With TBR’s Professional Services market and competitive intelligence research, understand the vendor strategies that are resulting in market-leading performance.

Examine portfolios, go-to-market strategies, services delivery, and revenue and profitability around IT services; strategy, operations, technology and organizational practices of management consulting firms; and vendor investment, divestment and portfolio repositioning of public sector vendors, focusing on professional, technical and IT services.

A free trial of TBR’s Insights Center platform gives you access to our entire Professional Services research portfolio and the ability to customize and curate reports detailing our analysis based on your company’s specific needs. Start your free trial today!

Trends we’re watching in 2025:

- Talent pyramid restructuring will challenge consultancies’ and IT services’ companies margins and HR management

- Generative AI revenues will shift from road-maps and MVPs to GRC and scale

- Political and macroeconomic uncertainty will fuel new consulting demand

Explore TBR Professional Services Coverage

Market & Competitor Benchmarks

Market and competitor benchmarks provide a comparison of vendor performance in a market, including analysis on vendor strategies, financial performance, go-to-market and resource management. The research graphically portrays comparisons of vendors by myriad metrics, calling out leaders, laggards and business models. Defensible, data-informed views of market opportunity and operational best practices are highlighted in each publication. TBR also provides benchmark data in Excel pivot tables.

Current Market & Competitor Benchmarks:

- Global Delivery Benchmark

- Healthcare IT Services Benchmark

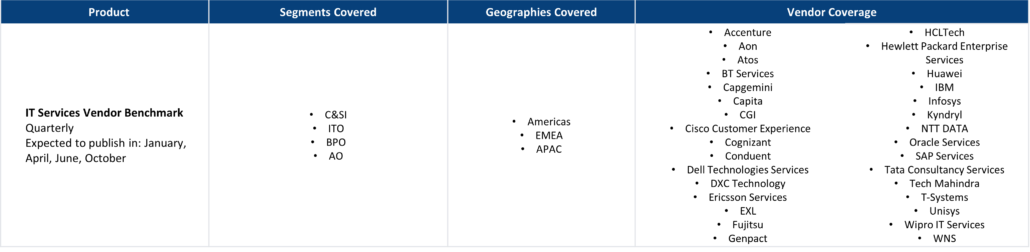

- IT Services Vendor Benchmark

- Management Consulting Benchmark

Market Landscapes

TBR’s vendor reports, snapshots and profiles provide deep-dive analysis of a single vendor across corporate strategies, tactics, SWOT analysis, financials, go-to-market strategies and resource strategies. Vendor performance is put in the context of market opportunity and competitive environment and our assessment shows where a vendor will success and its future market position.

Ready to Level Up Your Insights?

TBR’s digital-first competitive intelligence platform, TBR Insight Center™, allows for configured & customized views into IT markets, vendors, alliances and ecosystems.

Benefits delivered through TBR Insight Center™ include:

- Dynamic, configurable platform for TBR’s objective, independent and validated data and analysis

- Customizable views of millions of data points to match your specific needs

- Simple download functionality for customized views of analysis and feeds of data, saving staff dozens of hours per month

- Updates for market disruptions and emerging trends

Already a TBR Classic client but don’t have access to TBR Insight Center yet? Request access today.

EY Reinvents Its People Advisory Services, Leaning on a Single Methodology to Drive Successful Change

/by Kelly Lesiczka, Senior AnalystAs workforce and employee experience grow increasingly critical in the era of rapid technological advancement, EY’s refreshed approach within People Advisory Services — centered on a unified methodology and a stronger focus on people experience — helps distinguish the firm from its peers and better aligns with technology-driven transformation initiatives. Further, taking a global approach to retraining and methodology creates a more unified approach within the firm to better engage with clients and navigate market change.

AI Inferencing Takes Center Stage at Red Hat Summit 2025

/by Catie Merrill, Senior AnalystRed Hat Summit 2025 marked the company’s entry into AI inferencing with the productization of vLLM, the open-source project that has been shaping AI model execution over the past two years.