With TBR’s Telecom market and competitive intelligence research, examine telecom operator and telecom vendor markets as well as key industrywide trends and developments, such as 5G, edge computing, private networks, and the encroachment of hyperscalers into the telecom industry.

Understand operator business models, capital expenditure, subscriber metrics and next-generation technology adoption, with coverage spanning wireless, wireline, cable and enterprise markets. Access vendor customer demand analysis, portfolio analysis and competitive benchmarking.

Additionally, we are the leading resource for telecom infrastructure services (TIS) market research.

A free trial of TBR’s Insights Center platform gives you access to our entire Telecom research portfolio and the ability to customize and curate reports detailing our analysis based on your company’s specific needs. Start your free trial today!

Trends we’re watching in 2026:

- Impact of K-shaped economy on telecom market

- Why a price war is coming to the broadband market

- How telcos will adjust to meet AI’s timetable

- Ways in which the network needs to adjust for the AI economy

Explore TBR Telecom Coverage

Market & Competitor Benchmarks

Market and competitor benchmarks provide a comparison of vendor performance in a market, including analysis on vendor strategies, financial performance, go-to-market and resource management. The research graphically portrays comparisons of vendors by myriad metrics, calling out leaders, laggards and business models. Defensible, data-informed views of market opportunity and operational best practices are highlighted in each publication. TBR also provides benchmark data in Excel pivot tables.

Current Market & Competitor Benchmarks:

- Private Cellular Networks Vendor Benchmark

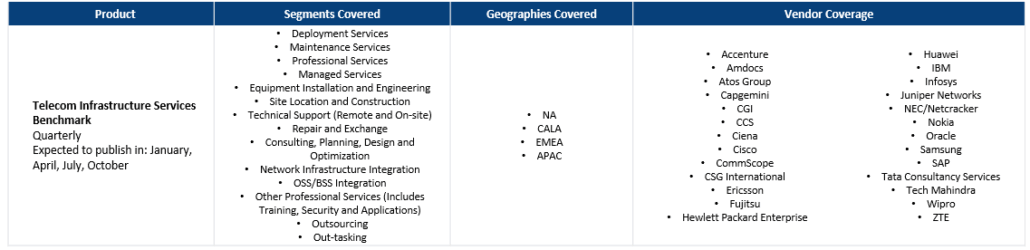

- Telecom Infrastructure Services Benchmark

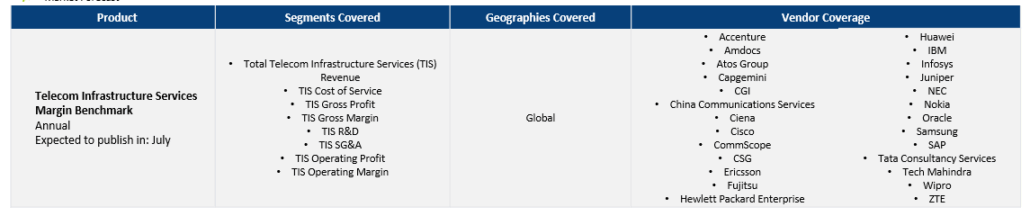

- Telecom Infrastructure Services Margin Benchmark

- U.S. Mobile Operator Benchmark

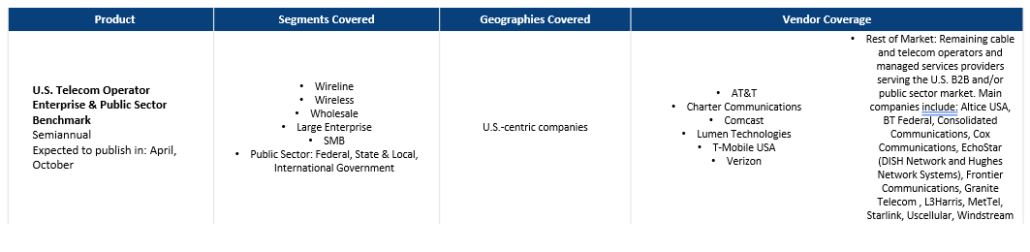

- U.S. B2B and Public Sector Telecom Operator Benchmark

Market Forecasts

Market Landscapes

TBR’s vendor reports, snapshots and profiles provide deep-dive analysis of a single vendor across corporate strategies, tactics, SWOT analysis, financials, go-to-market strategies and resource strategies. Vendor performance is put in the context of market opportunity and competitive environment and our assessment shows where a vendor will success and its future market position.

Telecom

- AT&T

- Cisco Systems

- T-Mobile USA

- Verizon

- Ericsson

- Nokia

Ready to Level Up Your Insights?

TBR’s digital-first competitive intelligence platform, TBR Insight Center™, allows for configured & customized views into IT markets, vendors, alliances and ecosystems.

Benefits delivered through TBR Insight Center™ include:

- Dynamic, configurable platform for TBR’s objective, independent and validated data and analysis

- Customizable views of millions of data points to match your specific needs

- Simple download functionality for customized views of analysis and feeds of data, saving staff dozens of hours per month

- Updates for market disruptions and emerging trends

- All data found in Insight Center can be leveraged to power your company’s AI tool via an API feed

Already a TBR Classic client but don’t have access to TBR Insight Center yet? Request access today.

Global Analyst Summit 2026: Value Creation Through Operating Model Transformation

/by Kelly Lesiczka, Senior AnalystAs consulting continues to evolve due to AI’s influence on business models and day-to-day operations across enterprises, EY’s leaders discussed how the firm is adapting its approach to guide clients through uncertainty and increased speed of change, and introduced featured clients, giving them an opportunity to share their experiences. The client stories emphasized the speed at which they need to navigate market changes and their desire to work with a long-term partner such as EY to guide the transformation as well as to create an ecosystem of vendors that support their end goals. The notion of value was consistent throughout the event, as the firm seeks to reconfirm its positioning in the consulting space despite ongoing market uncertainty about consulting’s future relevance.

The Race for Digital Sovereignty: How 4 IT Services Leaders Are Positioned

/by Jill Cookinham, Research AnalystTBR Fourcast is a quarterly blog series examining and comparing the performance, strategies and industry standing of four IT services companies. The series also highlights standouts and laggards according to TBR’s quarterly revenue projections as well as its geographic and segment estimates. With discussions about sovereignty in Europe only becoming louder, TBR thinks it is worthwhile to examine Atos Group, CGI, Fujitsu and Kyndryl. Our intent is to shine light on these similarly sized companies that have a strong presence in Europe and/or a strong presence in ITO and consulting and to discuss where each company’s opportunity lies.

Are Hyperscalers Really Competing for Services Revenue?

/by Jill Cookinham, Research AnalystTBR has consistently highlighted hyperscalers’ professional services units, despite their relatively small revenue streams, as potentially credible threats to IT services companies. Hyperscalers do not intend to displace global system integrators (GSIs) in consulting or managed services, but their growing services capabilities create more margin pressure for (and anxiety among) the GSIs each quarter. This report examines where hyperscalers’ professional services units overlap with GSIs’ and how their roles continue to evolve, beginning with comparison of the companies’ services operating models.