing in Arm-based chips (which are more energy-efficient than x86 chips, the predominant chip used in data centers today) as well as in new cooling technologies such as liquid immersion. Hyperscalers are also focused on developing new renewable energy resources and exploring promising technologies such as SMR (small modular reactors) and geothermal to provide a steady stream of energy to power their data centers. TBR expects hyperscalers will leverage most of these innovations in central data centers before incorporating them into edge data centers.

Hyperscalers have been focused on AI training in central data centers, but emphasis will shift to building out edge infrastructure to handle AI inferencing

Hyperscalers are building out their distributed computing and intelligent connectivity infrastructure platforms to capitalize on key use cases such as AR/VR and, more broadly, the digital ecosystem transcendence across key aspects of people’s lives (see TBR’s 2H25 Hyperscaler Digital Ecosystem Market Landscape for more information). Hyperscalers’ end goal is to enable ambient computing. TBR estimates trillions of dollars in economic value will be created by the intersection of distributed computing and intelligent connectivity through this decade, and we believe hyperscalers are positioning to capture an outsized portion of this market opportunity.

TBR believes hyperscaler distributed computing platforms, which encompass central and edge data centers as well as on-device computing, will be leveraged to run the intelligence layer of their respective global networks. For example, cloud-native, virtualized network functions, such as the mobile core, will reside in this distributed computing platform, supporting the transport and access layers of the network.

vRAN supports edge compute spend by CSPs such as Verizon and, until recently, DISH; Telus is the leading CSP in Canada in vRAN investment

Canada-based operators are taking a wait-and-see approach before making significant investments in edge infrastructure. These operators have, however, begun to invest in vRAN — and, more broadly, network transformation via virtualization and cloudification — with Telus making a strong commitment to the technology through an agreement with Samsung reached in February 2024, and Canada-based operators taking part in sovereign cloud efforts via offerings such as Bell AI Fabric.

AT&T, Verizon, Amazon, Microsoft and Google will spend the most on edge infrastructure in North America through the forecast period.

vRAN is the largest edge compute use case for telcos, and Verizon is among the leaders in this space as the company announced it has deployed over 22,900 vRAN sites as of early 2025 in markets across the country. Samsung and Ericsson are rolling out vRAN solutions in Verizon’s C-Band-based 5G network.

Other U.S.-based companies, especially Apple, Meta Platforms, Comcast, Lumen and T-Mobile, are also investing in edge infrastructure but at a lower scale compared to the five aforementioned companies.

DISH has extensively deployed vRAN, though the company is dismantling its mobile access network.

Comcast has spent the most compared to other cablecos on edge infrastructure to date as the operator pushes forward with its network transformation. Other cablecos, such as Charter, Cox, Altice and Liberty Global, are following in Comcast’s footsteps. However, in general, cablecos will lag hyperscalers and telcos in the edge compute opportunity. As of October, Comcast had rolled out over 50,000 edge compute servers and 1,300 vCMTS physical points of deployments.

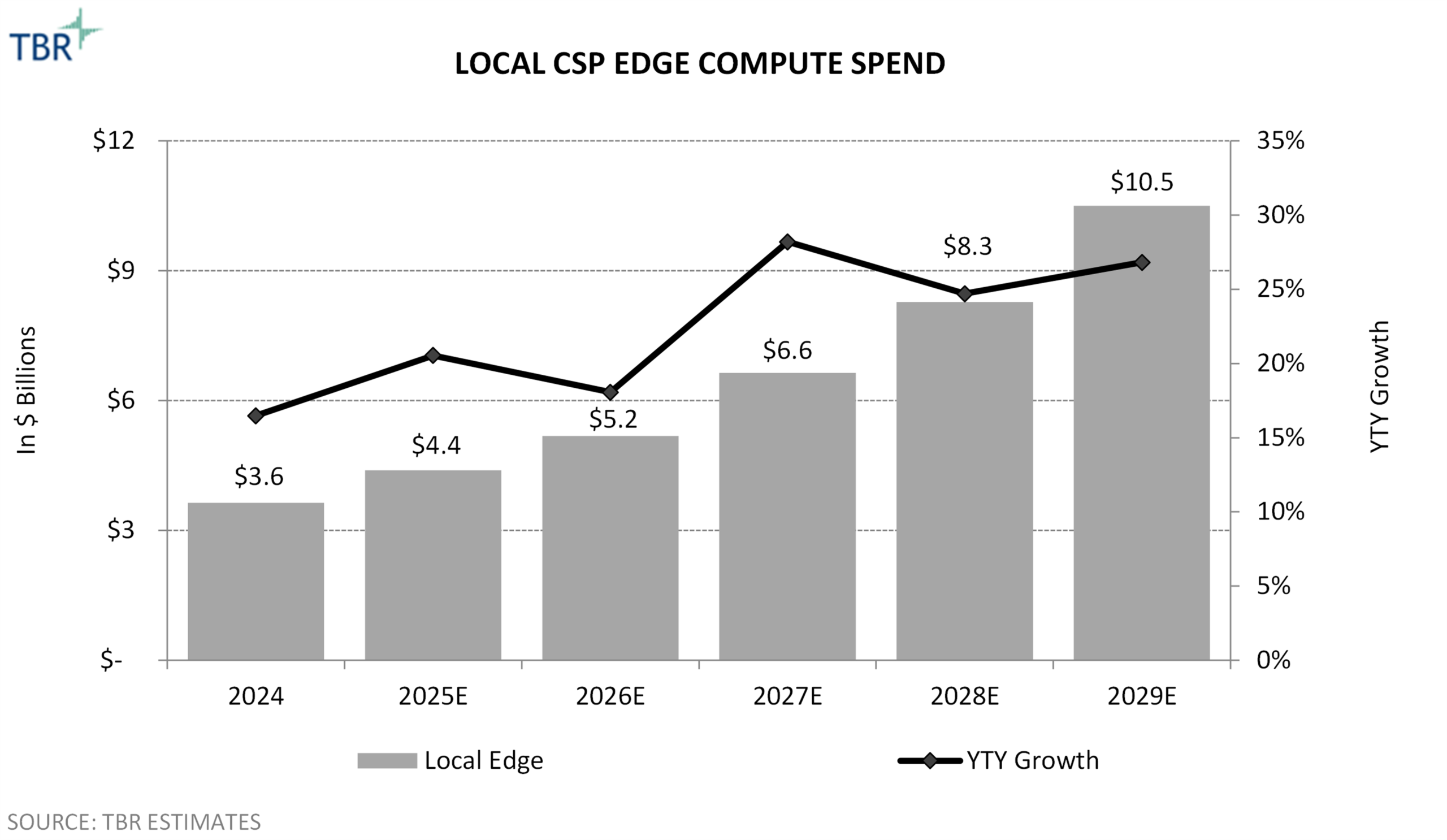

vRAN deployments largely drive local CSP edge compute spend; hyperscaler investment is materializing more slowly than previously anticipated due to a shift in their priorities

vRAN underpins local edge compute spend volume, with support to date provided by rollout initiatives at key operators such as China’s CSPs, Rakuten, Verizon and Japan’s Tier 1 CSPs. The proliferation of vRAN across more CSPs will drive growth during the forecast period.

Tower sites are especially pertinent to edge computing due to their proximity to population areas, availability of power, backhaul and last-mile access, and physical security.

Towercos have not seen the master lease agreements that hyperscalers were expected to sign with strategic shared infrastructure owner (SIO) partners to locate their edge stacks at the base of cell sites materialize at scale as hyperscalers pursue other avenues, such as satellites.

SIOs (such as tower companies, data center colocation providers and neutral host providers) are becoming increasingly important aggregation points for AI-related traffic and connectivity demand. Their facilities often serve as hubs where hyperscalers, neoclouds, enterprises and AI service providers interconnect, driving demand for high-capacity fiber, wavelength services, dark fiber and low-latency metro and long-haul transport. As AI workloads scale and become more distributed, SIOs are influencing where network investment is required and where new interconnection-rich locations emerge within metropolitan and regional markets.

Telcos have largely ceded this opportunity to SIOs because they have been divesting their tower and land assets to generate cash for network equipment, pay down debt, buy more spectrum and fund capex. As such, telcos will increasingly rely on SIOs for locating a portion of their edge sites.