Technology Business Research, Inc.

Technology Business Research, Inc.ServiceNow Ecosystem Report

TBR Spotlight Reports represent an excerpt of TBR’s full subscription research. Full reports and the complete data sets that underpin benchmarks, market forecasts and ecosystem reports are available as part of TBR’s subscription service. Click here to receive all new Spotlight Reports in your inbox.

ServiceNow’s evolving value proposition, centered on seamless tech integration and sales alignment, provides a strong backbone in its alliances’ strategy, appealing to client-mindshare-hungry partners

Key trends

The need to unlock data and break down integration barriers between the back, middle and front office is as relevant as ever as customers look to deploy generative AI (GenAI) within their workflows. Acting as an abstraction layer on top of the enterprise system of record (SOR), ServiceNow is in a strong position to message around business transformation and to have more outcome-based conversations with clients, which is aligned with the IT services companies and consultancies’ business models. IT services companies and consultancies that have experience reducing organizations’ technical debt and implementing systems like SAP, Workday and Salesforce are well positioned to use ServiceNow to deliver added value. As evidenced by ServiceNow’s introduction of consumption-based pricing for AI Agents, ServiceNow is focused on selling value as part of its GenAI portfolio, which is certainly in step with the market, though outcome-based pricing may be something for ServiceNow to consider to further align with the global systems integrator (GSI) ecosystem and stay ahead of its growing list of SaaS competitors.

Go-to-market strategy

As ServiceNow continues to grow and pursue new market opportunities, the company is doing a better job of enabling the ecosystem in both sales and delivery. Unlike some of its SaaS peers, ServiceNow is not as established in the market, underscoring a clear need to leverage partners that have the C-Suite relationships, particularly in the line of business (LOB) that can articulate ServiceNow’s value as it exists alongside core enterprise applications. Despite its rapid expansion into more SaaS markets, ServiceNow remains a platform company at its core, but being a true platform company requires an ecosystem that can build on that platform. We suspect the Build motion, where partners sell custom, often industry-specific offerings they develop on the Now Platform, will be an increasingly critical motion, helping ServiceNow capitalize on opportunities.

Vendors

Given the smaller size, ServiceNow is unsurprisingly among the fastest-growing practice area within the GSIs, with average practice-related revenue up 12.9% year-to-year in 4Q24. Several partners have more than $1 billion commitments with ServiceNow, and in early 2025 Infosys and Cognizant joined their competitors in the Global Elite tier of the ServiceNow Partner Program. Cognizant is also the inaugural partner for ServiceNow’s Workflow Data Fabric platform, a key offering that rounds out ServiceNow’s portfolio, offering zero-copy integrations with key platforms, including Google Cloud and Oracle, to feed ServiceNow’s AI Agents. On the technology side, ServiceNow is also strengthening its partnerships with hyperscalers beyond Microsoft, which could unlock new points of engagement for services partners as they start to embrace the multiparty alliance structure. For example, Deloitte is looking at how it can build agents for ServiceNow-specific use cases, with an immediate focus on the front office, on Google Cloud Platform (GCP), while Accenture included ServiceNow on its partner list for the recently announced Trusted Agent Huddle for agent-to-agent interoperability.

Emergence of multipartner networks will test vendors’ trustworthiness and framework transparency

Prioritizing the needs of partners and enterprise buyers over internal growth aspirations will position vendors across the ICT value chain as leading ecosystem participants. It sounds like an idea born in marketing, but positive digital transformation (DT) outcomes will require multiparty business networks that bring together the value propositions of players across the technology value chain. By leading with their core competencies, players can establish needed trust among partners and customers alike, increasing their competitiveness against other players that have spread themselves too thin with aspirations of being end-to-end DT providers.

To better understand these approaches, we have identified three back-office ecosystem relationship requirements that guide how the parties work together.

TBR Ecosystem Value Chain (Source: TBR)

TBR has identified 4 cloud ecosystem relationship requirements that guide how the parties work together

ServiceNow ecosystem relationship best practices

1.Consider PaaS layer and its role in the SaaS ecosystem: As discussed throughout our research, the value is shifting from “out of the box” to “build your own,” and customers clearly believe building their own custom solutions around a microservices architecture will give their business a competitive advantage. Naturally, we expect ServiceNow wants partners to take the lead in Now Assist delivery, but for the GSIs to see value, GenAI has to actually change the business process.

2.Drive awareness through talent development efforts: ServiceNow’s growing portfolio outside the core IT service management (ITSM) space is creating new channel opportunities for services partners to capitalize on, compelling them to invest in training and development programs. Gaining the stamp of approval from a ServiceNow certification program enhances services partners’ value proposition, especially in new areas such as the Creator Workflow and Build portion of the ServiceNow portfolio, which positions them to drive custom application and managed services opportunities. Standing out in a crowded marketplace where services and technology providers vie for each other’s attention will elevate the need to invest in consistent messaging and knowledge management frameworks that elevate buyer trust.

3.Prioritize IT modernization ahead of GenAI opportunities and scaling NOW deployment: Some vendors have made GenAI capabilities available only to cloud-deployed back-office suites, meaning customers still on legacy systems must first migrate to the cloud before they can adopt the emerging technology. Partners must account for this modernization prerequisite by prioritizing traditional migration services through broader programs like RISE with SAP if they hope to pursue new opportunities over the long term. Reducing legacy technical debt will also free up resources, both human and financial, which will allow for broader ServiceNow portfolio adoption.

4.Set up outcome-based commercial models to scale adoption across emerging areas and protect against new contenders: Aligning commercial, pricing and incentive models that resonate with buyer priorities and achieving business outcomes can allow partners to expand addressable market opportunities, especially as scaling GenAI adoption necessitates greater trust in the portfolio offerings. ServiceNow’s consumption-based model provides a short-term hedge against potential tech partner disruptors, which may take on the risk to offer similar solutions but are able to better align with services partners’ messaging through the use of outcome-based pricing.

Acting as an abstraction layer, ServiceNow has a unique opportunity to further expand into the back office to address integration pain points but risks further overlapping with its SOR peers

ServiceNow positions as system of action to expose gaps in core system of record

Existing as a platform layer that orchestrates and integrates workflows, ServiceNow has long been able to successfully enter new markets without encountering a lot of head-to-head competition. But this is changing as ServiceNow, a $10-plus billion company, continues to drive traction with the LOB buyer by challenging a lot of the fragmentation that exists within front- and back-office systems. Over the past several quarters, ServiceNow has continued to launch new products in areas like talent management, finance and supply chain. One of the company’s biggest moves was in the front office with the launch of Sales & Order Management (SOM), giving customers the ability to use CPQ (configure, price, quote) and guided selling in a single product. Though ServiceNow famously integrates with all of the systems of record, these new innovations could pose a risk to the likes of SAP, Workday and Salesforce, which perhaps do not have the platform capabilities to build custom processes that can be tied back to the workflow, at least in a truly modern way. To be clear, ServiceNow is not interested in being a core CRM, ERP or human capital management (HCM) provider, and today acts as a service delivery system. But having customers store their data in the service delivery layer, as opposed to the core system of record so they can use that data against a specific workflow, is how ServiceNow aims to position as a “system of action.”

DXC Technology’s ServiceNow Ecosystem Strategy in Review

TBR assessment

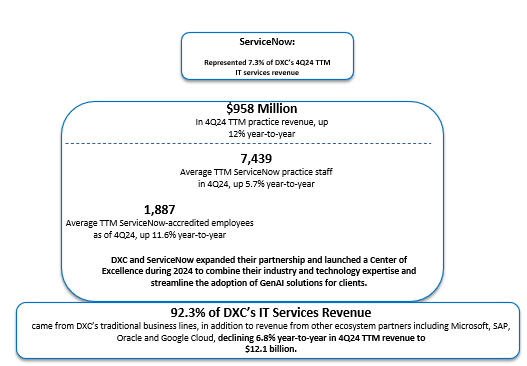

DXC Technology has an established history and deep expertise within the ServiceNow ecosystem, with a partnership spanning more than 15 years, a talent pool of over 1,800 ServiceNow experts, and a track record of more than 7,200 global implementations with over 350 instances managed worldwide, all of which position the company as a mature and experienced service provider for ServiceNow. Notable client wins, such as with the city of Milan (medical supply delivery during a crisis), Nordex Group (workplace safety management) and Swiss Federal Railways (unified customer inquiry management) underscore DXC’s ability to leverage the partnership to address diverse and critical business challenges across different industries and sectors. These successes highlight DXC’s capacity to translate its deep ServiceNow knowledge and implementation capabilities into tangible business value for its clients, suggesting a well-established and impactful ServiceNow practice.

Strategic portfolio offering

Through a strategic alliance with ServiceNow and bolstered by a dedicated global business group and acquisitions such as Syscom AS, TESM, BusinessNow and Logicalis SMC, DXC delivers a comprehensive range of ServiceNow-focused solutions. This approach enables DXC to digitize processes, enhance user experiences, and transform service management across the full ServiceNow platform, driving business innovation at scale, including specialized solutions such as those for the insurance industry, where DXC has had core competencies and long-lasting customer relationships. DXC’s offerings span enterprise applications transformation, security solutions, and compute and data center modernization, all designed to maximize client efficiency and agility utilizing the ServiceNow platform. The establishment of a new Center of Excellence in Virginia in November 2024, combining DXC’s industry strengths with ServiceNow’s solutions, further solidifies the two companies’ commitment to streamlining AI adoption and delivering cutting-edge solutions.

DXC Technology’s ServiceNow Ecosystem Strategy in Review (Source: TBR ServiceNow Ecosystem Report)

Technology Business Research, Inc.

Technology Business Research, Inc. Technology Business Research, Inc.

Technology Business Research, Inc.