Technology Business Research, Inc.

Technology Business Research, Inc.4Q24 AI & GenAI Market Landscape

TBR Spotlight Reports represent an excerpt of TBR’s full subscription research. Full reports and the complete data sets that underpin benchmarks, market forecasts and ecosystem reports are available as part of TBR’s subscription service. Click here to receive all new Spotlight Reports in your inbox.

‘If you save 30%, I want to save 30%’: the coming pressures on consulting and IT services, even as GenAI budgets increase

When PwC publicly stated its internal adoption of GenAI-enabled tools enhanced productivity and generated time and cost savings of up to 50% in software development and 30% in marketing, TBR’s clients began asking about implications for all consultancies and IT services companies if enterprise clients started expecting that those efficiencies would begin to lower their IT and consulting bills. A “customer zero” strategy helps IT services companies and consultancies test, calibrate and evolve technology solutions before rolling them out to clients. It also affords IT services companies instant credibility — “We’re using it ourselves!” — but the sword cuts the other way, too, if enterprise clients expect the efficiencies and cost savings will begin immediately.

In TBR’s view, managing margins while embracing — and delivering — GenAI-enabled solutions will be the biggest challenge facing IT services companies and consultancies in 2025.

“Managing the noise and risk around deploying GenAI services and solutions at scale will be key for vendors to take advantage of GenAI-related budget increases. We believe the advent of SLMs [small language models] and the emergence of a plethora of GenAI startups will test vendors’ positioning in the market, likely creating two camps: vendors that position themselves as tech-agnostic model orchestrators and those that use proprietary platforms to steer model development discussions in an effort to manage risk and decrease revenue sharing with tech partners.” — TBR’s November 2024 Digital Transformation: Voice of the Customer Research

Cloud vendors are all in on GenAI, despite dramatic investments and sparse returns in short term

Delivering GenAI services at scale is a massive undertaking, and cloud vendors of all types are moving full-speed ahead to maintain their competitive positions. From the IaaS and PaaS vendors alone, we expect capex spending to exceed $150 billion in 2024, a significant portion of which is driven by new data center locations and infrastructure build-outs to support AI-related workloads. Most of the large hyperscale platforms are increasing total capex spending by up to twofold on a year-to-year basis, noting AI as the largest driver of those increases.

The investment extends well beyond just capex, however, as R&D for new offerings, training and ecosystem investments targeted at AI technology are being undertaken.

Despite the furious pace and scale of investment taking place on the vendor side, customers remain tentative regarding their GenAI investments. The predominant use cases have remained stable since the initial onset of GenAI technologies, with customer service and general productivity being the most widely deployed. Together, the high cost of many GenAI services and the difficulty in clearly documenting financial returns from those investments have slowed the pace of spending. We expect 2025 to be a pivotal year for GenAI, as customers move beyond initial use cases and build operational and financial experience with the technologies.

AI infrastructure demand will see a new spike in early 2025 with launch of NVIDIA’s Blackwell GPU

AI server demand has increased rapidly over the past year, primarily fueled by purchasing from cloud service providers.

From Dell and Hewlett Packard Enterprise (HPE) alone, their combined AI server revenue increased from $1.2 billion in 4Q23 to $4.4 billion in 3Q24. This represents only a portion of the total market, as other vendors including NVIDIA, Supermicro, Lenovo and Penguin Computing have not published specific data on their AI server sales.

While revenues leveled off from 2Q24 to 3Q24, TBR expects demand to spike again once new server models are ready to ship with NVIDIA’s latest GPU.

NVIDIA’s H200 GPU, announced in November 2023, has had huge success reaching quarterly revenues in the tens of billions of dollars in 3Q24 and being deployed in data centers by all of the Big Three public cloud providers. A single AI server can use between one and eight H200 GPUs, demonstrating that the total infrastructure market opportunity will be many multiples in size.

In addition to server demand, AI use cases prompt the need for complex networking systems, storage equipment and all services. AI infrastructure vendors will need to capitalize on this broader opportunity to help support margins as the high volume of AI servers sold has negatively impacted profitability. Much of this ability to improve margins relies on increased enterprise adoption of AI infrastructure, as the cloud service provider customer base is more cost competitive.

PC OEMs and other ecosystem players are bullish on the opportunity presented by the advent of AI PCs, especially as new x86-based AI PC chips come to market

While TBR believes the ongoing rise of GenAI will continue to have more profound impacts on devices-adjacent technology markets, PC OEMs and other devices vendors across the industry are modifying their go-to-market strategies to align with evolving AI-driven market dynamics while also investing in the development and integration of AI-enabled capabilities and components to strengthen portfolio offerings.

For example, over the last several quarters PC OEMs, including those outside the Windows ecosystem, have increasingly invested in the development and marketing of machines powered by PC silicon offerings featuring a neural processing unit (NPU). The NPU is a dedicated chip component meant to accelerate and optimize certain AI workloads by offloading them from other compute-oriented components, like the CPU.

Despite Apple M Series chips having featured NPUs since their inception in 2020, silicon offerings featuring onboard NPUs for Windows-based machines first came to market in 2023. This development paved the way for the introduction of the AI PC, and despite the definition of an AI PC varying between OEMs and silicon platform providers, there is consensus that for a PC to be considered an AI PC, it must be equipped with components specifically designed to enable local AI acceleration.

As PC OEMs await the ramping of the next major PC refresh cycle, they are encouraged by the opportunities presented by the new AI PC category. The richer configurations of AI PCs support PC premiumization while new, albeit limited, AI features and capabilities are expected to drive increased advisory and professional services engagements as well as third-party software sales. However, TBR expects the lack of killer apps for the AI PC to continue to throttle the first wave of AI PC adoption, despite chip makers like AMD, Intel and Qualcomm all bringing more powerful AI PC silicon to market.

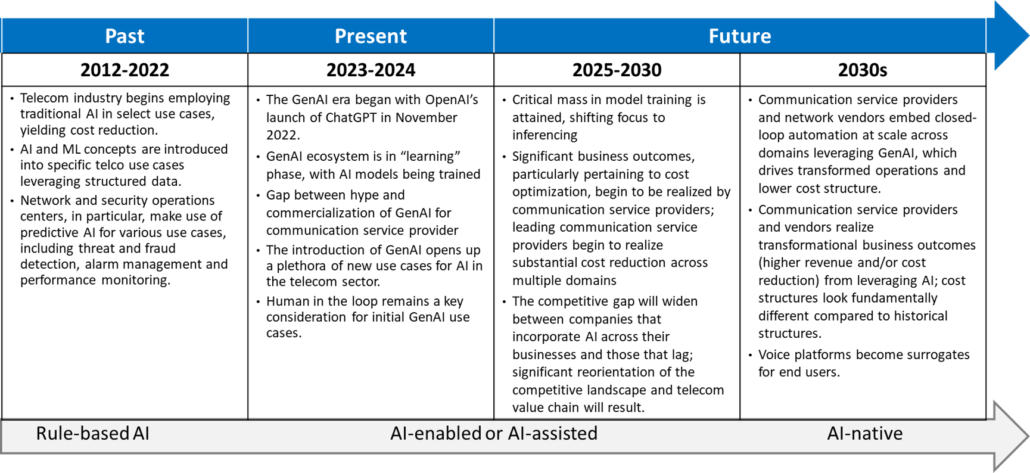

GenAI is expected to have a broad impact across the telecom industry, but the technology is still immature and transformation will take time as telcos tend to invest slowly in new technologies

GenAI Telecom Outlook (Source: TBR)

Technology Business Research, Inc.

Technology Business Research, Inc. Technology Business Research, Inc. (AI Generated)

Technology Business Research, Inc. (AI Generated)