With TBR’s Cloud & Software market and competitive intelligence research, gain a true understanding of how technology and business strategies are being used by leading vendors to address the growing desire for cloud-enabled solutions. Our unique research in this space includes financial data that goes beyond just reported data, revenue and growth benchmarks, go-to-market analysis, ecosystem and partnership teardowns, and market sizing and forecasting.

Receive in-depth financial and business model analysis of the leading vendors in the cloud, rounded out with marketwide perspectives and direct insight from end-customer primary research. This combination of perspectives allows TBR to quantify the financial returns being generated from leading vendor strategies and identify where the market is headed based on feedback from customers making cloud investment decisions.

A free trial of TBR’s Insights Center platform gives you access to our entire Cloud and Software research portfolio and the ability to customize and curate reports detailing our analysis based on your company’s specific needs.

Start your free trial today!

Trends we’re watching in 2025:

- Scale, innovation and even repatriation will moderate cloud market growth in 2025

- Microsoft will narrow the gap with AWS in IaaS & PaaS market share, en route to leadership in 2027

- SaaS vendors will shrug off growing GenAI disillusionment, focusing on the long term by prioritizing GenAI agents within their development strategies

Explore TBR Cloud & Software Vendor Coverage

Market & Competitor Benchmarks

Market and competitor benchmarks provide a comparison of vendor performance in a market, including analysis on vendor strategies, financial performance, go-to-market and resource management. The research graphically portrays comparisons of vendors by myriad metrics, calling out leaders, laggards and business models. Defensible, data-informed views of market opportunity and operational best practices are highlighted in each publication. TBR also provides benchmark data in Excel pivot tables.

Current Market & Competitor Benchmarks:

- Cloud and Software Applications Benchmark

- Cloud Components Benchmark

- Cloud Infrastructure & Platforms Benchmark

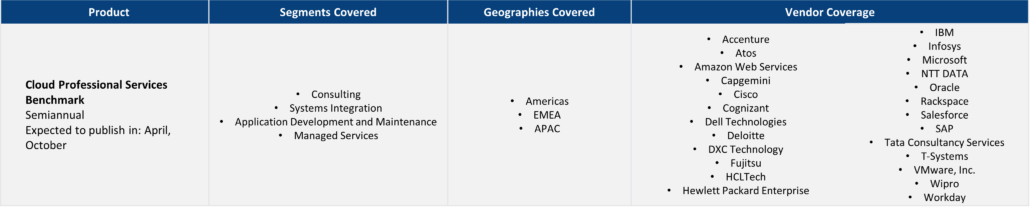

- Cloud Professional Services Benchmark

- Colocation Benchmark

Customer Research

Ecosystem Reports

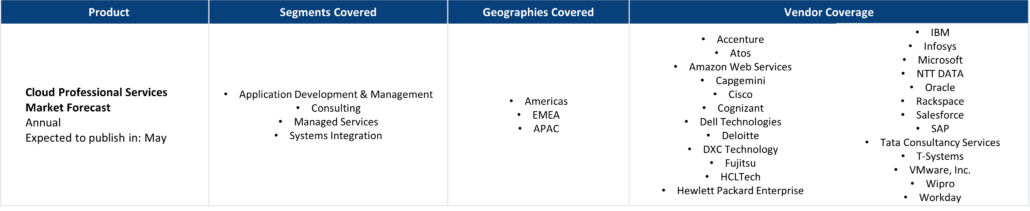

Market Forecasts

Market Landscapes

TBR’s vendor reports, snapshots and profiles provide deep-dive analysis of a single vendor across corporate strategies, tactics, SWOT analysis, financials, go-to-market strategies and resource strategies. Vendor performance is put in the context of market opportunity and competitive environment and our assessment shows where a vendor will success and its future market position.

Ready to Level Up Your Insights?

TBR’s digital-first competitive intelligence platform, TBR Insight Center™, allows for configured & customized views into IT markets, vendors, alliances and ecosystems.

Benefits delivered through TBR Insight Center™ include:

- Dynamic, configurable platform for TBR’s objective, independent and validated data and analysis

- Customizable views of millions of data points to match your specific needs

- Simple download functionality for customized views of analysis and feeds of data, saving staff dozens of hours per month

- Updates for market disruptions and emerging trends

Already a TBR Classic client but don’t have access to TBR Insight Center yet? Request access today.

AI Inferencing Takes Center Stage at Red Hat Summit 2025

/by Catie Merrill, Senior AnalystRed Hat Summit 2025 marked the company’s entry into AI inferencing with the productization of vLLM, the open-source project that has been shaping AI model execution over the past two years.

A Challenger Mindset Transforms HCLTech’s Approach to Financial Services to Achieve Success Through AI

/by Kelly Lesiczka, Senior AnalystHCLTech has a long history working with AI, building off its DRYiCE platform, the company’s original automation platform. This heritage equips HCLTech with the background and trusted technical expertise, backed by its engineering prowess. to deliver on clients’ AI transformation needs. Further, HCLTech can pursue larger-scale and more aggressive AI-led transformations, helping the company accelerate ahead of its peers in terms of client engagement and growth.